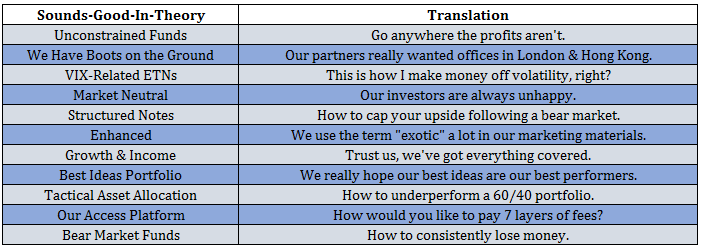

Now for some context on the Sounds-Good-In-Theory Portfolio:

Unconstrained funds. Go-anywhere funds sound great in theory until you realize that anywhere is a pretty wide open mandate in a marketplace overflowing with choices. The portfolio manager has to be right on way more decisions with an unconstrained fund which means they have more opportunities to be wrong on things like timing and poor execution of an investment thesis.

We have boots on the ground. The truth is information barriers are continually being broken down as technology improves our ability to communicate with one another. Sure, some local funds perform better, but there’s no discernible advantage to having “boots on the ground” in another country or region. This myth is mainly a product of good marketing.

VIX-related ETNs. VIX funds always sound interesting after volatility has picked up. In reality, very few investors understand what the VIX even represents or how it is structured. Most funds indexed to the VIX in some way are complete and utter failures.

Market neutral. These funds seek to improve performance by providing an uncorrelated return stream. However, in theory the expected return of a market neutral portfolio should be zero as the long and short exposure nets out to zero. The manager or strategy must produce alpha to actually achieve positive uncorrelated returns on both the long and short side of the ledger. Easier said than done.

Structured notes. These products are usually rolled out following a large move in the markets one way or another. They promise to limit your downside participation in the stock market with the understanding that you’re capping your upside. They’re expensive, inefficient products that are mainly used to fight the last war. There are far easier ways to reduce your exposure to market risks.

Enhanced. Take a good idea and make it better? Enhanced funds are more likely to take a good idea, add on a layer of fees, derivatives and complexity and make it harder to understand and easier to do worse than the original strategy.

Growth & income. I feel like the only place you really see growth and income mutual funds are in 401(k) plans. They sound really smart to people who don’t know a ton about the markets. Growth? Yes! Income? That would be great! Basically, these funds end up being closet index funds that hold a mish-mash of growth and value stocks and look very index-like for higher fees.

Best ideas portfolio. Shouldn’t all funds be a best ideas portfolio? If portfolio managers knew their best ideas ahead of time they would simply invest in those securities and call it a day. Most of the best performers each year probably don’t come from the pre-selected best ideas of a portfolio manager.

Tactical asset allocation. The majority of tactical asset allocation funds have been huge disappointments to those investors who piled into them following the crisis. I’m weary of any tactical asset allocation model that isn’t heavily systematic with a disciplined practitioner running it. And even with a good process these strategies are not easy to follow.

Our access platform. Many consultants and brokerage firms will preach the benefits of investing with them based on the “access” they can provide to top tier funds. If funds are closed to the majority of investors, chances are this type of program will just mean you’ll be paying more fees than the current investors to gain access to a fund that’s looking to make some extra money. By the time top tier funds reach this point in their business life-cycle the outperformance is usually long gone and the owners are looking to cash out.

Bear market funds. There are the funds that no one wants to own 3 out of every 4 years, but when markets fall, everyone questions whether or not they should own a short biased fund. Since the long-term trend of the market is up, these funds are fighting an uphill battle the majority of the time. The expected return of a bear market fund in negative.

Subscribe to receive email updates and my quarterly newsletter by clicking here.

Follow me on Twitter: @awealthofcs

My new book, A Wealth of Common Sense: Why Simplicity Trumps Complexity in Any Investment Plan, is out now.

[…] Things, like ‘structured notes,’ that sound better in theory than practice. (awealthofcommonsense) […]

Thanks for making me laugh this morning!

[…] Some humour from A Wealth of Common sense, talking about the different marketing names given to funds and investment ideas. Remember simpler is normally better and definitely cheaper over the long run – The Sounds-Good-In-Theory-Portfolio […]

[…] Cap Secret No One Ever Told You (Irrelevant Investor) • The Sounds-Good-In-Theory-Portfolio (A Wealth of Common Sense) • Washington’s blockbuster budget deal could be the end of an era (Business Insider) […]

It is all “Financial Manufacturer Packaging”, a.k.a. Product Pushing, a.k.a. “Lipstick on a Pig”… (Selling rather than Investing)

Reminds me of the Crap the Wire houses were telling us to sell in the 80’s, “Enhanced” Yield Government Bond Funds… If investors had of only purchased a 30-yr Treas and held till maturity, they would have made a fortune… but the firms would have made nearly zip.

They are in the business to make money for NY, not for clients…

Sad, nothing has changed on that side of the fence..

[…] https://awealthofcommonsense.com/the-sounds-good-in-theory-portfolio/ […]

[…] The Sounds Good in Theory Portfolio. Love the pic below, priceless! […]

What about annuities?