Staying in your lane may be the closest thing there is to an investing superpower. Low commissions and access to nearly unlimited fund choices have been a boon to the individual investor but the downside to this situation is when performance causes investors to chase.

In this piece I wrote for Fortune I look at two fund examples where investors got carried away and chased performance to their detriment.

*******

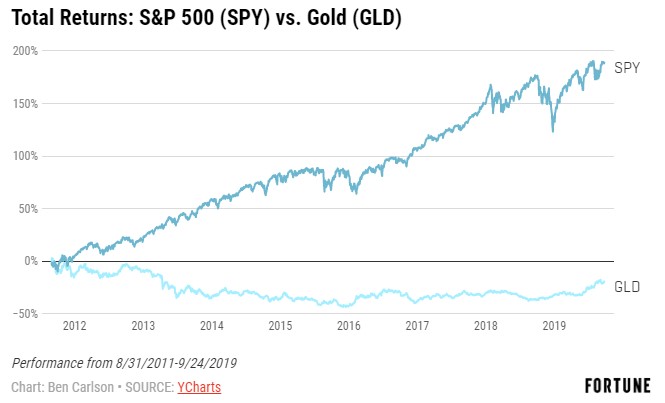

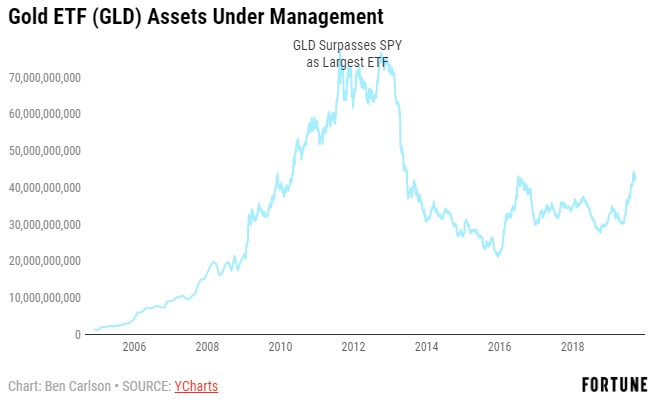

In August 2011, the SPDR Gold Shares ETF (GLD) briefly surpassed the S&P 500 SPDR ETF (SPY) as the largest exchange-traded fund in terms of assets. Since then, the investment performance of these two funds are night and day.

The S&P 500 is up roughly 190% in total since the end of August 2011 while gold remains nearly 20% below its high watermark from that summer. There’s nothing magical about becoming the biggest ETF in the world but the aftermath of this honor was none too kind to the assets in GLD:

From a high of more than $77 billion in that late-summer of 2011, assets under management (AUM) in GLD fell all the way to $21 billion by the end of 2015. What’s interesting in this scenario is how much more AUM fell than performance in the underlying fund.

Assets in GLD fell more than 72% in a little over 4 years while performance in GLD itself was only down 43%. That’s a fairly substantial crash in price but an even more substantial outflow in terms of assets.

The flipside was true in the run-up to becoming the world’s largest ETF. From 2007 through August 2011, GLD was up more than 180%. But assets in the fund grew nearly 700% in that time. Some of this could have been due to the fact that the financial crisis created a flight to hedge systemic risk, of which gold is a favored proxy for many. But it’s clear there was also an element of performance chasing going on as well.

When the fund performed well, assets poured in. And then when the fund performed poorly, assets fled. This is nothing new in the fund space. There have always been performance chasers and there will always be performance chasers.

SPY now wears the crown as the largest ETF with more than $270 billion in assets. Surprisingly, the growth in assets for SPY since GLD passed it briefly in 2011 has come from market gains, not flows from investors. Assets under management in SPY have grown just shy of 194% since August 2011, not much more than the close to 190% total returns in the fund.

Index funds and ETFs aren’t immune to performance chasing but the more non-traditional asset classes and strategies tend to see more performance chasing from investors.

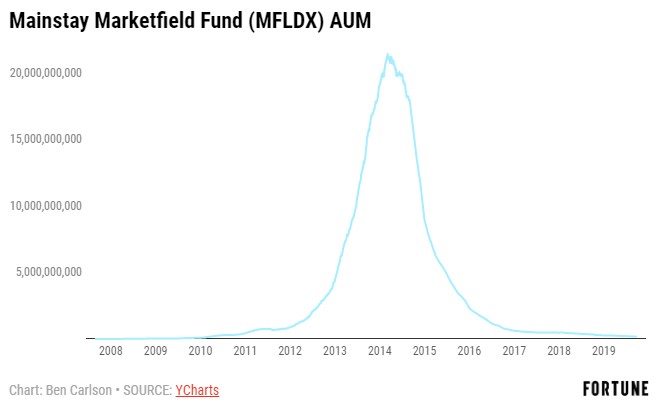

Following the market crash in 2008, investors were eager for alternative investments that would either hedge the stock market or offer an uncorrelated return stream with high expected returns. Few funds in the liquid alt space delivered on these promises but one fund did gain investor attention because of its performance.

The Mainstay Marketfield Fund (MFLDX) saw strong returns, delivering a return of more than 100% from 2009 through the first quarter of 2014. The S&P 500 was up more than 130% in this time, but the fact that an alternative fund that switches between a number of asset classes and has the ability to short securities was able to keep up attracted huge inflows from investors.

Assets in MFLDX exploded from just $34 million at the outset of 2009 to more than $21 billion by early-2014. So while fund performance merely doubled, assets were up 60,000%. Warren Buffett once said, “Size is the enemy of outperformance,” and the Marketfield Fund was no different.

Since the first quarter of 2014, MFLDX has gone nowhere, losing a total of more than 11% up to now. U.S. stocks are up nearly 80% in this time. The fast money that poured into this fund fled just as fast as it came in. Assets are now under $200 million, down 99% from the highs in 2014.

This was a performance chase of epic proportions, most likely caused by investors who were still somewhat scarred from the financial crisis and in search of an alternative to the stock market’s crazy ways. The market can be fickle but so are investors.

Performance chasing is as old as the hills so this type of behavior is never going away. There will always be certain funds or esoteric strategies that do better than others at times. Unfortunately, most investors tend to put their money into these strategies only after they’ve already experienced strong outperformance.

This piece was originally published at Fortune. Re-posted here with permission.