A few weeks ago I took the other side of the phenomenal growth in index funds by playing devil’s advocate on some of the problems with this growth. A few people asked me to expand on one issue in particular:

“Index” can be a subjective term. Most of the money is going into traditional index funds that track something like the S&P 500 or a total market fund but there is plenty of money going into products that are index in name only. The number of choices now available in ETFs and index or index-like products can be overwhelming and many are meant to be sold, not bought. Our brains don’t function very well when faced with an ever-increasing number of choices. The temptation to make a change to your portfolio has never been greater.

One of the reasons many funds can be considered an index in name only is because they have a hard time tracking the actual index. Sumit Roy wrote a piece for ETF.com last week that aligns nicely with this idea. He wrote about the VanEck Junior Gold Miners ETF (GDXJ), which tracks the MVIS Global Junior Gold Miners Index.

This fund currently has more than $5 billion in assets, more than $3 billion of which has come since the beginning of 2016. The size of the fund is becoming a problem. Roy explains:

The ETF has gotten so big that it now owns giant stakes in its underlying holdings, three-quarters of which are Canadian companies. According to an analysis by Scotiabank, there are 10 Canadian companies that the ETF owns where its ownership percentage is more than 18%.

For six of those companies, the percentage would be even greater, but presumably, the fund doesn’t want to exceed the 20% level, which, under Canadian rules, would force the ETF “to automatically extend a takeover offer to all remaining shareholders at the same terms,” according to a Scotiabank report.

The ETF has also struggled to abide by U.S. IRS diversification requirements. “GDXJ has intermittently been in jeopardy of losing its preferential tax treatment (as a regulated investment company) since last September because its portfolio often doesn’t comply with the diversification requirements of the U.S. Internal Revenue Code,” noted Scotiabank.

The fund it getting so large that it’s having to go outside of its stated mandate to meet demand and avoid becoming too large of an owner in certain stocks:

In an attempt to try to ameliorate the concentration issues it’s facing, the ETF now has five holdings that aren’t index constituents, representing 25% of GDXJ’s portfolio, according to BMO Capital Markets. One of those holdings is the VanEck Vectors Gold Miners ETF (GDX), another product from the same issuer, which focuses on much larger gold companies.

I pulled up the portfolio holdings for this fund and sure enough, the second largest holding is GDX, coming in at around 5% of the total assets. So the second largest holding of this ETF is…another ETF.

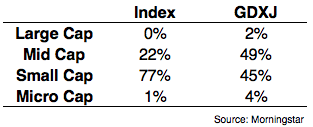

Adding these new names to the fund has also changed the complexion of the portfolio in terms of market cap. Here’s the comparison of GDXJ against the index it’s supposedly tracking:

Junior gold miners are supposed to be small cap stocks but this product has been transformed by the changes the fund provider has made into more of a mid cap fund. This may not be a huge deal just yet but eventually, there is bound to be tracking error from the underlying index that most investors are likely unaware of.

This example brings up a whole host of questions and potential problems down the line as ETFs continue to gain market share. Here are a few questions that come to mind on the subject:

- Are regulators going to have to eventually change the rules to allow for larger ownership stakes in companies for ETF and index providers?

- How should ETF providers act when they become so large that they can’t fully replicate the index or strategy in their mandate?

- Should some ETFs stop creating new units and close to new investors?

- How many obscure stocks are going to see liquidity or trading issues based on ETF ownership?

- How much of an impact will fund flows end up having on the winners and losers in the ETF space?

- How many ETF or index fund investors actually know what they’re getting themselves into when they buy these funds?

- How many ETF experts and ETF fund-of-funds are going to spring up in the years ahead?

- How long until ETF picking becomes the new form of stock picking as a hobby for novice investors?

- How much of the cost and tax benefits of the ETF structure will be squandered in pursuit of the next best thing in the ETF space?

Investors in ETFs need to understand their fund’s exposure, cost, liquidity, risk, and regulatory structure before investing. It’s not good enough to simply trust the word “index” in a fund name anymore. The low-cost fund revolution is an amazing development for investors but you can’t buy something just because it’s an ETF or index fund. You still have to do your homework and know what you own and why.

Source:

How an ETF Gets Too Big For Its Index (ETF.com)

Further Reading:

Playing Devil’s Advocate in Index Funds

How to Pick the Right ETF