In the 1970s the S&P 500 returned 5.9% per year. The problem is inflation was 7.1% per year so the real returns were negative.

This means inflation must be bad for the stock market right?

Well in the 1980s inflation averaged 5.5% per year but the stock market was up 17.3% on an annualized basis, nearly 12% higher after adjusting for higher prices.

What about low inflation?

Inflation averaged just 1.8% per year in the 2010s and stocks returned 13.4% on an annual basis.

However, inflation was 2.6% per year in the 2000s yet the S&P 500 experienced a lost decade, falling 1% per year nominally.

The stock market is a wonderful long-term hedge against inflation but sometimes it doesn’t work so well in the short-term:

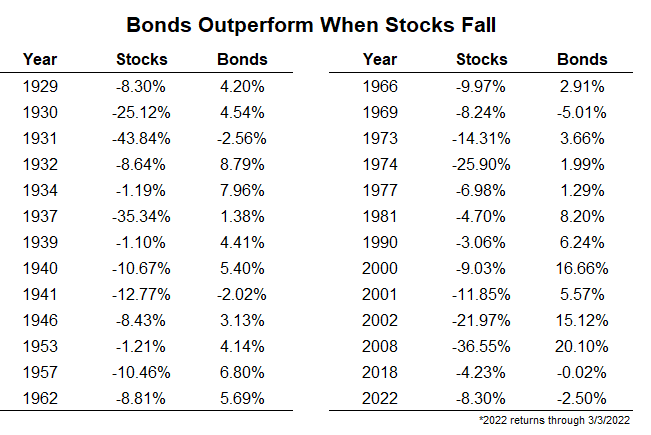

Treasury bonds1 are a great hedge against stock market declines. This is every down year for the U.S. stock market back to 1928 along with the corresponding returns for 10 year treasuries:

The average loss in a down year for the stock market is -13.3%. The average return for bonds in those same years is +5.1%, good enough for an average outperformance of almost 19%.

Unfortunately bonds are not a great hedge against high inflation over the long run.

Inflation averaged 4.3% per year from 1950-1981. The nominal annual returns for 10 year treasuries during that stretch were +2.8%. So after accounting for inflation, bond investors lost more than 37% of their investment on a real basis.

Gold was a great hedge against inflation in the 1970s, rising more than 1,300% or 31% per year. Even after accounting for 7% annual inflation, gold was up more than 23% per year.

So gold must be a wonderful inflation hedge right?

Since the start of 2020 we’ve had the highest inflation rate in four decades and gold is flat.

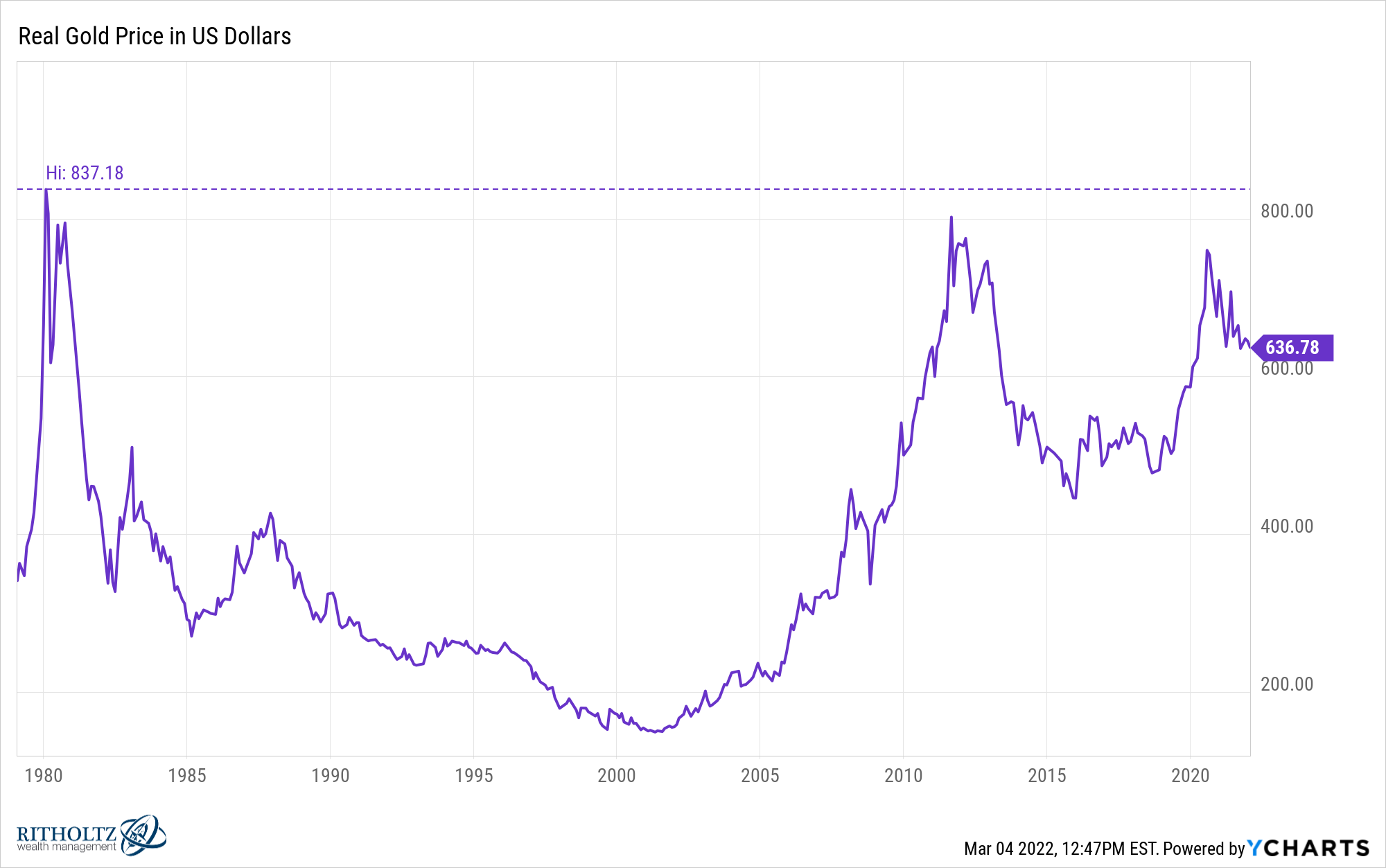

One dollar in 1980 would be worth 44 cents by 1999 because of inflation. Gold was down 43% in this two-decade period. In fact, gold is still below the 1980 highs when adjusted for inflation:

The S&P 500 is up more than 3500% even after accounting for inflation since 1980.

So gold can’t keep up with the stock market?

Actually, since the gold ETF (GLD) was launched in late-2004 it’s done a nice job more or less keeping up with the stock market. These are the annual returns since the inception of GLD:

- S&P 500 +9.9%

- GLD +8.5%

Not bad.

Some people think bitcoin is the newest of inflation hedges. It’s currently in the midst of a 40% drawdown from all-time highs despite 7.5% inflation at the latest reading.

Now you could quibble with some of the statistics here. You can win any argument you want about the markets by simply changing the start and end dates.

And markets are forward-looking after all.

The point here is there are no perfect assets. Nothing hedges you against every single risk at all times.

Investing involves uncertainty.

You can’t predict how certain investments are going to react to every situation.

Investing involves risk.

You can’t protect your portfolio from every risk.

Investing also involves trade-offs.

You can’t have it all.

There is no hedge that works for inflation, deflation, up markets, down markets, rising rates, falling rates, peace, war, recessions, expansions and everything else.

The good news is once you realize there are no perfect assets, you can begin to create a portfolio that takes into account the fact that nothing works always and forever in the markets.

Michael and I talked about hedges against inflation, geopolitical events and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

Diversification Isn’t Undefeated But It Never Gets Blown Out

Now here’s what I’ve been reading lately:

- 3 investing lessons from the Russian stock market collapse (Prag Cap)

- The 2 worlds (Prime Cuts)

- Fatherhood, cancer and what matters most (The Ringer)

- Have a plan (Irrelevant Investor)

- Will the optimists triumph yet again? (Dollars and Data)

- If you’re afraid, read this (Bull & Baird)

- War’s impact on the stock market (Big Picture)

1I’m using the S&P 500 and 10 year treasuries here.