Apparently June is the month to call a bubble if you’re a seasoned fund manager or prognosticator.

Meb had Jim Grant on his podcast last week calling AI one of the greatest bubbles of all-time:

Jim Chanos says the AI capex is bigger than the dot-com bubble:

Jeremy Grantham loves calling for another bubble:

So does Ray Dalio:

I received a question this week about Dalio’s latest market musings:

OK, Ray Dalio is worth over $20B. So he knows something, that’s for sure. A lot of people certainly believe in his thinking. Not saying he is wrong, but are you down with his current thinking, or at least some of it?

This is in reference to a few things Dalio has written in recent weeks:

Market and economic concentration is in one new sector that is highly volatile and risky–and is super-popular among unsophisticated investors. That’s classic bubble stuff.

While it is indisputable that the risks are high, I am now going to give you an opinion, which could be wrong, that the prospective returns are low. That assessment of prospective future returns is based on my analytical work related to valuations and my bubble indicator’s readings: the real returns in equities over the next 5 to 10 years look to be about -5 to -10%, though there is considerable uncertainty around those numbers.

All of this sounds kind of scary.

Maybe they’re all right. Maybe this is a gigantic bubble that’s ready to burst. Maybe we get a lost decade. Maybe stock market returns are terrible from here.

These things have all happened in the past and will likely happen again at some point in the future. Risk assets are sometimes risky.1

Listen, Dalio is very intelligent. He’s extraordinarily rich. He’s made many Bridgewater investors rich too. The guy essentially saved McDonald’s Chicken McNuggets back in the 1970s (look it up).

However, even legendary investors like Ray Dalio have a hard time predicting these things in advance.

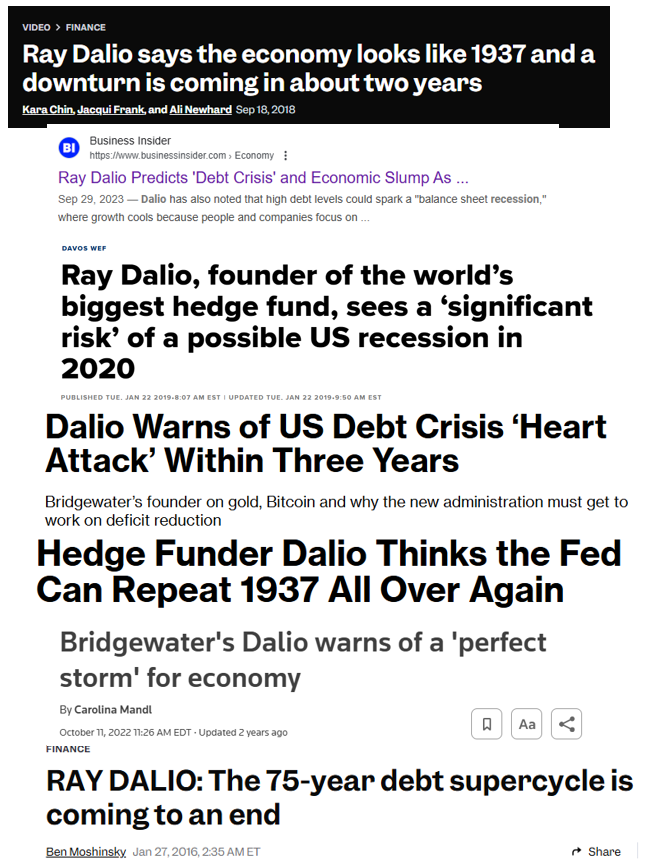

He’s been making dire warnings for well over a decade now and none of those warnings have come true:

Grantham too:

Spotting bubbles and calling tops is hard, even for legendary fund managers.

The thing is that hedge fund managers, newsletter writers and the like have to make predictions about financial crises, bubbles and stock market valuations. It’s in the job description or something.

The financial media is always taking a stab at this stuff too:

Everyone knows when we’re in a financial crisis or crash. No one ever knows for sure when we’re in a bubble until after the fact.

AI might in fact be a bubble right now. It certainly checks a lot of the boxes.

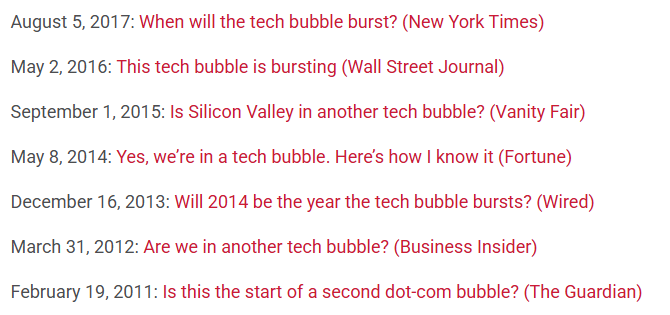

But it’s also worth pointing out the fact that people have been calling tech a bubble for a very long time now.

I wrote something all the way back in 2017 about the many tech bubble calls that proved to be wrong:

Anything before the pandemic feels like a hundred years ago but this was a long time ago!

Does that mean this isn’t a bubble? Of course not. It might be!

I just don’t like the idea that you have to call bubbles and market tops to be a successful investor. The pundit graveyard is full of market top calls that were unfulfilled.

I’ve interacted with thousands of wealthy people over the years through my writing and time working in wealth management. I’ve yet to meet one person who told me they got rich picking tops and calling bubbles. It sounds exciting but it’s not necessary.

And the people that get one right are usually right once in a row and spend the rest of their career chasing the thrill of predicting the next top.

It’s a fund manager pipe dream.

I’m sure someone will “call” the next top through some combination of skill and luck. They may even profit from it.

But they won’t be able to do it on a consistent basis.

No one can call tops on a consistent basis.

Build a durable portfolio that can see you through tops, bottoms and middles.

That’s the best you can do.

Further Reading:

Is This a Bubble?

1That’s part of the message in Risk & Reward.