Widespread tariffs are a bad idea.

How do I know this?

History shows they don’t work.

Let’s look back.

JP Morgan’s Michael Cembalest wrote about President McKinley’s disastrous tariffs in the late-1800s:

President William McKinley tariffs were very popular at the time they were enacted, but they caused an almost immediate inflation spike. Voters were very unhappy: a few months later, the GOP lost 100 seats in the 1890 midterm elections. The GOP loss in 1890 is the third largest in the history of the House going back to the Civil War.

Sounds great in theory but not so much in practice.

I first learned of tariffs from Ferris Bueller’s Day Off:

Those didn’t work either.

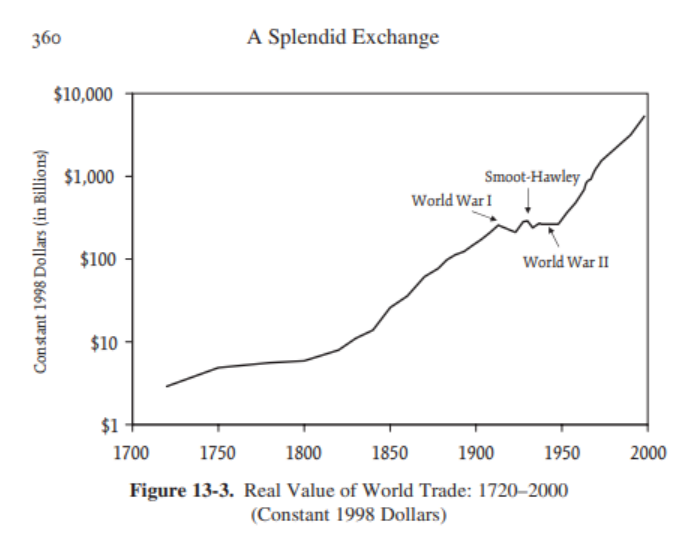

A Splendid Exchange by William Bernstein is the best book about the benefits of free trade.1 Here’s a passage about the Smoot-Hawley tariffs that were enacted in the 1930s:

All over the world, for three years after the passage of Smoot-Hawley in 1930, as French lace, Spanish fruit, Canadian timber, Argentine beef, Swiss watches, and American cars slowly disappeared from the world’s wharves. By 1933 the entire globe seemed headed for what economists call autarky–a condition in which nations achieve self sufficiency in all products, no matter how inept they are at producing them.

This was the outcome:

Between 1930 and 1933, worldwide trade volume fell off by one-third to one-half. Depending on how the falloff is measured, this computes to 3 to 5 percent of world GDP, and these losses were partially made up by more expensive domestic goods.

You can see the fall off in trade during this period of isolation:

The Great Depression played a big role here, too, obviously, but a trade war made it worse. Isolationism and protectionism were also partly to blame for World War II.

Following WWII nations around the globe opened up trade. In 1929 Americans spent 24% of their income on food. Today it’s more like 10%. This is a benefit of free trade.

Obviously, the world is a different place now than it was in 1890 or 1929. I actually think some targeted tariffs on a country like China could make sense to protect certain industries in the United States from our economic rival.

However, universal tariffs will cause unnecessary economic pain for businesses and consumers alike.

But won’t this bring back manufacturing and jobs to America?

No. Cullen Roche explains:

Manufacturing has fallen from 40% to 7% of US employment since 1950 and robotics will decimate the remaining 7% in the next 50 years. Those jobs aren’t coming back and trying to turn the most advanced technological economy in the world back into an emerging market manufacturing economy is backwards thinking.

Americans will have fewer choices because the government reduced competition and consumer options. This will drive UP prices. Especially when US firms realize they have more pricing power due to the government’s manipulation of the market.

An advanced economy shouldn’t want to go backward. It makes no sense. Joe Weisenthal explains:

One way to think about any relatively open trading bloc is that by allowing more specialization and focus, the economy can build out more complex market objects. If you want to have autarky in America, you could probably do it, but good luck building out any advanced, complex industry, with so many resources dedicated to manufacturing kitchen mitts or microwaves.

Even if you agree with tariffs as a policy idea the implementation here is worse than how the Mavericks traded Luka to the Lakers. You can’t possibly expect global corporations or small businesses to change their supply chain and manufacturing capabilities on the fly like this. You can’t do that overnight.

It’s economic suicide.

Based on the White House’s numbers, businesses will pay upwards of 40%, 50%, or maybe 60% in tariffs. Corporations will try to cut costs like crazy, which means lots of layoffs are likely coming.

This is not sustainable.

The hope is that there will be negotiations and that these rates will come down drastically. If they don’t, a recession has to be the baseline expectation in a trade war like this.

The outcome here feels binary.

While not exactly the same scenario, this situation reminds me a lot of the story from Art Cashin about what he learned from a more seasoned investor about navigating the Cuban Missile Crisis:

Professor Jack was already in the bar, and I came bursting through the doors as only a 19- or 20-year-old could. And I said, ‘Jack, Jack. The rumors are that the missiles are flying.’

And he said, ‘Kid, sit down and buy me a drink.’

And I sat down and he said, ‘Listen carefully. When you hear the missiles are flying, you buy them, you don’t sell them.’

And I looked at him, and I said, ‘You buy them, you don’t sell them?’

He said, ‘Of course, because if you’re wrong the trade will never clear. We’ll all be dead.'”

If Trump and team keep these ridiculously high tariffs we’ll all be dead in a manner of speaking. It will eventually nuke the economy.

Markets are in a freefall but they will be fine. The stock market has been through worse than this in the past. Stocks will come back at some point.

I’m more worried about the economic ramifications. A lot of people are going to be in a world of pain if this continues.

Michael and I talked about tariffs and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

The Wealth Effect

Now here’s what I’ve been reading lately:

- The keys to happiness (Psychology Today)

- You know nothing (Morningstar)

- Pineapple Suite state of mind (Money with Katie)

- What to do in chaotic markets (Discipline Funds)

- An oral history of Good Will Hunting (Boston Magazine)

Books:

1Here’s a free chapter about tariffs and trade wars that is worth reading.