A reader asks:

My wife and I are both 50 and we retired from our jobs about three years ago. We’ve been living off our investments. However we were harshly reminded in 2022 of the impact of volatile returns vs. smooth returns when drawing upon the principal. I am a bit of a spreadsheet warrior and have run many models going out 50 years. I assume a 2.25% inflation rate, and a composite 15% tax rate which I hope to manage even lower. Our assets excluding our home are about $4.4M broken down as 60% taxable/liquid, 35% in IRAs and 5% in Roths. Our only debt is a 2.1% mortgage that will be paid off in 10 years. You’ve often said: “When you’ve won the game, you stop playing” which I probably need to shift to more than my current “in for a dime, in for a dollar” approach. I am considering perhaps going “all-in” on JEPI or a similar investment(s) with my ideal scenario being 5-6% yield plus 1-2% annual appreciation. Drawing from principal during market downturns would have minimal impact, and this math would work really well for me until age 59.5 and beyond. Other than market declines in the principal, I am trying to think about other risks I may not have considered and alternatives to this approach. The wild swings created by adjusting +/- 50 bps in long term returns are incredible with compounding.

I too am a spreadsheet warrior.

I made my first retirement spreadsheet right out of college.

I made a bunch of assumptions about savings rates, market returns, asset allocation, etc. That was roughly 20 years ago.

None of it played out like that retirement spreadsheet. Spreadsheets are linear but life is lumpy.

That doesn’t mean you should forgo the spreadsheets altogether. Setting expectations is an important part of the financial planning process. You just have to go into that process with the understanding that any multi-decade investment plan involves guesswork that needs to be updated as reality plays out.

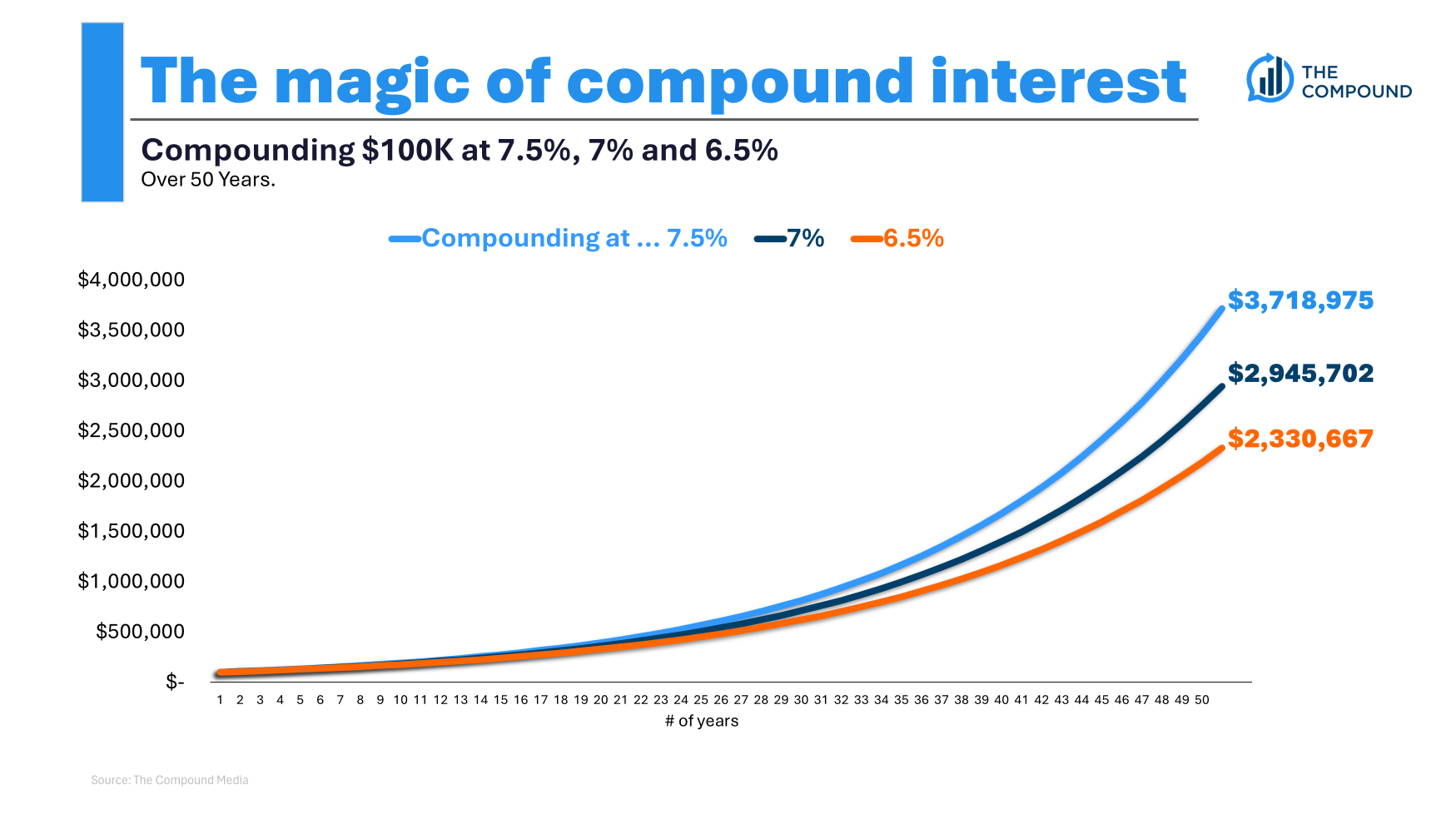

This reader is correct in stating that 50 basis points here or there can make a big difference over 50 years. This is a simple chart that shows the growth of $100k over 50 years at different annual return levels:

A 7.5% annual return would net 26% more than 7%. But if you went from 7% to 6.5%, now you’re down more than 20%. Jumping from 6.5% to 7.5% would mean nearly 60% more wealth over 50 years!

Obviously, there are a bunch of other assumptions you could make here about savings rates, withdrawal rates, tax rates, inflation rates, etc.

One of the hardest things about financial planning for us spreadsheet people is the fact that you have to throw precision out the window.

Your initial plans never come to fruition. Your expectations are almost always going to be too high or too low. That’s true over 50 years or 5 years or 5 months.

Now that we got that out of the way let’s dig into some of the other details here.

Bear markets often act as a wake-up call. There is nothing wrong with wanting more stability to survive early retirement. Sell-offs are never easy, but during retirement, those downturns are even scarier.

Young people have time, income and human capital at their disposal to wait out bear markets and lean into them by buying at lower prices. Retirees don’t have that same luxury.

I have mixed feelings about what happens once you win the game when it comes to investing.

On the one hand, it seems silly to put your capital at risk during retirement when you’ve already saved enough money. You don’t have the income or time to see you through a bear market like young people do.

On the other hand, when you retire in your 50s, you could have 30+ years to grow and compound your money. Plus you have inflation to contend with.

The biggest problem with an “in for a dime, in for a dollar” approach (which I assume means taking more risk) is you don’t want to sell your stocks when they’re down.

Covered call strategies can serve a purpose in a portfolio.1 They can offer lower volatility than the market and higher income.

But this seems like trading one in for a dime, in for a dollar strategy for another. I’m just not a fan of going all-in on anything, especially in retirement.

These are just some of the risks you have to contend with in retirement:

- Longevity risk (running out of money)

- Inflation risk (seeing a lower standard of living)

- Market risk (bear markets)

- Interest rate risk (fluctuations in yield or outright bond losses like we saw in 2022)

- Sequence of return risk (you get poor returns at the outset of retirement)

And those are just portfolio management-related risks. You also have to contend with health risks, unforeseen expenses, family issues and life getting in the way of your best-laid plans.

Your two best forms of risk management in retirement are diversification and flexibility with your plan.

Every strategy comes with trade-offs. Unfortunately, there is no investment panacea that offers 100% certainty during retirement.

Maybe it’s time to bring in a financial advisor so you can enjoy your winnings without stressing too much about the next bear market.

We tackled this question on the latest edition of Ask the Compound:

The Roth Man himself, Bill Sweet, joined me on the show this week to discuss questions about taxes in marriage, retirement withdrawal strategies, the tax implications of selling farmland and how to manage tax rates in early retirement.

Further Reading:

How Much Money You Need For Retirement

1We’ve talked about JEPI on Animal Spirits in a past Talk Your Book episode with the portfolio manager of the strategy — Hamilton Reiner. Listen here.