Many consider the gains seen in the stock market since 2009 the most hated bull market of all-time. As they say, stocks climb the wall of worry, and people have been mighty worried about pretty much everything over the past seven years or so. But it’s getting harder and harder to correctly judge sentiment anymore these days. There are more opinions out there because of the Internet, more financial news publications and more noise than ever.

When considering market sentiment it always makes sense to watch what people do, not what they say.

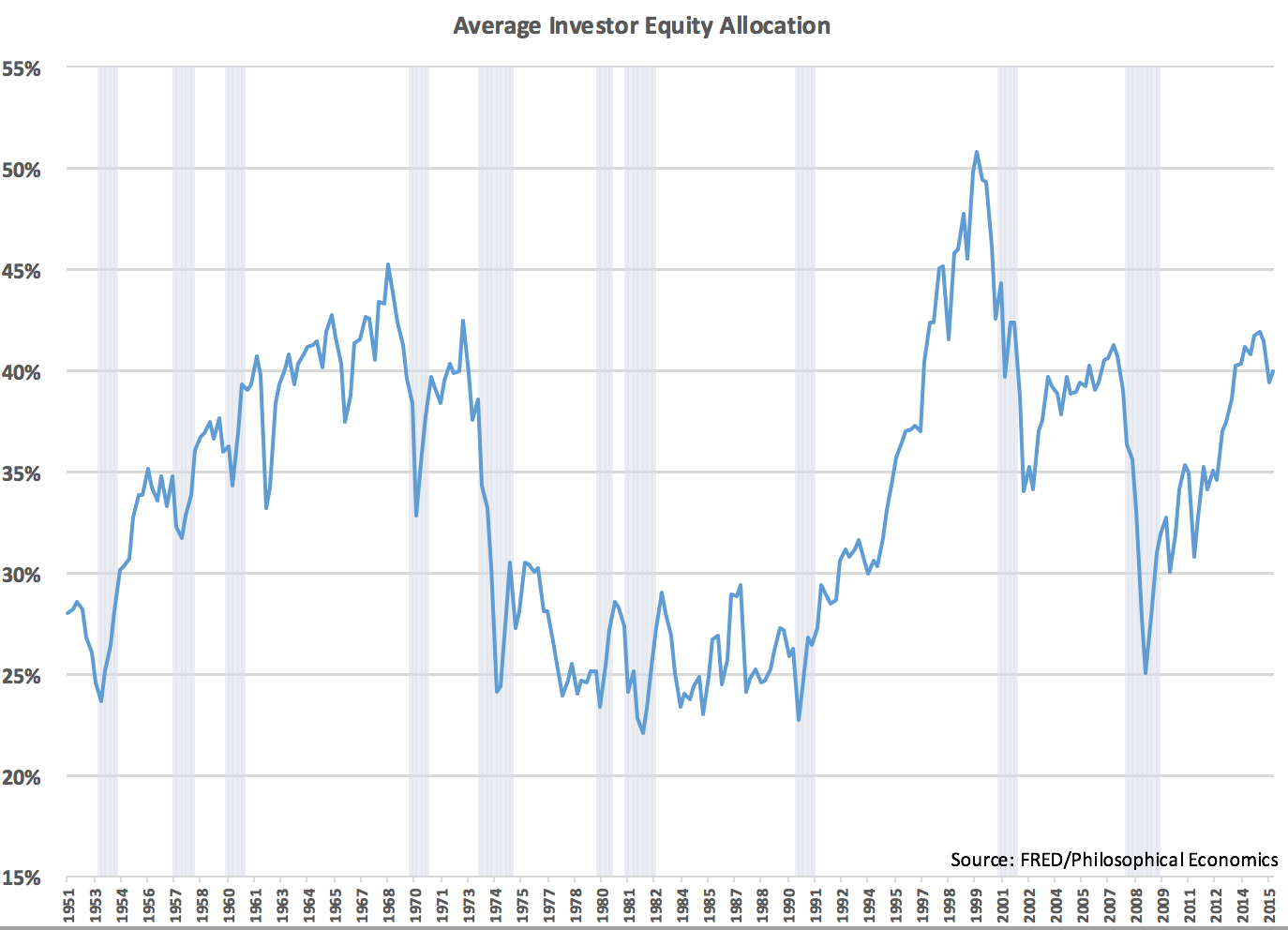

Investors may not like it, but they do own more stocks. The average investor equity allocation is now back to where it was around the 2007 market peak:

This has some people worried that things are getting frothy once again. Maybe they are, but there are some legitimate reasons for the increase in equity allocations by households. Here are seven of them:

1. Low savings rates. Lots of people out there have very little saved for retirement. The only ways to remedy this situation are to save more money, work longer, lower your standard of living or take more risk. Many investors need to take more risk in their portfolios to try to make up for a perceived shortfall. This can be a risky proposition for those who can’t handle the additional volatility this strategy brings, but for many they see stocks as their only refuge.

2. Low interest rates. There’s nowhere safe to hide for high quality income needs in today’s low rate world. The days of 5-6% Treasury yields are behinds us for now. The S&P 500 yields over 2% in dividends while the 10 Year Treasury yield is under 1.8%. These are two very different investment structures but many investors need to accept more risk for both higher yields and higher returns if they wish to accomplish their goals.

3. People are living longer. The odds of at least one person in a male-female couple reaching age 75 is around 90%. There’s an 80% chance at least one will live to 85 and a 40% chance one will survive to age 95. In the past people used to retire in their 60s and die in their 60s. Now people are living longer than ever. Many people will have an additional three decades or more in retirement without earning a working wage. Inflation can eat up a lot of your returns over 30 years, so people realize they need to get some growth in their portfolios if they wish to not outlive their money.

4. Financial advisors. There is now close to $2 trillion being managed by registered independent advisors (RIAs). Many of these advisors along with their hybrid broker/advisor counterparts are now using strategic asset allocations for many of their clients. That means more money in stocks, for the most part. This trend will likely continue.

5. Target Date funds. Target date retirement funds continue to be under-appreciated by many for the shift in investor allocations. These funds hold three-quarters of a trillion dollars and continue to grow at a nice clip because they are now the default fund selection for workplace retirement plans. Auto enrollment has been a huge source of inflows for these funds. Many savers who would have kept their retirement money in a low interest stable value fund in the past are now automatically invested in a target date fund and more diversified than they ever would have been on their own. They’re not perfect, but I believe these funds have been a huge net positive for the typical retirement saver who knows nothing about the markets or portfolio management.

6. It’s easier to own stocks now. I covered this a few weeks ago — we now have better technology, with lower costs, more access to the markets and more options than ever before to invest your savings. There’s no more phone calls with your broker to place a trade as people can now do it from their smartphone if they so choose. Mutual funds and ETFs also make it easier than ever to build diversified portfolios with as little as a single fund holding.

7. Stocks have tripled. Shouldn’t we expect a higher allocation to equities after they have a huge run? When one asset class performs much better than the other asset classes you would expect that allocation to rise. And rising stocks also attract buyers who initially missed out on the fun. So it makes sense that equity allocations would be rising for the simple fact that stocks have been rising.

None of these reasons for the increase in equity allocations mean that stocks can’t or won’t fall from these levels. They certainly can and will. But I also think that people need to recognize that the structure of the markets and the structure of people’s lives will likely lead to a higher allocation to equities than most would have required in the past. There will be some unintended consequences from this shift in allocation preferences for sure, but I would assume that it will be here to stay for the foreseeable future, even though it will fluctuate along with the market.

Further Reading:

Seeing Both Sides of the Market Debate