People have been calling this a “low return envionrment” for a number of years now which defies all logic considering how great returns have been in the markets. But eventually those who have been predicting lower returns will be right. Lower than average returns are nothing new because markets are always and forever cyclical. This piece I wrote from Bloomberg looks at some of the worst historical returns for a stock-bond portfolio and also offers some other considerations when we do finally experience this type of market environment.

*******

Jack Bogle, Vanguard’s founder, is on record stating that future returns in the financial markets will be below average. In his book and in recent interviews, Bogle has said expected returns for stocks and bonds should both be muted for the coming decade or so.

Based on current dividend, valuation and yield levels, Bogle predicts annual returns for U.S. stocks of about 4 percent, and of 3 percent for high quality U.S. bonds over the next 10 years. On a typical balanced 60/40 stock/bond portfolio, that would mean an annual return of just 3.6 percent. He admits that there are a host of factors that go into these types of forecasts so they are simply educated guesses.

Bogle’s expected returns may be spot on, but they could be too high or too low. Valuations can always go higher or the music could end on this bull market tomorrow. Either way, investors in risk assets need to understand that low returns are a feature of the financial markets, not a bug.

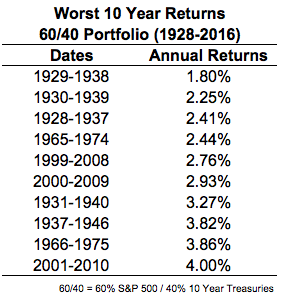

Using data on the S&P 500 and 10-year Treasuries as proxies for stocks and bonds, I looked at the historical 10-year annual returns for a 60/40 portfolio from 1928 to 2016. Here’s a list of the 10 worst 10-year returns for this balanced portfolio:

Financial historians will notice that each of these instances included periods of enormous market stress. These include the Great Depression, the 1970s bear market, the bursting of the dot-com bubble or the recent financial crisis or their aftermath.

Annual returns came in below 4 percent in 12.5 percent of all rolling 10-year periods in this time frame. That means investors experienced returns that were similar to Bogle’s prediction in one out of every eight years. So you need to prepare yourself for below-average returns at some point as a long-term investor. It’s not “if” but “when” for below-average returns in risk assets.

No one can nail the timing of when below-average returns will hit, but there are a number of factors investors need to be aware of when this occurs.

Inflation. Most people don’t realize inflation is a relatively new phenomenon. From 1871-1940 the annual inflation rate was basically zero. The total rate of inflation in that period was just 13.2 percent or around 0.2 percent on an annual basis. Since then, inflation has come at a much stronger clip, at close to 4 percent per year. From 1970-2007, inflation was even higher, at close to 5 percent a year. Since 2008, inflation has slowed substantially, at 1.6 percent. Although it’s certainly possible nominal returns will be lower, the only returns that matter to investors are their after-inflation figures. If inflation stays subdued, investors could earn much closer to historical returns on a real basis.

Cost matters. Just as real returns matter more than nominal returns when it comes to inflation, net returns after accounting for all costs matter more than gross returns. Costs always matter for investors but fees, expenses and trading will have a much large impact on the bottom line in a low-return environment. Anyone who has studied the stock market from a historical perspective can tell you stocks have earned around 10 percent a year going back over the past 100 years or so. The problem with this figure is that it does not account for costs, which at one time were extremely prohibitive to investors. Before the mid-to-late 1970s, investors could expect to lose 2 percent to 3 percent on each trade they made in brokerage commissions and bid-ask spreads alone. Mutual funds used to carry 8 percent to 10 percent sales loads. It was also almost impossible to diversify properly. It’s not what you earn but rather what you take home that matters in the markets.

Someone must lose. Investing is a zero-sum game. In order for one party to win, another party must lose. And after accounting for inflation and costs this means many more investors end up losing than winning. But in a lower-return environment, underperforming can be even more devastating. It’s no fun to underperform in a raging bull market, but even then almost everyone should be making money. If you’re on the losing side of the equation when market returns are muted, your portfolio could go nowhere even as the markets slowly climb. Many investors will try harder by taking more risk when yields are low and valuations are high. There is a higher degree of difficulty in undertaking such a strategy, which will likely lead to very poor performance from investors who don’t understand their risk profile or time horizon correctly.

The other problem with low expected returns is that the path to get there is impossible to predict. We could certainly see a crash or even multiple crashes in the years ahead but markets could simply go nowhere for some time, as well. The bull market could continue for a number of years but eventually we’ll see lower-than-average returns. Investors would be wise to prepare for a wide range of outcomes in that scenario.

Originally published on Bloomberg View in 2017. Reprinted with permission. The opinions expressed are those of the author.