“The investor’s chief problem – and even his worst enemy – is likely to be himself.” – Benjamin Graham

One of the best performing mutual funds of the past decade is the Fairholme Fund, which is run by portfolio manager Bruce Berkowitz. The ten year annual return on the fund outpaces the S&P 500 by nearly 4% a year.

Berkowitz is notorious for going against the grain with his investment approach. The fund is usually concentrated in only a handful of stocks. At times he holds high levels of cash.

For an active mutual fund, it’s fairly uncorrelated with the broader market, which is rare these days.

This can lead to periods of extreme variation from the market which occurred in 2011 when the S&P was flat but Fairholme was down more than 30% after a heavy bet on financial stocks.

The opposite was true as Berkowitz outperformed the index by a wide margin in 2012 with a comeback year.

It was a wild ride, but those investors that hung in their were rewarded with market-beating results.

Unfortunatelty, not many did. Instead they traded in and out of the fund and missed out on most of the gains.

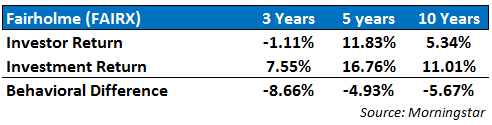

Courtesy of Morningstar, these are the actual returns earned by investors in the fund versus the stated return earned on the fund for those investors that bought the fund and held for on the the entire period (through year end 2013):

You can see the effect that behavior has on actual investor returns In these numbers.

Poor timing and fund flow decisions caused investors to underperform the S&P 500 over 10 years even though the fund outperformed by a wide margin.

(Side note: Investor returns are calculated on a dollar-weighted basis, so they take into account the timing and magnitude of fund flows from investors. Basically, the investor returns measure average returns actually earned and investment returns measure a buy and hold strategy from day 1, hence the behavioral difference.)

The lack of persistence in returns is what makes active mutual funds so hard to invest in. It’s impossible to tell whether or not a star manager can keep up their great performance or not.

The easy solution to this problem is to simply invest your money in index funds then, correct? In the immortal words of Lee Corso, not so fast my friends.

While index funds do offer investors broad diversification at a low cost and take away the temptation to chase the hot active mutual funds they don’t solve the market timing problem that seems to plague so many investors.

It’s still far too tempting to jump in and out of the best performing stock markets (large, mid, small, int’l, emerging markets, etc.).

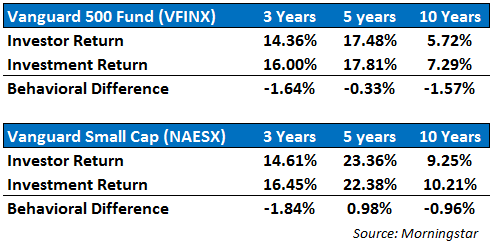

See the return numbers on the Vanguard 500 and Small Cap funds to see this in practice:

Now, the behavioral difference is much smaller in these funds than in the Fairholme Fund, but you can still see some distance in the 10 year numbers, especially on the 500 Fund.

Many investors became convinced they could time the markets after seeing the large losses sustained during the financial crisis.

The question then becomes, are there any mutual funds that show positive investor behavior?

Actually, there are.

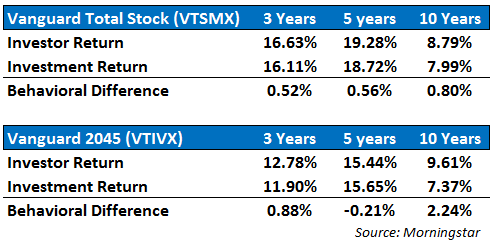

Here are the results from the Vanguard Total Stock Market Fund and the Vanguard Target Retirement 2045 Fund:

You can see both have positive behavioral differences and the 2045 Fund has an amazing 2%+ outperformance by investors versus the fund returns.

What could be the reasoning behind the positive behavior in these funds?

They are far more diversified than an active fund or simple sinlge market index fund. The total market fund includes large, mid and small cap stocks as opposed to the large cap only and small cap only funds profiled above.

The Target 2045 Fund contains a diversified four fund portfolio of both U.S. and international stock and bond funds.

Basically, the reason for the positive behavioral element is the fact that these funds take away the need to watch your behavior as long as you don’t try to continually time the market by going to cash when you get nervous.

In the Total Stock Market Fund, you don’t have the option of jumping in and out of large, mid or small cap stocks. You hold them all based on their weights in the index.

And the Target 2045 Fund has an asset allocation set by Vanguard and rebalanced for you so you don’t even have the opportunity to change your fund line-up. It’s simply done for you.

Critics of these funds claim that they don’t optimize your personal risk profile and situation perfectly.

This is true, but it’s amazing how much better investor performance can be when the human/emotional element is taken out of the equation.

Targetdate funds are usually the default option for employee retirement plans so the majority of the investors in the fund simply dollar cost averaged on a periodic basis throughout the 10 year period that saw many ups and downs along the way.

The fund was also extremely diversified and systenatically rebalanced each year, a simple strategy that has little to no complexity involved.

Yet this fund’s investors outperformed all of the other investors in the four funds we looked at here.

Once again, this shows that the investment strategy you choose to implement has much less bearing on your performance than actually sticking to a long-term plan no matter what happens in the market.

When all else fails, you should abide by Warren Buffett’s Fouth Law of Motion (emphasis mine):

“Long ago, Sir Isaac Newton gave us three laws of motion, which were the work of genius. But Sir Isaac’s talents didn’t extend to investing: He lost a bundle in the South Sea Bubble, explaining later, “I can calculate the movement of the stars, but not the madness of men.” If he had not been traumatized by this loss, Sir Isaac might well have gone on to discover the Fourth Law of Motion: For investors as a whole, returns decrease as motion increases.”

Further Reading:

Indexing is no pancea for investors (Abnormal Returns)

[widgets_on_pages]

Follow me on Twitter: @awealthofcs

That was my learning too. As much you trade as worse results you get. So limit your trading and be consistent in your investing. Easy to say, hard to do.

Recently, I programmed a filter in Strategy Desk picking up stocks with a good potential to grow. I am now testing it in real life and the goal is to apply a given investing routine, like a computer. Completely eliminate human emotions causing us chasing stocks and trade like crazy.

A systematic, rule-based approach is probably the process that could help investor’s the most with the behavior issue. Things like collar cost averaging and automatic rebalancing should be no-brainers for 99% of investors.

A checklist approach is another advantageous route to take, especially with a program like what you’re talking about. It helps minimize mistakes and get be updated over time.

Interesting! Although some of the investors may have jumped in and out of funds not just because they were trying to market time, but also because they needed the money during the recession etc.

I’m not totally clear, though, on how the “investor return” can actually exceed the “investment return” for the 2045 fund. What is clear, though, is that by comparison with the other funds, staying fully invested over the long term is more profitable, even if those absolute percentages are not quite achievable.

You’re right. There’s no perfect way to calculate these numbers, but a large gap tells you that something’s up. Basically if more money poured into the targetdate fund when it was down in 08-09, the investor return would be much better because the returns are calculated on a dollar weighted basis. On the other hand, if investors poured a ton of cash in at the prior top in 2007 or pulled out a bunch of money at the bottom in 2009, the investor returns would be much worse. It picks up the broad trend, but not each decision.

Read here for a more in depth rundown on how they calculate these numbers:

http://www.verisi.com/resources/dollar-weighted-returns.htm

Thanks, will do!

[…] Behavior trumps investment strategy. (A Wealth of Common Sense) […]

[…] Complicated Than They Look (Motley Fool) • Buffett’s Fourth Law of Motion: Your Behavior (A Wealth of Common Sense) • The US is nowhere near another housing bubble (Quartz) see also The Tale of a House, and an […]

[…] Buffett’s Fourth Law of Motion: Your Behavior (A Wealth of Common Sense) […]

A systematic approach can definitely help enforce discipline, but only as long as the person using the system maintains confidence. I think most people overestimate their capacity to withstand pain. When faced with the reality of the inevitable downswing that every investment approach has (Fairholme is a great example), they lose confidence and chase something else.

Understanding your own psychology is as important as understanding your investment approach.

Well said. If you look back at diversified buy, hold & rebalance portfolios historically the numbers are great. It just takes one or two cycles of fear and greed to ruin things.

I think one of the most important things I’ve learned it that when you’re dealing with financial markets, everything is cyclical. Thinking things will only get worse or only get better is probably the biggest mistake investors make on a consistent basis.

I’m in complete agreement with you that the behavioral elements are by far the most important piece of the investment puzzle.

Thanks for the comment.

[…] recent article in A Wealth of Common Sense, which you can read here – https://awealthofcommonsense.com/behavior-investment-strategy/ – delves into Warren Buffet’s Fourth Law of Motion: Investor […]

[…] Behavior trumps investment strategy. (A Wealth of Common Sense) […]

[…] I showed last week (see Buffett’s Fourth Law of Motion), simple investment strategies often produce the best results from actual investors. This is […]

[…] you forget Buffett’s Fourth Law of Motion, which states that ‘returns decrease as motion […]

[…] As many in the finance industry have pointed out (myself included), behavior still matters. […]

[…] But there are still simple options out there for investors that are afraid of the typical Wall Street huckster. In your workplace retirement plan you can choose a targetdate fund until you become comfortable building your own portfolio (this also reduces the behavior performance gap). […]

[…] A Wealth of Common Sense – Buffett’s Fourth Law of Motion; Your Behavior. […]

[…] the funds or securities they hold, regardless of whether they’re index funds or active funds. As Buffett’s Fourth Law of Motion states, “For investors as a whole, returns decrease as motion […]