Goldman Sachs has a report out called the New Economics of Retirement with survey results from interviews with working and retired Americans across generations and wealth levels.

There’s some data in here that stands out.

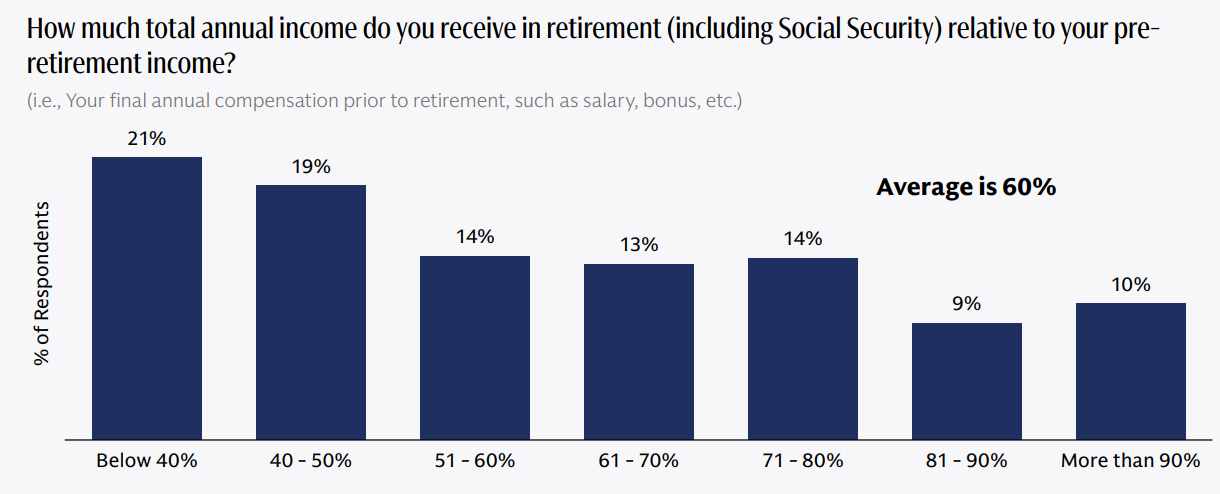

For example, they asked retirees what percentage of pre-retirement income they are living on during retirement:

The average is 60%, which makes sense since you often need less income during retirement. No more payroll taxes. You don’t have to save money anymore. Work-related costs, such as commuting, go away. And many retirees have their homes paid off.

This is one of the reasons you probably need less money saved up for retirement than you think.

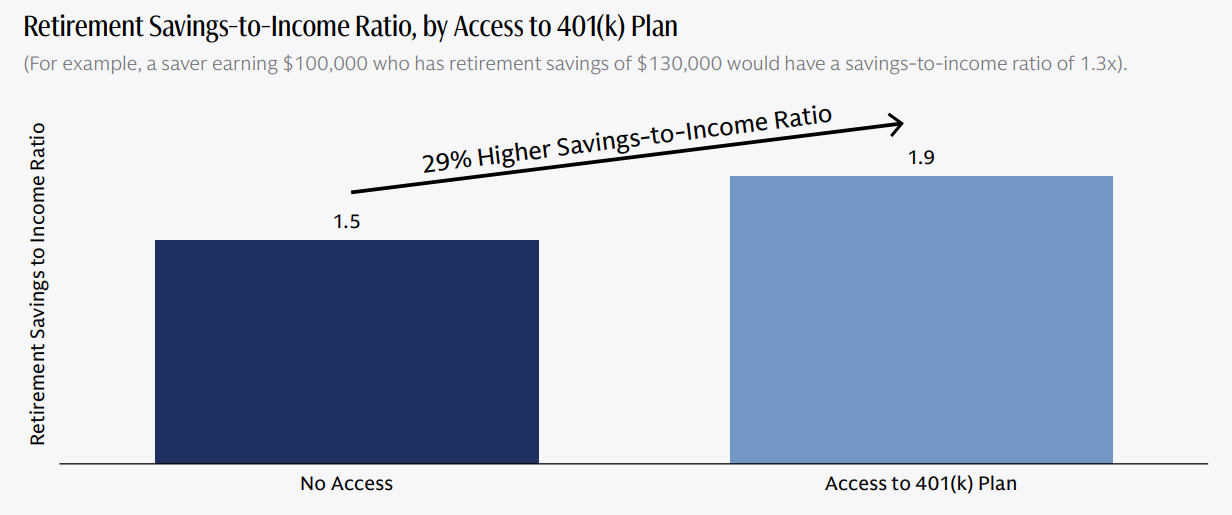

This chart is obvious but also interesting:

People with access to a workplace retirement plan have a higher savings-to-income ratio. This is why the government should do everything it can to give every worker who wants it access to a tax-deferred workplace retirement plan.

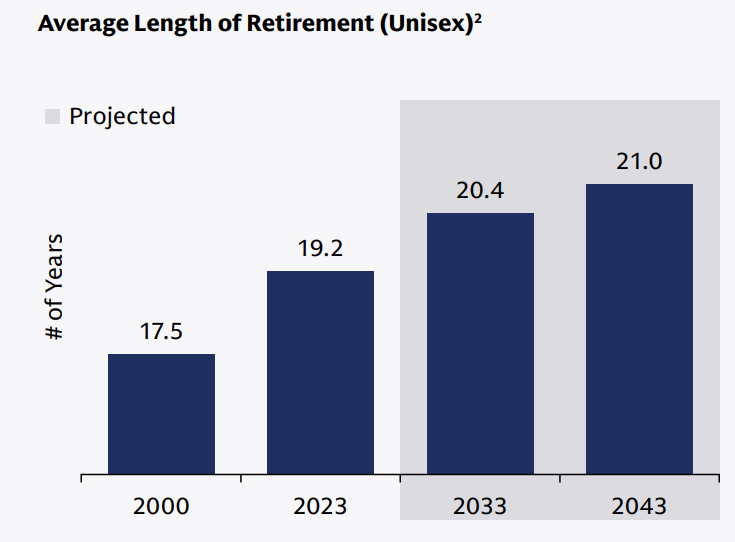

It’s also worth noting that people are living longer in retirement:

This will have ramifications for how much risk retirees need to take, the timing of inheritances (later than you think) and an increased need for financial advice in the years ahead.

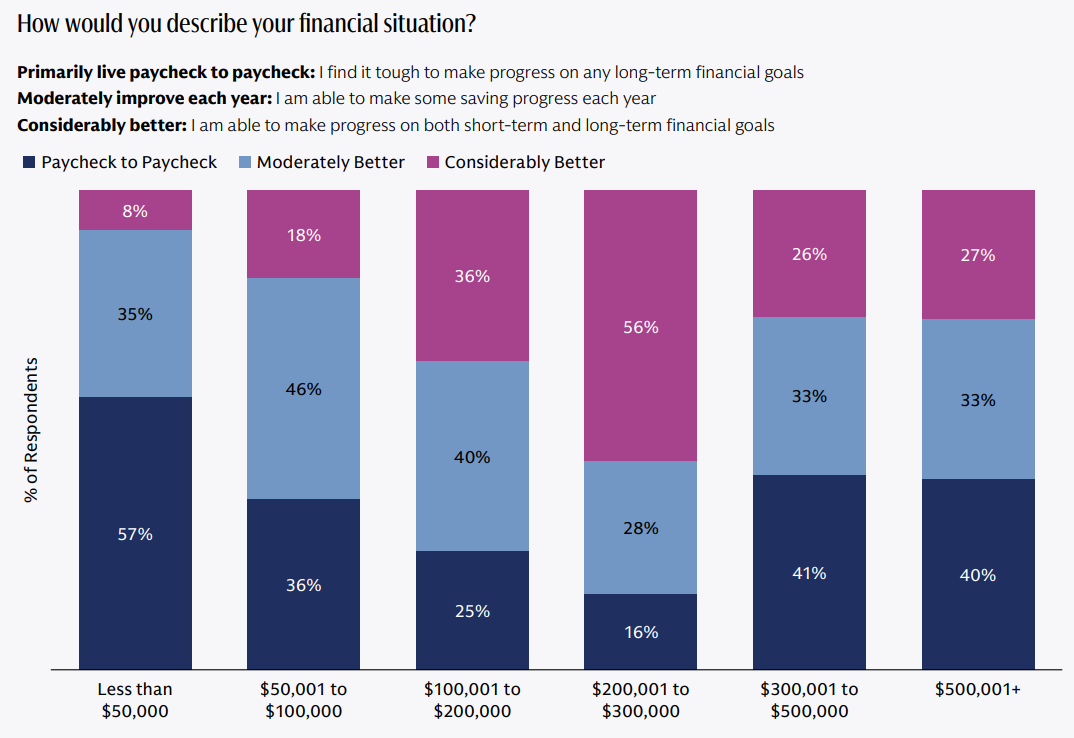

Now for the real eye-opener:

This chart shows that 41% of households earning $300k to $500k live paycheck to paycheck. And 40% of households earning half a million dollars or more live paycheck to paycheck!

Anyone with a personal finance brain will take one look at these numbers and immediately lecture you about lifestyle creep.

It doesn’t matter how much money you make. If you spend more than you bring in, you’re never going to get ahead.

That’s sound financial advice that I wholeheartedly agree with.

But that’s not going on here.

It’s ridiculous to believe 40% of people making half a million dollars live paycheck-to-paycheck. Making $300k a year puts you in the top 3% of wage earners. If you make $500k a year you’re in the top 1%.

Come on! Paycheck-to-paycheck?! No.

So what’s the real story?

Three things.

1. Social media. I am not a Luddite. Technological innovation is one of the biggest reasons we have experienced so much progress as a species for the past few hundred years or so:

Having said that, social media was probably a mistake.1

Keeping up with the Joneses used to be your peers, neighbors, and co-workers. Envy existed but it was relatively contained. Now you’re constantly inundated with people flaunting their wealth, spending, vacations, material possessions, investments and more every single day.

Social media is full of influencers, billionaires, grifters, and people who craft fake lives that are meant to make you feel like you don’t have enough money.

Our brains were not meant to be bombarded with this much information about how certain people in society live.

This is how we have so many rich people who don’t feel rich.

2. Surveys. In his book Everybody Lies Seth Stephens-Davidowitz doesn’t hold back:

People lie about how many drinks they had on the way home. They lie about how often they go to the gym, how much those new shoes cost, whether they read that book. They call in sick when they’re not. They say they’ll be in touch when they won’t. They say it’s not about you when it is. They say they love you when they don’t. They say they’re happy while in the dumps. They say they like women when they really like men.

People lie to friends. They lie to bosses. They lie to kids. They lie to parents. They lie to doctors. They lie to husbands. They lie to wives. They lie to themselves.

And they damn sure lie to surveys.

It’s not necessarily that everyone is lying but you have to watch what people do not what they say.

You also have to look into the actual questions asked on surveys. Look more closely at how Goldman defines living paycheck-to-paycheck:

I find it tough to make progress on any long-term financial goals.

That’s not living paycheck-to-paycheck! Making progress on long-term financial goals can be difficult because you don’t see results in the short-term! This is also a subjective definition because different people have different long-term financial goals.

What if your long-term goals are to own a private jet even though you’re maxing out your 401k? Does that mean you’re living paycheck-to-paycheck?

The other reason you should be dubious of most financial surveys right now is because the vibes are broken.

Why?

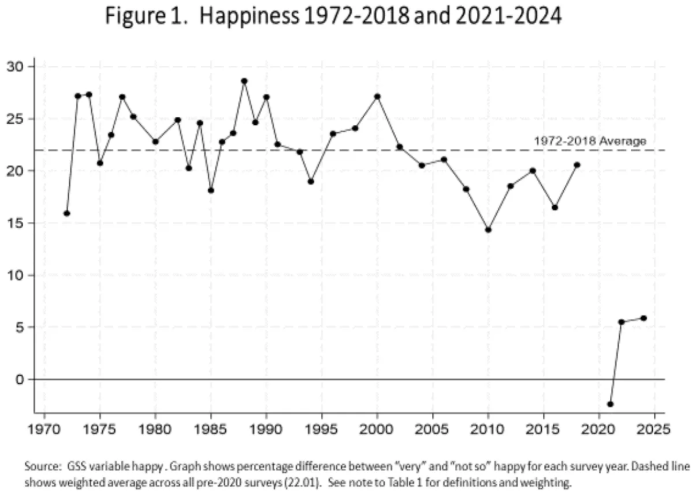

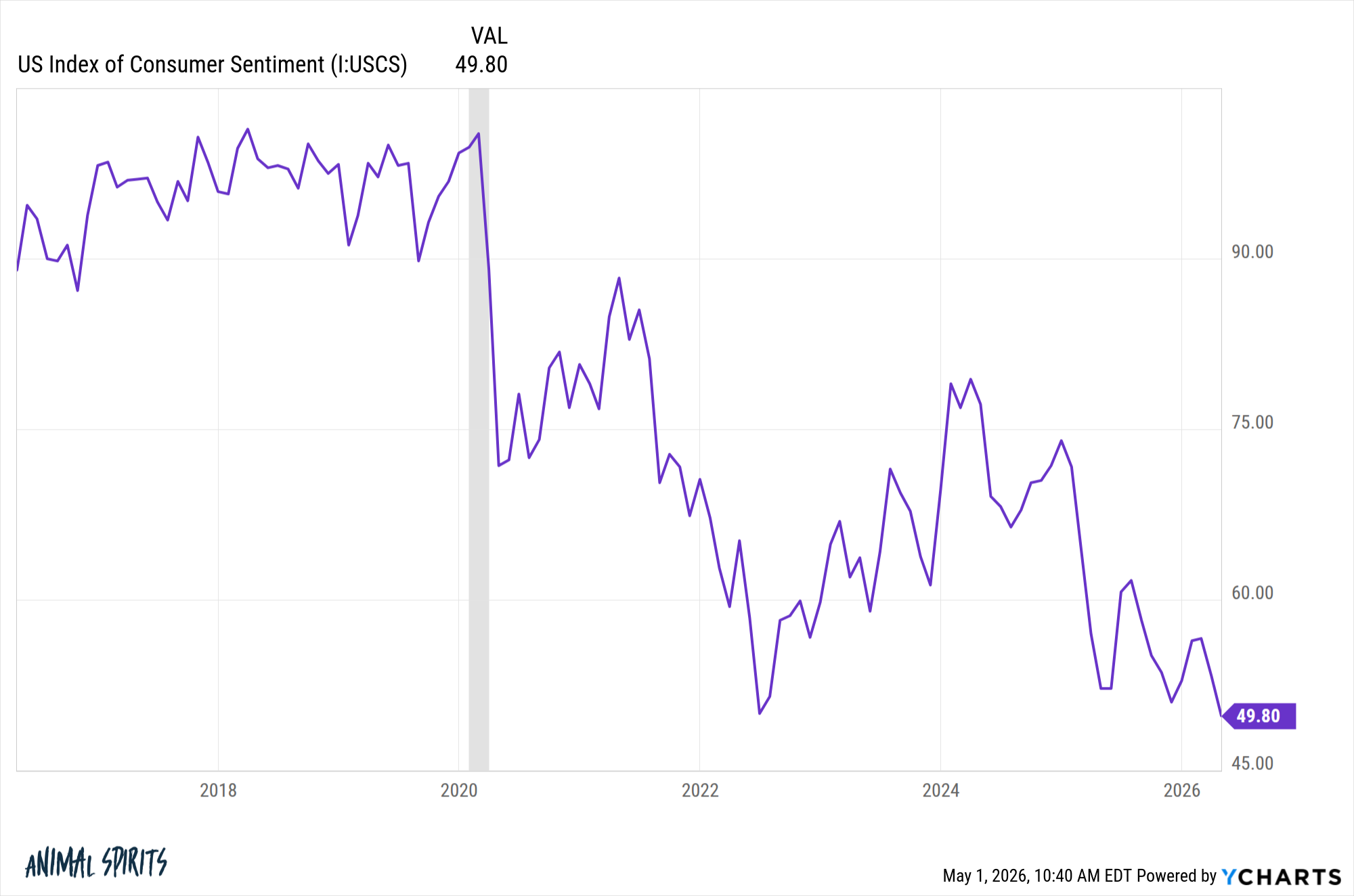

3. The pandemic. Derek Thompson wrote a piece about wealth and happiness with a chart that shows how dramatically the pandemic impacted our collective feelings:

Look at consumer sentiment:

Covid caused a happiness cliff that we still haven’t recovered from. And it’s causing some weird responses to financial surveys.

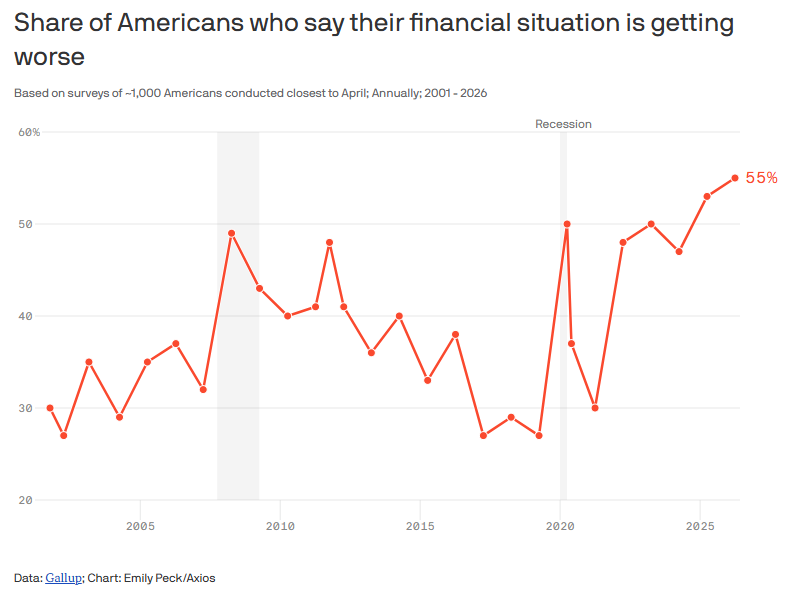

Here’s another one from Gallup via Axios:

The share of Americans who say their financial situation is getting worse has never been higher this century.

Worse than the Great Financial Crisis?! Are you kidding me?!

I lived through the 2008 financial crisis. The financial system nearly imploded. The stock market was down almost 60%. The unemployment rate reached 10%. No one could get a raise. You felt lucky to have a job. Businesses went under. It was scary times.

We’re not in a recession right now. The unemployment rate is low. Americans are richer than ever before. The stock market is at all-time highs.

I feel like I’m taking crazy pills! Or maybe everyone else is.

Obviously, the economy is not perfect. It never is. Inflation is painful for many households. Some households are doing better than others.

But please don’t believe every survey you read.

Watch what they do not what they say.

Michael and I talked about living paycheck-to-paycheck, surveys and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

The Super Rich

Now here’s what I’ve been reading lately:

- Nike and the arithmetic of durability (Toward Evergreen)

- Why most people never make it (The Write Path)

- Friction is a feature (Educated Guess)

- Lessons from 500 blog posts (Of Dollars & Data)

- Existential uncertainty (Abnormal Returns)

Books:

1And I say this as someone whose career has benefited from social media in many ways.