The S&P 500 has outperformed the MSCI World Index each of the past three years and six out of the last eight. This is quite a run when you consider how often U.S. stocks have outperformed the rest of the world’s markets over historically.

Since 1970, on a calendar year basis the S&P 500 has outperformed 23 out of 46 years or 50% of the time. On a rolling three and five year basis it was also a dead heat at 50% for each. At the seven year interval the U.S. has outperformed 48% of the time. It looks like a coin flip to see which markets outperform over both shorter and longer time frames. The returns are also fairly similar with annual gains of 10.3% and 9.5%, respectively, for U.S. and foreign shares.

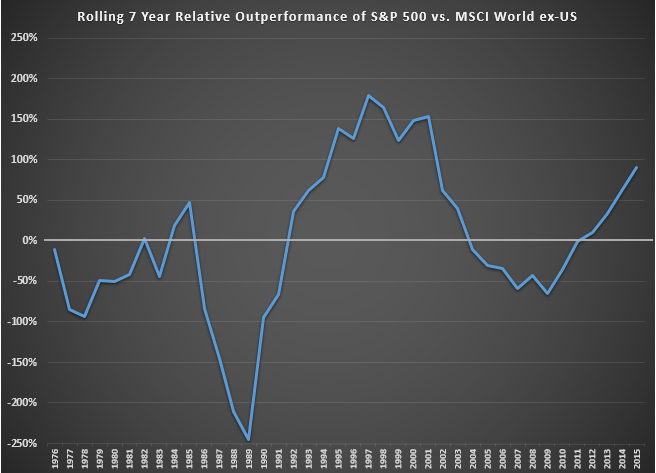

Yet the total returns have seen some huge divergences in that period. This graph show the relative outperformance of the S&P 500 versus the MSCI World ex-U.S. over rolling seven year periods since 1970:

Since 2009 the U.S. has clearly been the big winner, outperforming by nearly 100% in total. One would assume this trend would show some mean reversion eventually but these markets have seen even wider dispersion in the past from a relative performance perspective.

In the 1970s and 1980s the dominance of Japanese stocks saw world markets outperform U.S. stocks by almost 250% in the seven year period ending in 1989. From there the U.S. dominated in the 1990s and ended up outperforming foreign stocks by almost 200% by the tail end of that decade (hello mean reversion).

The question then becomes — if the returns are similar over the long-term, what’s the point of diversification between the various markets? The reason many investors ask this question repeatedly is because diversification within risk assets rarely, if ever, earns its place in a portfolio over the short-term.

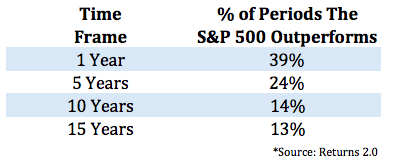

I did a similar comparison between the S&P 500 and the DFA Equity Balanced Index, which is a globally diversified index consisting of large caps, small caps, REITs, foreign stocks, emerging markets and value stocks (see below for the index weights). The following table shows the number of times the S&P 500 outperformed the more diversified equity index using rolling annual calendar year returns since 1970:

S&P 500 outperformance has dropped each time you go further out in your time horizon. I will say that one of the reasons for this outperformance is that DFA tilts towards small caps and value stocks, which have performed very well in that time. Even if the small and value premiums are lower in the future there are still many reasons to stay diversified as an investor.

Here are three reasons I think it makes sense to broadly diversify, both globally and within an asset class:

- No one really knows how the future is going to turn out. The U.S. has been the clear winner over the last century or so in terms of becoming an economic and stock market powerhouse. It’s hard to see that changing anytime soon but who knows how these things will play out in the future from a relative perspective. Diversification is an admission of a lack of foresight about an uncertain future.

- Diversification is never going to protect you from horrible days, months, quarters or years. It really earns its stripes over longer periods of time (which are the only ones that should really matter to investors). The only way it works is if you have the patience to follow through with it. Like all reasonable investment strategies, it’s never going to feel great all the time.

- Successful investing really boils down to regret minimization. Think about being a U.S.-only investor and missing out on those huge relative gains in foreign stocks the 70s and 80s. Or think about being a foreign investor and missing out on the huge relative gains in U.S. stocks in the 90s and more recently. Most investors will be better off thinking globally, not because it promises higher returns, but because is reduces concentration risk. Diversification is still one of the best forms of regret minimization and risk management an investor has..

Further Reading:

Is International Diversification Worth the Risk?

*DFA Equity Balanced Index = 20% S&P 500 Index, 20% US Large Value Index, 10% US Small Cap Index, 10% US Small Value Index, 10% DJ Wilshire REIT Index, 10% Int’l Value Index, 5% Int’l Small Cap Index, 5% Int’l Small Value Index, 3% Emerging Markets Index, 3% Emerging Markets Value Index, 4% Emerging Markets Small Cap Index; rebalanced monthly. Reminder, this is not a recommendation — do your own homework before choosing an asset allocation that’s right for you.

Great article, at just the right time, as I was beginning to question my own decision to invest in a global tracker, as opposed to the Buffett recommendation of the S&P 500. Thanks for the reassurance.

I think it might narrow in the future if the US continues to embrace the ideas of the international developed markets. With a government taking more taxes, increasing regulation, and having more control, there may be less growth in the US market. We truly need to make sure we have entrepreneurs settle in the USA to do their work and develop new tech that brings good jobs and new goods to market. Surrendering that leadership to China would be bad for the States.

Sure, but technology now makes it easier to innovate from anywhere. People will still want to come to the states but having smart people innovate around the globe is a great thing for everyone.

Brian — fully agree. Technology is not a limiting factor. There may be more political risk in some countries where property rights aren’t nearly as strong. I think that the USA stays strong there. I think the tax & regulatory risk questions may be on the minds of some entrepreneurs. Even a few years ago we saw entrepreneurs moving from France to the UK just to enjoy improvements in labor laws and taxes.

If the US moves more toward a European model, do all the entrepreneurs move to Singapore? If yes, what’s the net loss to the USA? The net gain to Singapore? (* been there, great country, great people, highly recommend although very boring weather! *)

Insightful piece, as usual. One has to look at which markets are dominating during any particular period by putting the major country ETFs on a relative chart. The US market has dominated recently.

When we say “stocks for the long term” we don’t mean all stocks in the world – there are many countries with terrible records, including confiscation. It depends on the culture and the economics of the country concerned and historically the English-speaking countries (US, UK, Canada, Australia, NZ) have been the markets most hospitable to investors’ money as far as stocks are concerned.

True, Dimson and Marsh have done some great work on this if you haven’t seen it:

http://www.investering.dk/documents/10655/157815/Credit+Suisse/0c0ceeb5-c5af-464d-be00-fb1378cb0412