“Habits are the compound interest of self-improvement.” – James Clear

I hear from young people on a regular basis who complain that it’s impossible for them to save money.

The list holding them back is a long one — student loans, low wages, rent, the high cost of avocado toast, and the desire to actually enjoy their youth.

I get it.

It can be hard to find the money and saving for your future isn’t high on the list of priorities when you’re young and feel invincible.

My typical advice to this group is twofold:

(1) Start small

and

(2) Automate it.

Starting small helps for a couple of reasons. There’s a sense of loss in some ways when you start saving because delayed gratification means less fun money today. And even small amounts can really add up over time because the biggest asset you have as a young person is your human capital and the long runway ahead of you to allow compounding to do the heavy lifting.

The reason you automate is that you’ll never save what’s leftover at the end of each pay period. Pay yourself last doesn’t work very well because something will always come up and if you don’t automatically save money you’ll either (a) eventually give up or (b) forget to save in the first place.

Let’s see these ideas in action using some realistic and unrealistic assumptions.

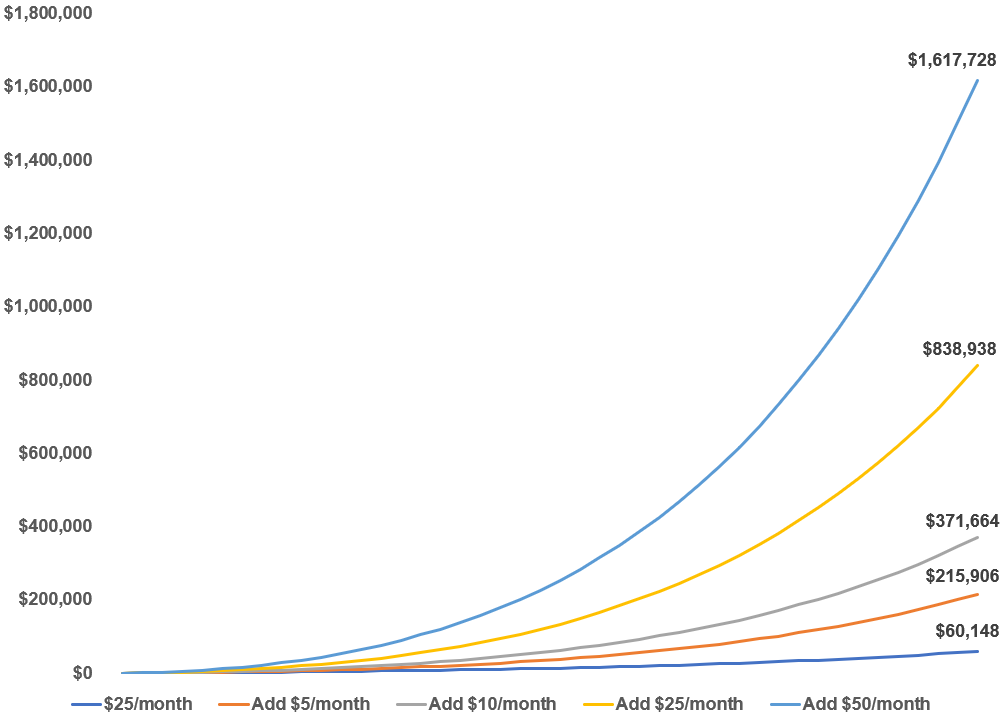

First, let’s start small by assuming a young person can start out saving $25/month. That’s basically the price of a grapefruit infused IPA at a bar in New York City or San Francisco during happy hour. If you can’t save 25 bucks a month I don’t know what to tell you. That’s our realistic assumption.

The unrealistic assumption is that you earn 6%/year on that money starting from age 22 until retirement at age 65. No one earns consistent returns like that but making this assumption helps show the power of compounding.

If you were to continue saving $25/month from age 22 to age 65 you would end up with a little more than $60k. Not exactly enough money to retire on.

But what if instead of saving a measly $25/month for the entire period, instead you slowly but surely increased the amount you save every year. What if you saved just $5 more per month every year? Or even $10 or $25 or $50 more per month every single year to work your way into a higher savings rate?

Now things look much better:

Adding $5, $10, $25, and $50/month to your savings each year is an annual increase of just $60, $120, $300, and $600, respectively. These aren’t enormous sums of money but look at the massive differences in the ending balances.

Saving $25/month over the course of a year is only $300 in total but adding $50/month to that total every year using an incremental approach can add up to a fairly large sum of money through a combination of diligent saving and compound interest.

Every little bit helps when you’re young and have decades and decades ahead of you. Building wealth from a young age doesn’t require a ton of money as long as you remain disciplined and work your way up to a healthy savings rate.

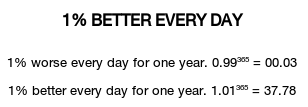

James Clear talks about the big difference small changes in our habits can make in his excellent book Atomic Habits. Clear makes the point that massive success does not require massive action, but minor improvements that can compound on top of one another:

The difference a tiny improvement can make over time is astounding. Here’s how the math works out: if you can get 1 percent better each day for one year, you’ll end up thirty-seven times better by the time you’re done. Conversely, if you get 1 percent worse each day for one year, you’ll decline nearly down to zero. What starts as a small win or a minor setback accumulates into something much more.

This is one of my favorite new examples to explain how compounding works, both for you and against you. Here’s the math Clear uses to visualize this relationship:

Most people don’t even realize their poor habits aren’t just causing them to miss out on the improvements that can be seen by implementing good habits, but their bad habits are effectively compounding against them in the wrong direction.

Even small amounts of money can help because small wins can help you develop the correct savings habits over time. One way to reduce the strain on your brain is to start small but also automate good behavior ahead of time so you don’t even have to think about it.

Automation is the key to creating good money habits you can actually stick with.

Source:

Atomic Habits: An Easy & Proven to Build Good Habits & Break Bad Ones

Further Reading:

Just Half a Percent