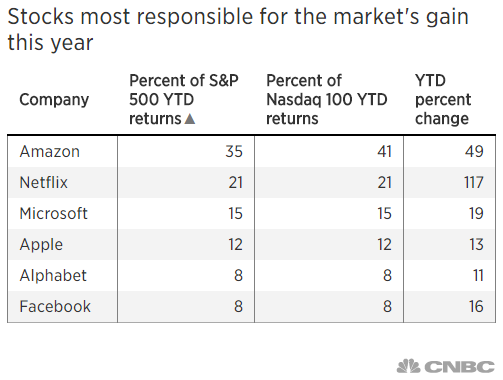

CNBC had a piece this week that looked at how top heavy returns in the stock market have been this year. They showed 3 stocks — Amazon, Netflix and Microsoft — alone make up more than 70% of the gains in the S&P 500 and Nasdaq 100 indexes:

When you include Apple, Google (I refuse to call this company Alphabet), and Facebook those numbers jump to an absurdly high 98% and 105%, respectively.

The obvious takeaway here would seem to be that 2018 market returns (around 5% for the S&P and 14% for the Nasdaq 100) are all being driven by a handful of names. And if that handful of stocks ever come back down to earth, which they’ve been wont to do on occasion, watch out below.

The simplest explanation for these staggering numbers is the fact that this is how market capitalization weighted indexes work. By definition, the largest stocks will have a bigger impact on the returns than the smaller stocks.

For instance, Amazon has added nearly $285 billion in market cap this year alone. This number is insane when you consider Amazon’s entire market cap was $285 billion in April of 2016. That $285 billion gain this year is the same size as the total combined market cap of the 40 smallest stocks in the S&P 500.

Many of the names in that list of the 40 smallest stocks by market cap have had good returns this year:

- TripAdvisor +70%

- Robert Half International +21%

- Envision Healthcare +29%

- AES Corp +23%

- Nordstrom +14%

But those stocks aren’t going to move the needle as much as Amazon or Microsoft or Apple because they don’t carry the same weights as the large tech stocks.

It would also be more concerning that the gains were so concentrated at the top if the S&P 500 was the only thing going up this year. Spoiler alert — it’s not.

Small cap stocks are up around 10% in 2018. Mid caps have risen almost 6%. Micro caps, the smallest stocks in the market, making up a measly 2% of the total, are up more than 13% this year.

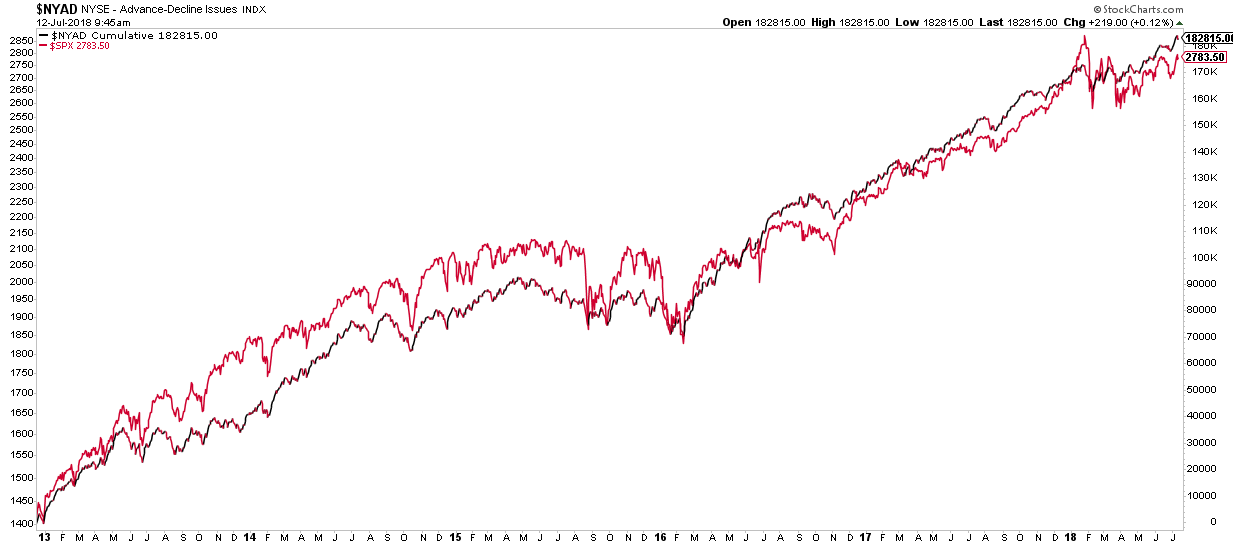

Another way of looking at this is the advance-decline line, which is a way to track market breadth by comparing the number of stocks rising with the number of stocks falling. Here’s the latest reading set against the S&P 500:

If there were only a few stocks rising you would see a large divergence between these lines. Instead, we see the advance-decline fairly inline with the stock market. This tells us that there are far more stocks rising than just a few of the biggest names.

It may feel odd to see performance being driven by so few stocks but this is how the stock market generally works over time. The majority of returns come from a handful of names. It’s like this over both short and long time frames.

Data from Hendrik Bessembinder showed that from 1926 to 2015:

- Less than half of all monthly stock returns in the U.S. are larger than the one-month Treasury bill rates (meaning most stocks don’t outperform cash).

- Just 42.1% of stocks have a lifetime return greater than T-bill returns while half deliver negative lifetime returns.

- Over half the wealth created in the stock market came from the 86 top-performing stocks, around 0.33% of the total.

This doesn’t mean other stocks didn’t do well over this period, just that the most wealth was created in the stocks that grew to be the biggest (which seems sort of obvious when you think about it).

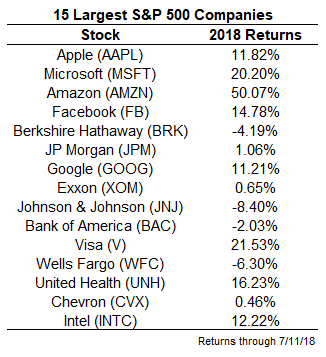

It can also be instructive to look at how some of the other biggest names are performing this year:

Yes, tech stocks are the big winners. No, this won’t last forever. But it’s also true that financial or energy stocks at the top of the market won’t be laggards forever either. It’s quite possible that they can offset some of the relative losses when we do finally see a mean reversion in technology.

Here are a few takeaways to wrap things up on this topic:

- If you’re invested solely in a total market or S&P 500 index fund, then yes, your returns will likely be driven by a handful of stocks. This is simply the way market cap weighting works, for better or worse.

- If you’re diversified outside of the market cap weighted indexes, that means your returns are going to look different at times. Going lower on the cap-weighted spectrum has been a net positive this year. Last year large caps outperformed micro, small and mid caps. So it goes when diversifying.

- The concentration of returns in the stock market is one of the most underrated reasons for diversifying your investments. No one knows where the huge gainers will come from each year or over the long run. Diversifying gives you a chance to allow the outlier winners to overshadow the outlier losers.

- None of this data I’ve presented here means the stock market can’t fall from here. We certainly could see what many would call an overdue correction in tech stocks that brings down the rest of the market with it. Or investors could get spooked by something else which could send micro caps, small caps, mid caps and mega caps all reeling.

- But the stock market is not currently being driven by just a handful of stocks. In fact, the fact that smaller companies are outperforming this year is a tell-tale sign that this isn’t the case. Whether it lasts or not, this is a full-fledged market rally where every capitalization size is taking part in the gains.

Further Reading:

The Biggest Stocks

Now here’s what I’ve been reading lately:

- What burden is that other person carrying? (NY Times)

- A letter to grandparents (Retirement Field Guide)

- The 9 essential conditions to commit massive fraud (Reformed Broker)

- “Simple is better than complex and processes are better than pundits.” (Irrelevant Investors)

- The next 7 years (Pension Partners)

- The rise and fall and rise of Benjamin Graham (Novel Investor)

- Is Jerry Seinfeld the reasons the Amex Black card exists? (Points Guy)