Each year Aswath Damodaran at NYU kindly updates the annual returns for stocks (S&P 500), bonds (10 year Treasuries) and cash (3-month T-bills) going back to 1928.

I love this data because stocks, bonds and cash are the building blocks of asset allocation.1

Sure, you can add other asset classes and strategies but those three are where most investors should start when it comes to figuring out your portfolio mix.

These were the returns for each asset class in 2022:

- Stocks: -18.0%

- Bonds: -17.8%

- Cash: +2.0%

Cash beat stocks and bonds for the first time since 2018 and had its highest return since 2007.

Stocks and bonds have higher long-term returns than cash but it’s not out of the ordinary for cash to be the best asset class in a one year time frame.

By my count, it’s happened 14 times over the past 95 years. So relatively rare but not out of the question. Before 2018, the last time it happened was in 1994.

Bonds have beaten stocks 35 times in a calendar year since 1928. Cash has beaten stocks in 31 out of the past 95 years.

So while stocks are your best bet over the long run, over the short run anything can happen.

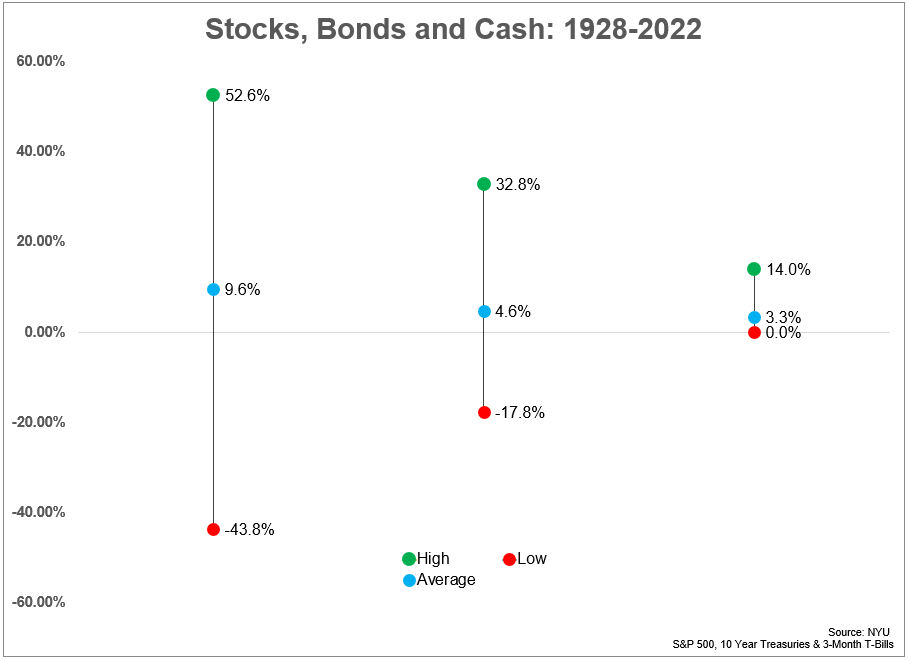

These are the annual returns for each from 1928-2022:

- Stocks: +9.6%

- Bonds: +4.6%

- Cash: +3.3%

Long-term investing is great and all but returns over the short-term are anything but average.

Looking at the range of results around the averages does a nice job of explaining why the long-term returns line up like they do:

Stocks go up for lots of reasons but one of the biggest ones is the fact that sometimes they go down a lot.

The S&P 500 has been down in 26 of the last 95 years. Bonds were only down 19 times but stocks declined double-digits 12 times while 10 year Treasuries have had just 2 calendar years with returns of -10% or worse.

Cash has never had a down year on a nominal basis.2

This is the trade-off we’re forced to make as investors.

Cash gives you short-term peace of mind and not much variability but low expected returns. Stocks provide protection against inflation over the long-term but kick you in the teeth on occasion in the short-term.

Bonds are somewhere in the middle.

Inflation is all the rage these days so it’s also helpful to look at the long-term returns net of the inflation rate.

Inflation has averaged a little more than 3% from 1928 through 2022 which leads to the following real annual returns in that time:

- Stocks: +6.5%

- Bonds: +1.5%

- Cash: +0.2%

The point of this exercise is not to prove the superiority of any one asset class over another. They all have their own pros and cons.

The point is that it’s helpful to know going into each asset class what you can reasonably expect in terms of outcomes over various time horizons.

No one knows what the exact returns will be like over the next 95 days or 95 years for stocks, bonds or cash. There are a lot of variables we simply cannot predict.

But it’s a safe bet to assume stocks will beat bonds and bonds will beat cash over multi-decade periods.

It’s also safe to assume cash or bonds can beat stocks over a year or even multi-year periods.

This is what makes investing relatively simple but never easy.

Further Reading:

Updating My Favorite Performance Chart For 2022

1I use this data all the time on this website.

2On a real (inflation-adjusted) basis cash has been down 41x since 1928.