A reader asks:

There is a lot of data on the probability of positive returns for different time periods (S&P 500). Does anyone have similar data for different portfolio allocations? 60/40 stocks/treasuries, etc.

This one is right in my wheelhouse.

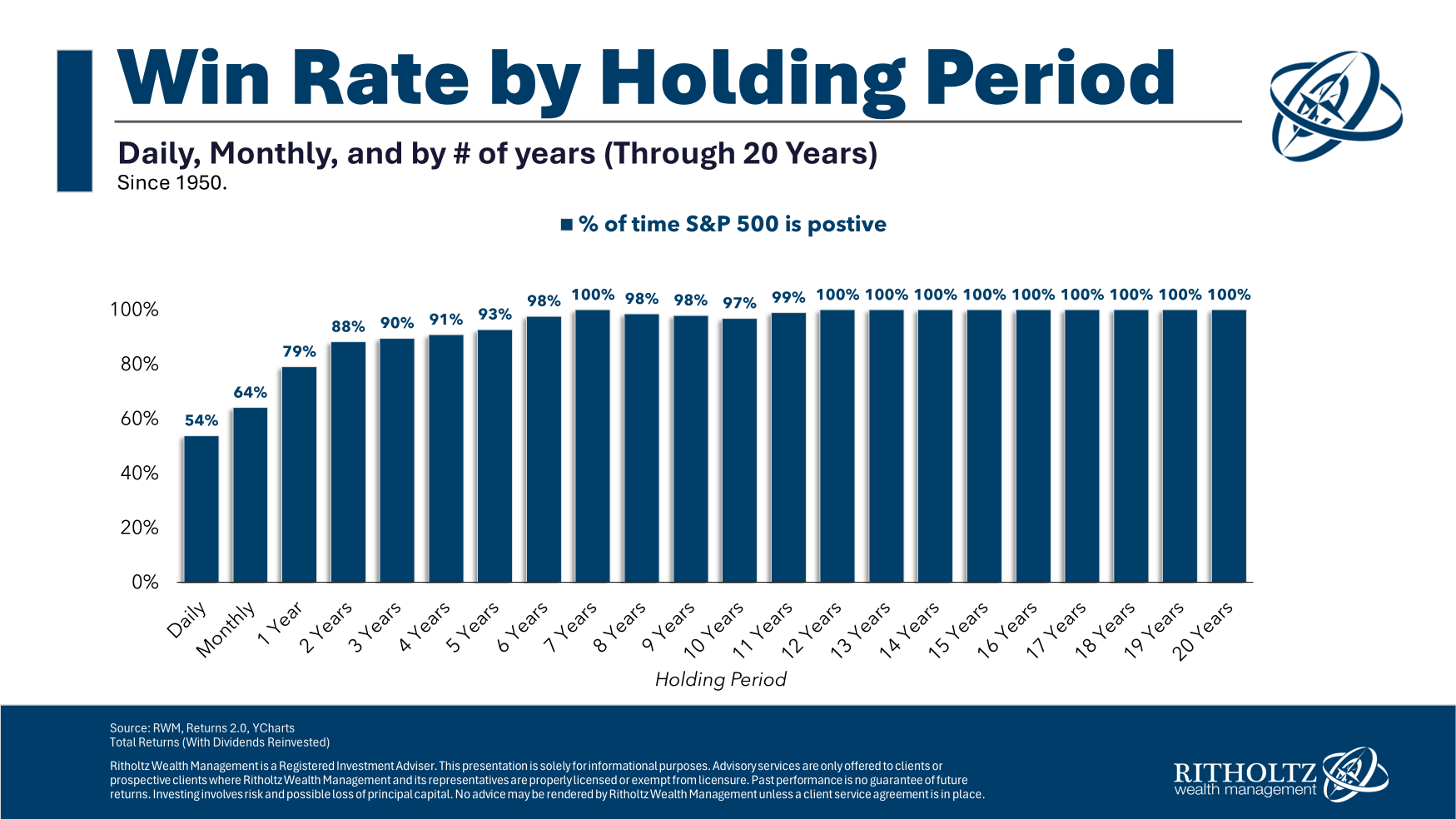

As a staunch advocate for long-term investing, I love the charts that show the win rates for the stock market over various time frames:

This is one of my all-time favorite stock market charts.

The historical win rates for international stocks are similar.

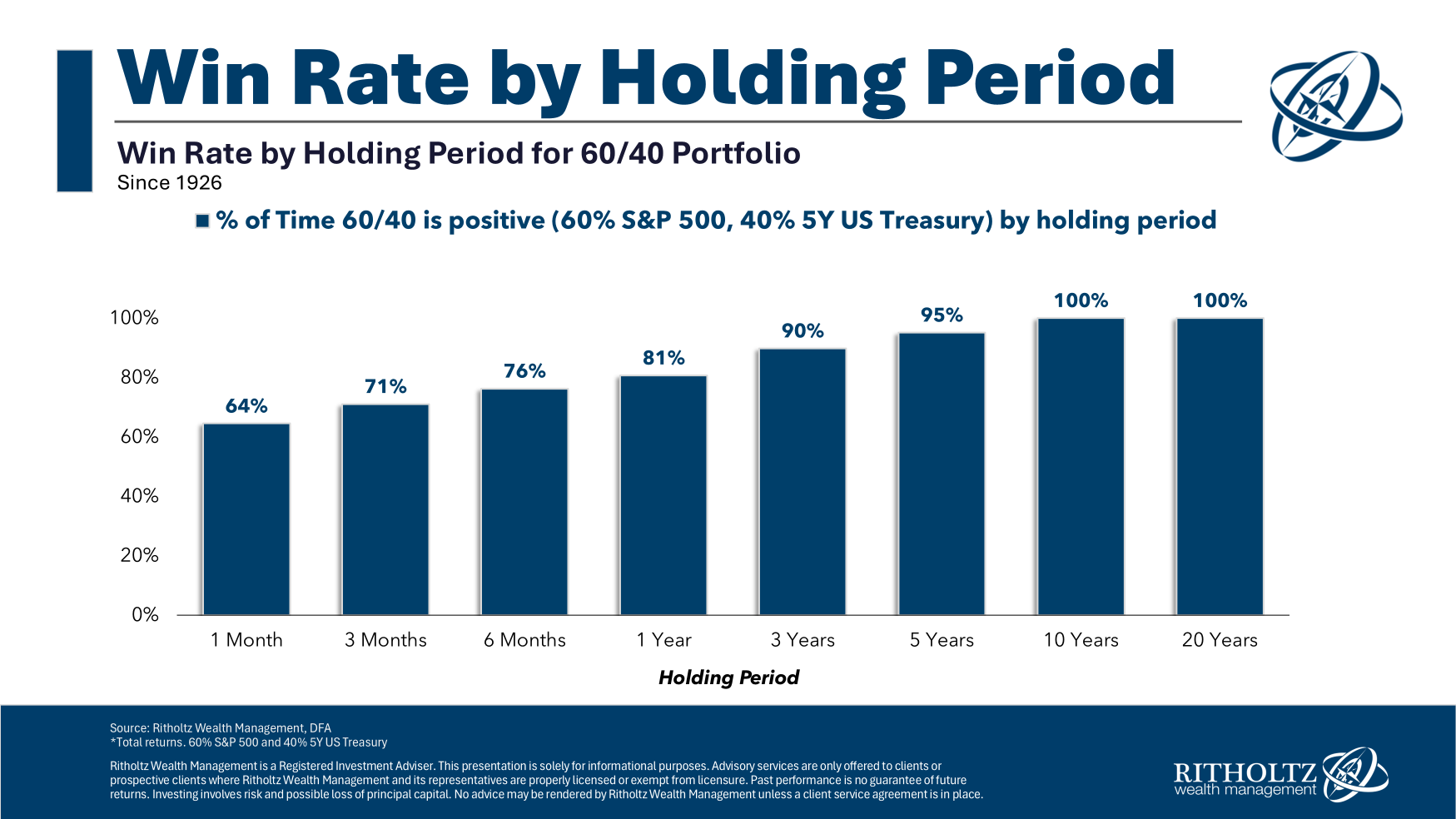

But I’ve never done this exercise for a diversified portfolio.

Let’s get to the data!

I looked at a diversified portfolio using 60% in the S&P 500 and 40% in 5 year Treasuries going all the way back to 1926:

That’s pretty, pretty good.

The monthly numbers are the same as the stock market while the 1 year, 3 year, 5 year and 10 year win rates were slightly better for a 60/40 portfolio.

In the history of this data, there has never been a negative 10 year return for a diversified mix of U.S. stocks and bonds. That’s a phenomenal track record.

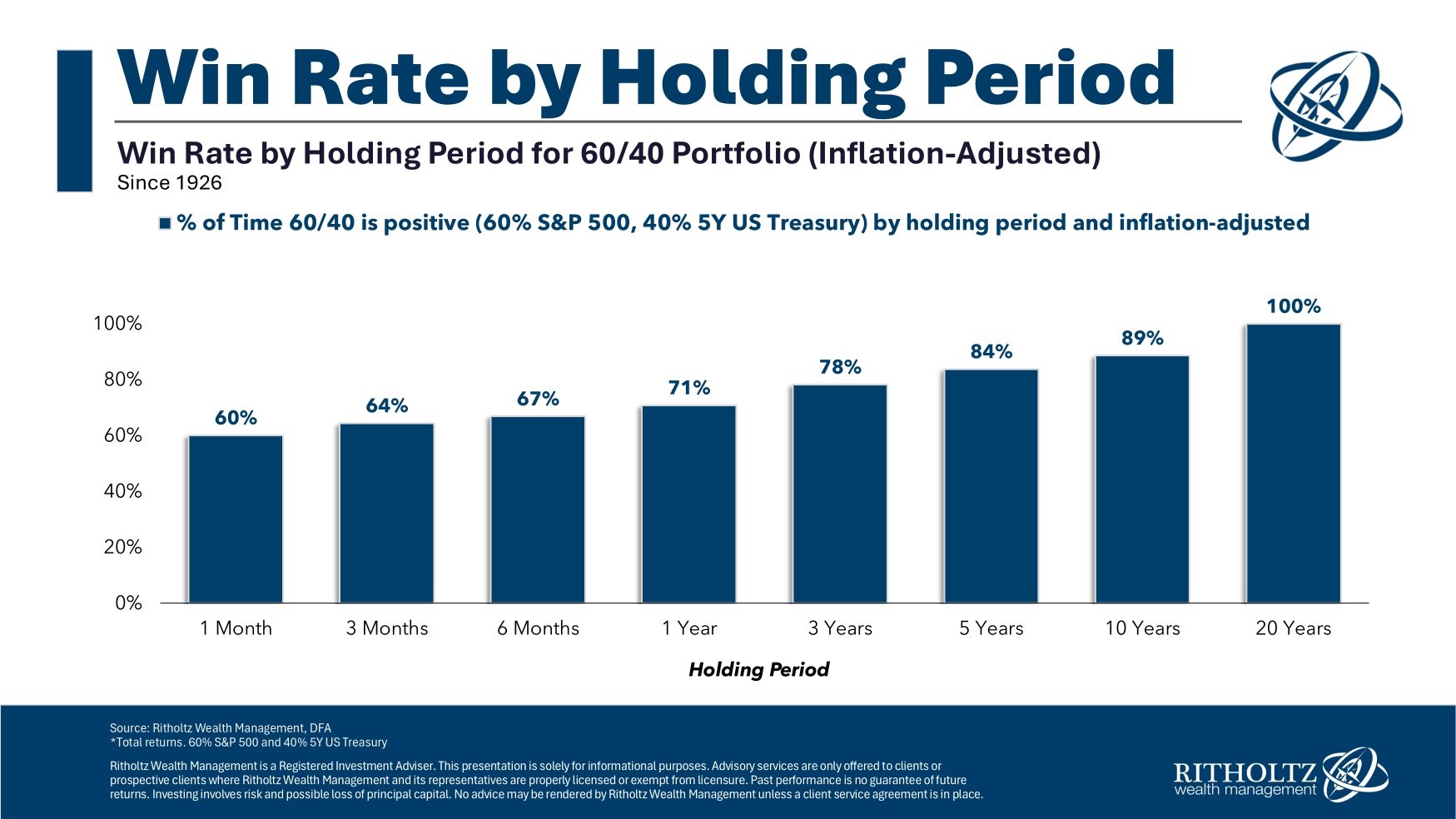

The biggest pushback I typically receive when producing these kinds of charts is the lack of an inflation adjustment.1

For all of the real return people, here are the inflation-adjusted win rates over the same holding period for the same 60/40 portfolio:

That knocks things down a little bit but it’s in the same section of the ballpark.

The data is pretty clear — the longer your time horizon, the more likely you will experience positive results.

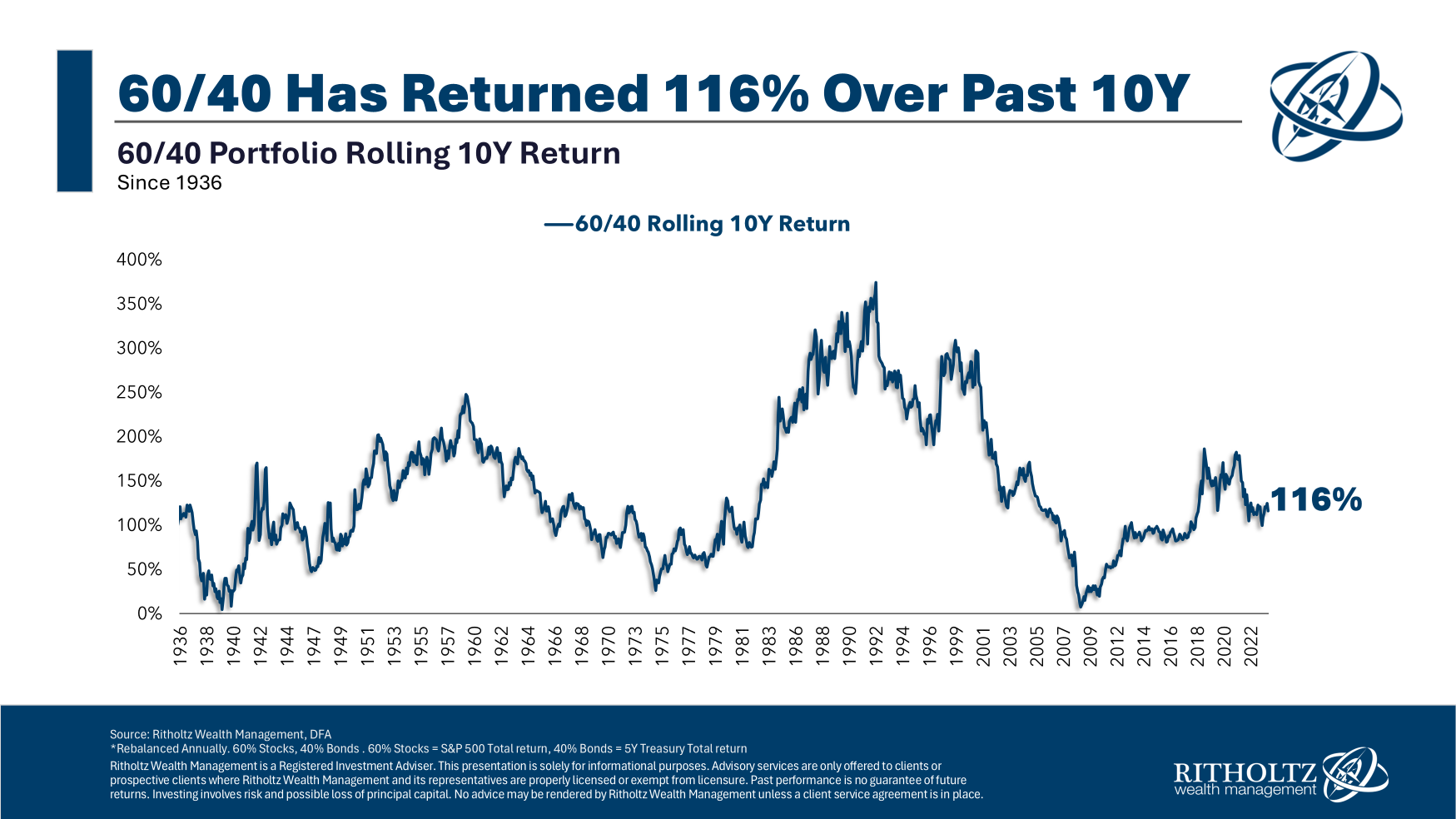

Of course, the level of returns are promised to no one and end up all over the map. These are the historical rolling 10 year total returns:

Some 10 year returns have been better than others but the results have been impressive nonetheless.

Long-term investing continues to give the vast majority of investors the best odds of success.

We dissected this question on this week’s all-new Ask the Compound:

Callie Cox, our new Chief Market Strategist at Ritholtz Wealth, joined me on the show this week to discuss questions about the potential for a recession, what the Fed should do now, going all in on the Nasdaq 100 in your retirement accounts and how markets move in off hours.

Further Reading:

What’s the Worst Long-Term Return For U.S. Stocks?

1Taxes and fees are excluded as well, of course.