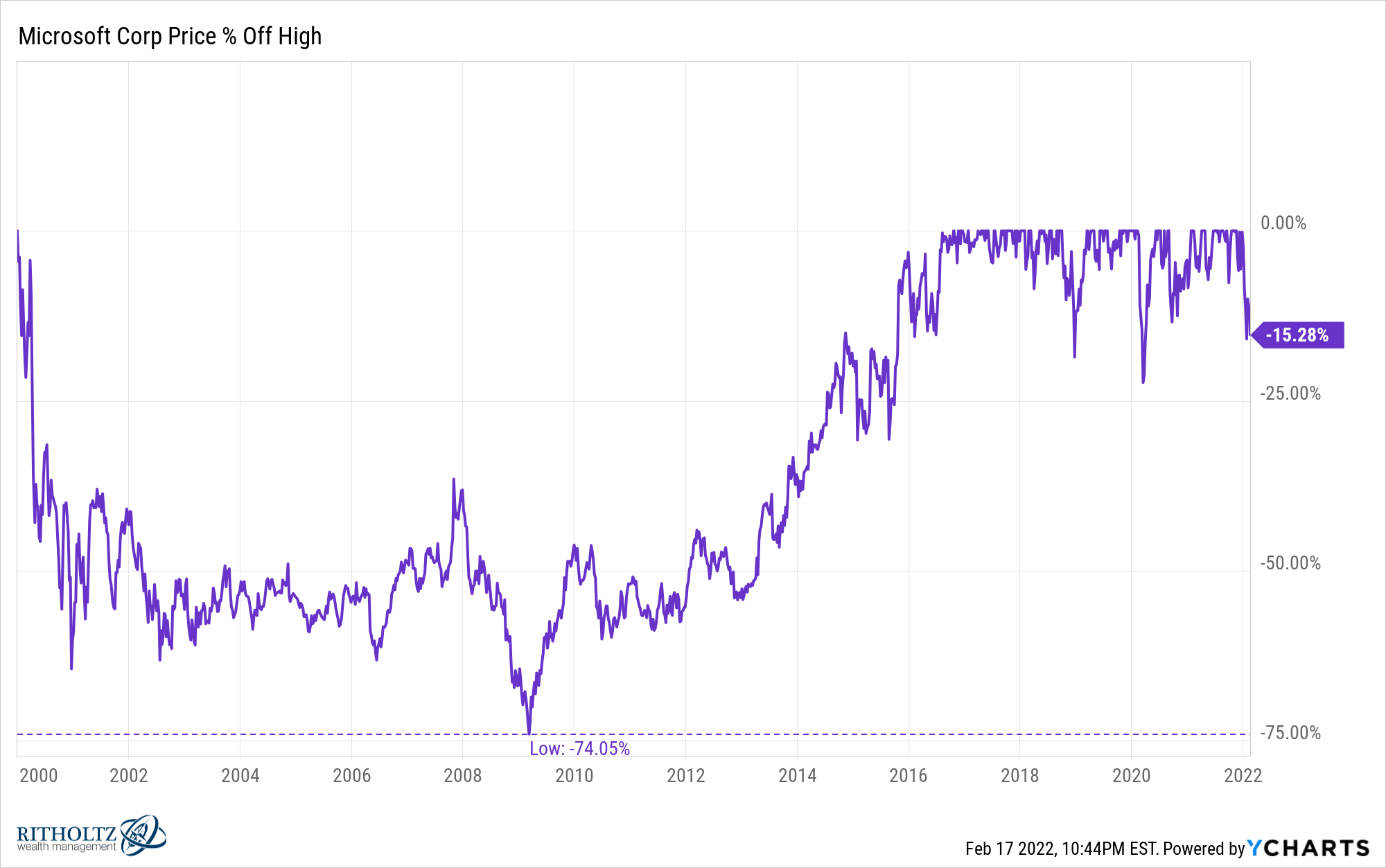

From 1990 through the end of 1999, Microsoft’s share price went from around 60 cents to almost $60.

That was a gain of nearly 10,000%, good enough to turn $10k into $1 million.

Not bad.

Then the tech bubble burst and the stock fell 60%. After basically going nowhere from 2001 to 2007 the stock crashed right along with everything else in 2008.

By the time the market bottomed in early 2009 the stock was 74% off all-time highs from the end of 1999:

The company went from a $613 billion market cap in 1999 to $135 billion by March 2009.

By any reasonable measure, Microsoft is one of the most successful tech companies ever created. It’s now a $2+ trillion behemoth.

But you can see from the chart that nasty drawdown took more than 16 years to break even with the 1999 highs.

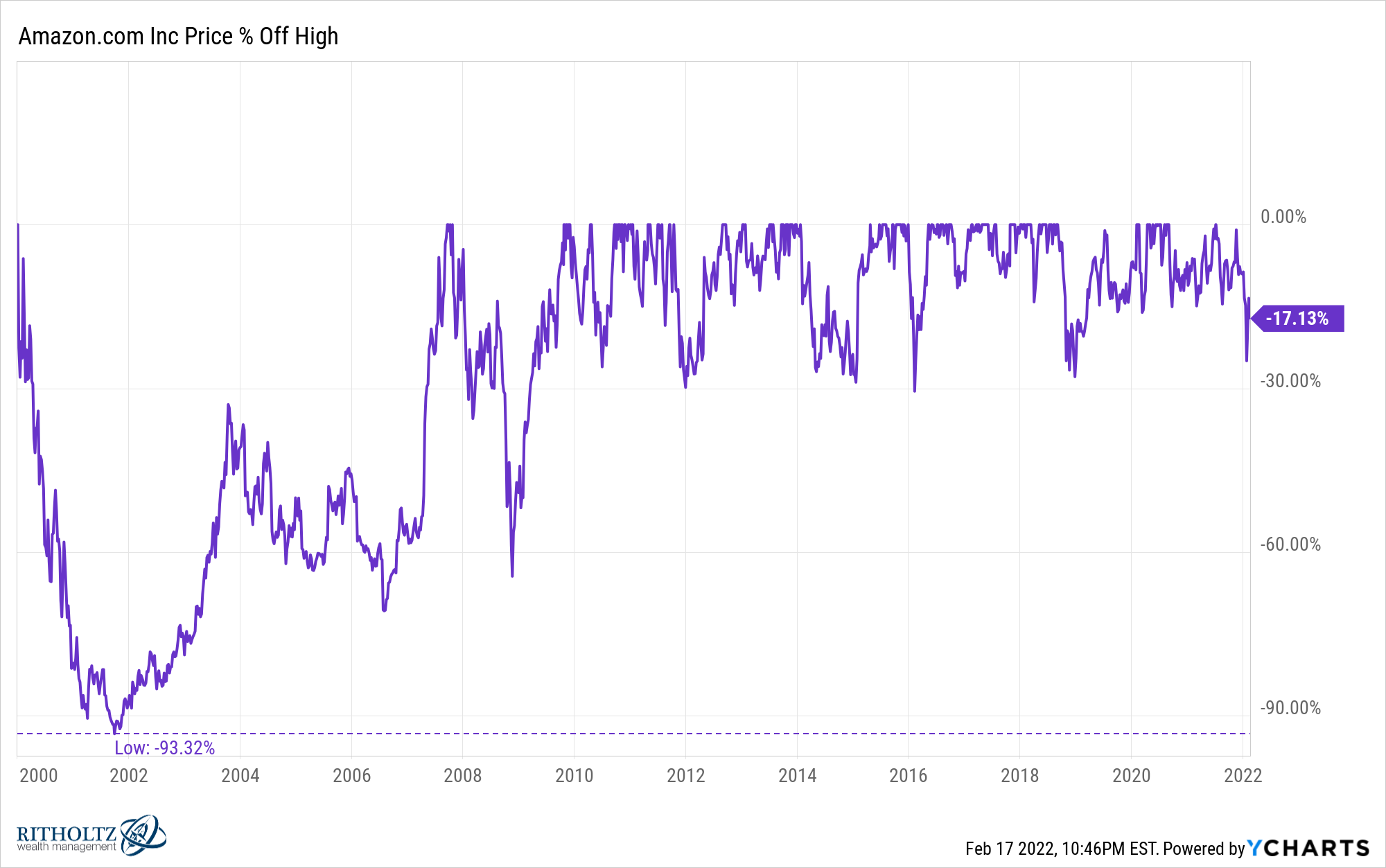

Microsoft is not alone in experiencing an extended drawdown from the dot-com bubble highs.

Amazon crashed more than 90%, broke even 7 years later for the blink of an eye just in time for the peak of the market in the fall of 2007 before the onset of the Great Financial Crisis:

Amazon spent 99.9% of the time below 1999 levels through 2010.

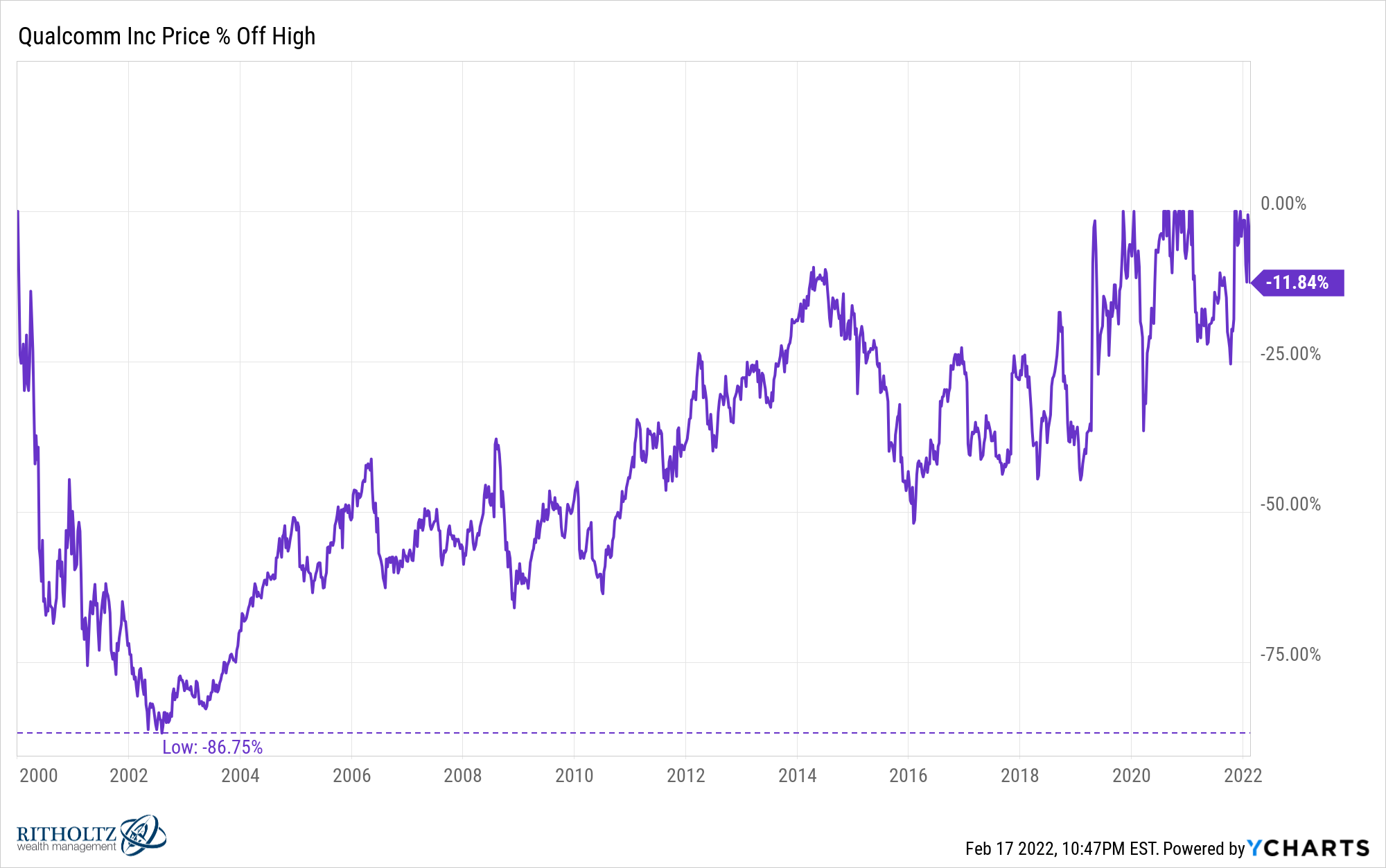

Qualcomm didn’t make it back to 1999 price levels until May 2019:

Cisco still hasn’t come close to reclaiming early-2000s levels:

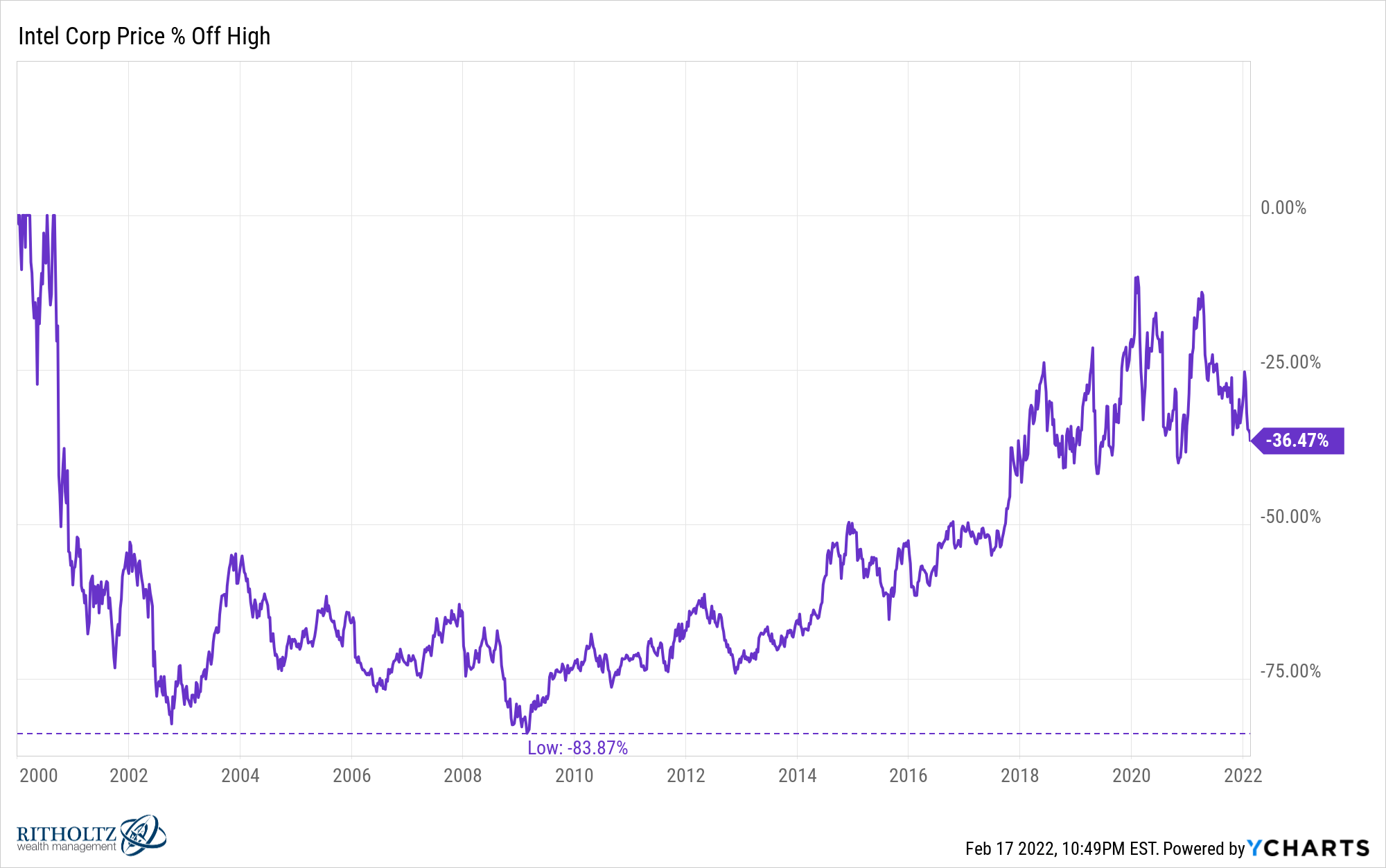

Same with Intel:

These are some of the biggest, most successful technology companies ever yet their stock prices have gone through drawdowns that have lasted for decades.

Obviously, the starting point here was the peak of maybe the biggest stock market bubble we’ve ever seen in U.S. stocks.

But tech stocks are prone to these boom-bust cycles because innovation always causes bubbles. We simply can’t help ourselves.

I’m not saying today’s tech stocks that are getting killed are in for a similar extended winter. But growth investors also shouldn’t assume all of these stocks that are down 50-80% are going to be back at new highs in a hurry.

The Nasdaq Composite was up 41% per year (450% in total) from 1995-1999. From 2017-2021 it was up 25% per year (205% in total). So we didn’t reach the level of insanity from the late-1990s but we were in the parking lot of the ballpark.

It’s also worth noting the Nasdaq Composite is still only 15% off its highs right now.

But within the index there is plenty of carnage:

- Half of the stocks in the index are down 30% or worse

- 40% of stocks are down 40% or worse

- 35% of stocks are down 50% or worse

- 28% of stocks are down 60% or worse

This is a small sample size but here are some of the biggest brand names currently in the midst of a painful drawdown:

Facebook, Netflix, Shopify, PayPal, Zoom and Square have lost more than $1.1 trillion in market cap from their peaks seen in 2021.

If you’re a holder of one of these stocks or any of the other growth stocks getting slaughtered, your level of pain obviously depends on when you bought them.

Many of these stocks still have wonderful long-term returns even with the recent plunge.

But if you got in over the past couple of years you’re definitely feeling it.

I don’t know if the growth stock sell-off will continue. It could depend on the overall market and whether some of the big names like Apple, Google, Microsoft and Amazon join the party.1

If there is another leg down for the growth stocks that are crashing it’s important to remember it could always get worse.

Remember that a stock price going from a loss of 60% to a loss of 75% is not an additional 15% down. It’s a further loss of nearly 40%.

I’m not predicting this but just putting it out there since it’s always a possibility.

Predicting what will happen to the stock market in the short run is always difficult but the path of individual stocks is even harder.

I’m not smart enough to sort out the winners and the losers when we see a repricing like this.

The counterpoint to this argument is markets are moving faster than ever these days.

But it could take a while, even for the best of breed software companies, to see their stock prices re-gain previous highs.

Further Reading:

Why Bubbles Are Good For Innovation

1These stocks are down 8%, 10%, 12% and 14%, respectively. So they’re in a correction but not a crash like many of the other growth names.