U.S. stocks and bonds are both having a phenomenal year so far. The Vanguard Total Stock Market ETF (VTI) is up more than 21% while the Vanguard Total Bond Market ETF (BND) has risen by almost 6%. Developed international and emerging markets are also up big (VEA and VWO both up roughly 14%) so it’s been a great year (again, so far) for the traditional asset classes. But it may seem odd at first glance to some that stocks and bonds could both be up so much this year given many investors assume these assets are negatively correlated.

Here’s a piece I wrote for Fortune that dispels this myth and provides some context around the idea of portfolio correlations.

*******

Stocks and bonds are moving higher together — for now.

The huge market gains in the first part of 2019 aren’t guaranteed to stick for the remainder of the year. But one thing is certain: It’s not out of the ordinary for stocks and bonds to rise in concert with one another.

Through the end of June, the S&P 500 was up 18.5% in 2019. The Bloomberg Barclays U.S. Aggregate Bond Index, a proxy for the broad U.S. bond market, was up 6.1% at the halfway point of the year. A simple 60/40 mix of U.S. stocks and bonds returned 13.6% through the first six months of the year, the best start for this portfolio since the first half of 1997.

In fact, going back to the inception of the Aggregate Bond Index in 1976, this was just the eleventh time a 60/40 portfolio of stocks and bonds began the first half of the year up double digits.

It may seem odd to some investors that both stocks and bonds could be up so much at the same time. Yet, since 1976, stocks and bonds have both gained in the same calendar year in 32 out of 43 years. We can take things back even further using data on 5-year treasury bonds. Since World War II, U.S. stocks and bonds have seen positive returns in 50 out of 74 years or roughly two-thirds of the time.

This relationship might not make sense to those who assume stocks and bonds should move in different directions but the whole point of diversification is to combine assets that act differently during various market environments. The problem is investors often confuse how to think about correlations within a portfolio. Most investors assume you want to own negatively correlated investments that move in opposite directions. But what you really want is assets that have a positive expected return profile with correlations that change over time depending on the market environment.

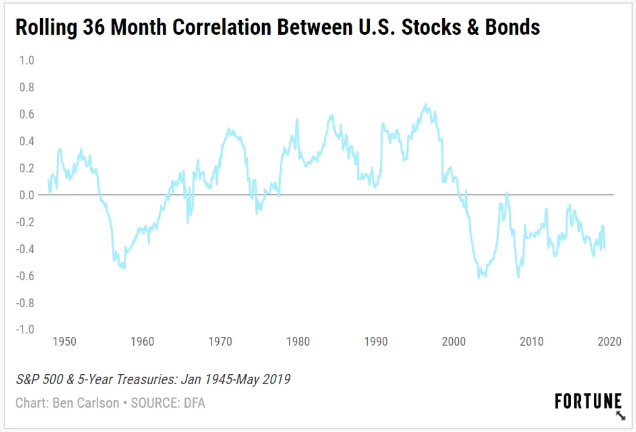

A correlation of 1.0 implies that when one asset rises so does the other asset while a correlation of -1.0 implies when one asset rises the other one falls. A correlation close to zero implies little relationship in price movements, which is exactly what things look like for stocks and bonds over the long haul. Since 1945, the S&P 500 and 5-year treasuries have a correlation of -0.1, meaning there is little relationship in how they perform. But this relationship changes over time as you can see from the rolling 3-year correlation numbers:

The relationship between stocks and bonds is anything but static, like nearly everything else in the financial markets but this is actually a good thing. The true time for bonds to shine in a portfolio is not when stocks are up but when they’re down, which is the only time you want that negative correlation to kick in.

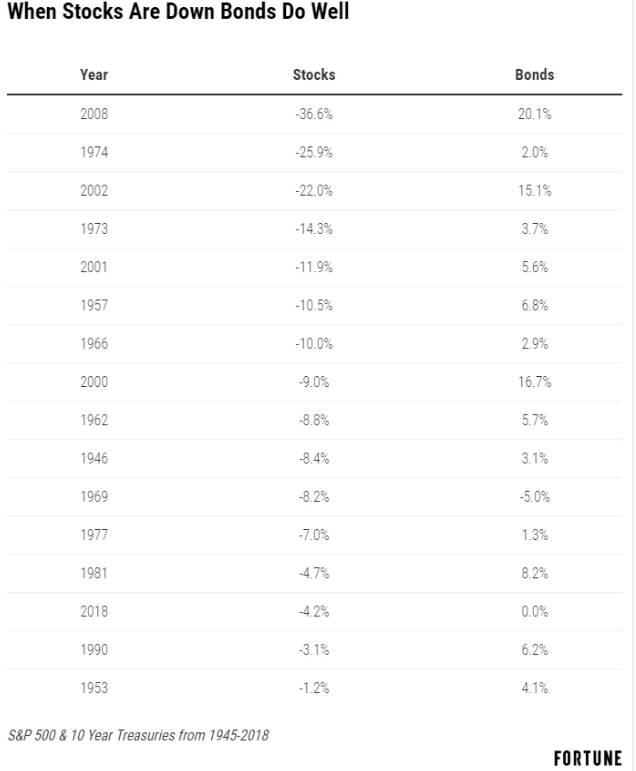

Since 1945, the S&P 500 has been down in 16 out of 74 years, with an average loss of -11.7%. In those down years, 5-year treasuries were positive 15 out of 16 times, with an average gain of 6.2%. The last time stocks and bonds were down in the same year was 1969, when the S&P fell more than 8% while 5-year treasuries were down less than 1%.

This is when bonds prove their worth in a portfolio, offering investors stability during times of volatility and the ability to rebalance into falling stocks or use bond proceeds for spending needs.

The first half of 2019 was about as good as it gets for investors in U.S. stocks and bonds. That won’t last forever. The good news is when the inevitable setback occurs in stocks, bonds tend to provide some shelter from the storm.

This piece was originally published at Fortune. Re-posted here with permission.