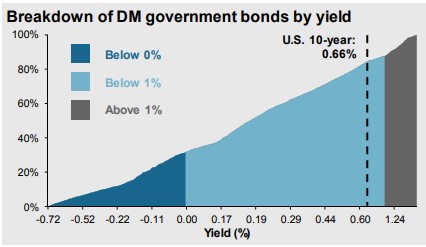

The latest JP Morgan Guide to the Markets has an incredible chart showing how yield-starved the fixed income markets are across the developed world:

Around 90% of developed countries have government bond yields of 1% or less. Almost 40% of these countries have negative yields.

Rates are low for a reason. We’re in the midst of a depression which is a deflationary force and central banks are doing their damnedest to keep rates down to be able to fund all of the government spending and keep borrowing rates low.

I don’t pretend to know the path of rates going forward but safe bond yields at these levels are bound to have unintended consequences. Here are some thoughts on what this means for investors:

1. Savers shouldn’t expect much. My online savings account currently offers 1.05% interest but I don’t expect that number to remain above 1% for very long. The Fed has set their short-term benchmark rate at 0% and it sounds like it’s going to stay there for a few years at a minimum.

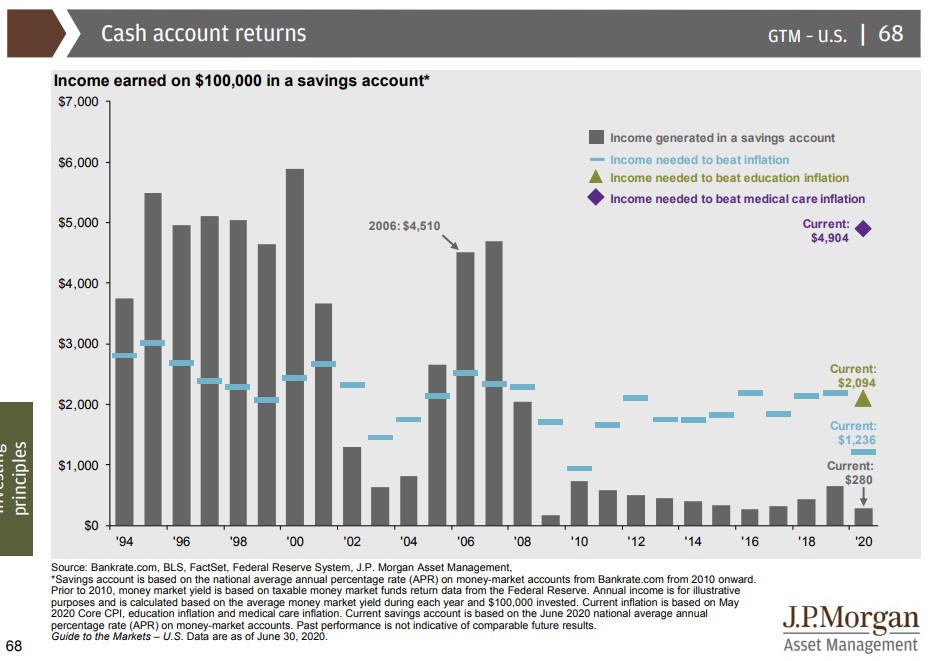

JP Morgan also shared a chart showing how much you could earn on savings accounts going back to the 1990s:

Not only are current rates likely to lose out to even a hint of inflation but there’s no way they can keep up with spending categories such as education or healthcare where prices have risen faster than the averages for years.

The days of earning 5-6% interest on your savings are over.

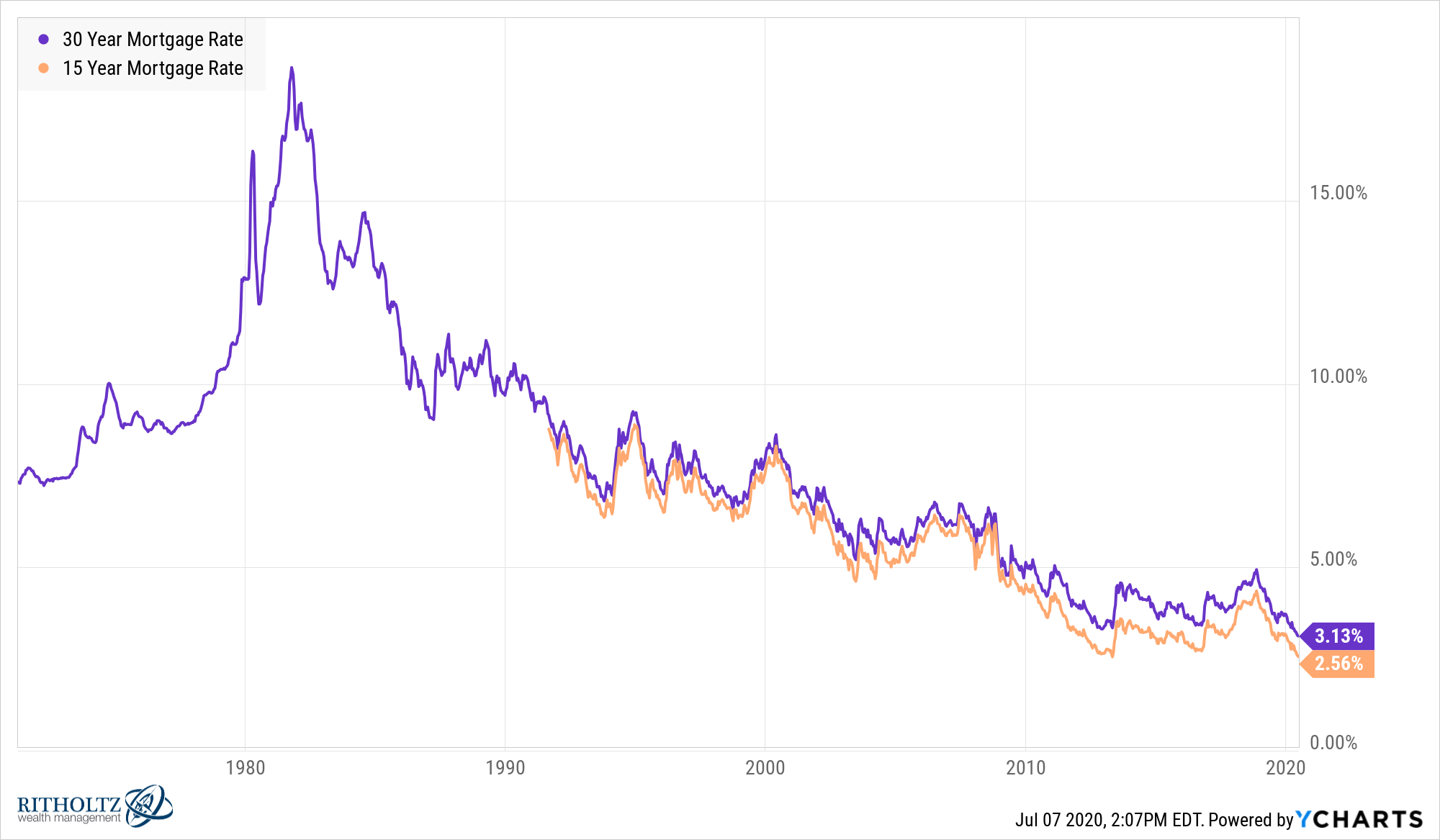

2. Borrowers are getting help. Savers are being punished but borrowers are in a position to take on debt at the lowest rates in history:

Once you factor in the tax savings on a mortgage and inflation you’re essentially borrowing for free on a net-real basis these days. If you can get approved for a mortgage or re-fi, you can save some serious money on long-term interest payments.

3. Investible assets have to go somewhere. The stock market can act as an incinerator of investor capital at times, much like it did earlier this year but money has to go somewhere. Sure, everyone could simply sit in cash if they’re worried about the stock market but that’s not a long-term solution, especially at today’s yields.

By keeping interest rates low, the Fed is begging investors to take more risk with their capital. This might be the simplest explanation for the continued strength in the stock market.

4. Historical valuations tools will be harder to use. I know, I know — Ben, are you saying this time is different!?

No, every time is different but in terms of rates, it’s really different this time.

If you’re waiting for valuations to revert back to some magical 15x average CAPE ratio from 1871 you may be waiting for a long time if the low yield environment is here for some time.

The best argument against this line of thinking is a place like Japan where interest rates have been on the floor since 1990. Rates have been low or negative in many European countries for a number of years now too.

My counterargument to that case would be the United States now makes up 55% of the global equity market cap. Fifty percent of all Americans take part in the stock market (it was just 1% of the population in the Great Depression). Americans are on their own when it comes to saving and investing for retirement and we have a much worse social safety net than these other countries.

At the height of the dot-com bubble, the highest stock market valuations in history, investors could still earn 5-6% yields on U.S. Treasuries. That is not the case today.

Valuation is not useless but it does require context.

5. Mini booms and busts may be here to stay. In a world with no safe assets that offer investors a living yield on their investments, where investors are pushed further out on the risk curve, there will likely be more volatility.

The Fed may have taken the Great Depression scenario off the table but it wouldn’t surprise me to see more super-fast bear markets like we experienced in March but also to a lesser degree at the end of 2018.

I wouldn’t be surprised to see more flash crashes or sharp bear markets that recover relatively quickly in the months and years ahead.

I’m still thinking through the many different ways investors and savers can prepare themselves for this situation but I feel safe in labeling this the hardest market environment ever for retirees.

There are no easy options available to investors today.

Further Reading:

My New Theory About Future Stock Market Returns