“Believe there are bubbles, but don’t go around looking for them and betting the ranch on them.” – Cliff Asness

Jeremy Grantham is a legend among investing circles. His quarterly letters are on my must-read list. I’ve seen him speak before and he has the uncanny ability to make complex investing topics easy to understand, which I think is one of the signs of a truly great investor.

Grantham’s investment firm, GMO, is considered an expert on asset price bubbles. They have studied market bubbles going back hundreds of years. Grantham is credited with calling the Internet bubble in the late-1990s and the real estate/global debt bubble in the most recent financial crash.

In his most recent piece, Grantham lays out his current thinking with a guess on a possible end to the bubble he sees in stocks:

But after October 1, the market is likely to be strong, especially through April and by then or in the following 18 months up to the next election (or, horrible possibility, even longer) will have rallied past 2,250, perhaps by a decent margin.

And then around the election or soon after, the market bubble will burst, as bubbles always do, and will revert to its trend value, around half of its peak or worse, depending on what new ammunition the Fed can dig up.

These types of calls garner plenty of media attention because everyone would like to be able to weave in and out of the markets to avoid painful losses.

But does spotting bubbles improve GMO’s investment performance?

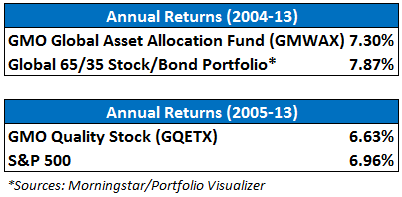

The only problem with this strategy is that there’s being early and being way early. Take a look at the past decade (GQETX only started in ’05) of returns for GMO’s Global Asset Allocation and Quality Fund results versus the benchmark returns:

I was actually surprised when I ran these numbers. I would have thought the GMO funds would have crushed the markets during the crash and lived off of that relative outperformance for years to come.

Based on the annual return numbers I looked at, even though the funds did protect on the downside in 2008, they were far too defensive in the two years leading up to the crash and stayed defensive during the snap-back rally that led to the new bull market.

The asset allocation fund currently carries a little less than 20% of fund assets in cash. This could turn out to be a prudent move if the markets crash and they are able to deploy at much lower prices. But if markets go higher the needle will continue to move as far as relative underperformance goes.

Of course, GMO is much more than just Grantham’s bubble calls. As Tom Brakke recently pointed out, focusing exclusively on timing and market levels misses the real point about risk management and market perspective. There could be many other reasons for the underperformance of these funds. And GMO’s risk-adjusted returns are better than the overall market because they didn’t fall nearly as much in 2008.

But this just goes to show you how hard it can be to try to run your portfolio based on the predictions of booms and busts. The leading experts in asset price bubbles have been unable to completely take advantage of them even though they saw them building in real-time before just about everyone else. Timing these moves requires not only getting the direction of the call right but also pinpointing the reversal of the move.

That’s because human nature is impossible to quantify. No one knows when or why investors will decide something is overpriced today versus last week or last month at a similar price and valuation. This is why risk management is so important.

Most investors investors need to use probabilities in combination with portfolio risk controls (asset allocation, diversification, rebalancing, etc.) when dealing with uncertain outcomes.

Would life be easy if we were all able to completely sidestep market meltdowns? Yes, of course. But even if you aren’t able to do this (and trust me, you can’t) you can still earn solid returns in the markets if you behave and don’t let the periodic downturns scare you.

Obviously, a diversify, buy, hold and rebalance strategy is not without its own psychological pitfalls. It’s not easy to stick to a long-term plan. I just think that for 95% of the investors it’s the simpler option because it requires a much lower number of decisions.

Unless you have a systematic process that tells you exactly when to move in and out of the market, it’s a constant game of second-guessing and anxiety. Even then, it’s a very difficult strategy to pull off for even the best investors.

*******

*For the Global 65/35 Stock/Bond portfolio I used index funds that tracked closely to the Morningstar benchmark for a global asset allocation fund: 30% Total U.S. Stocks, 25% International Stocks, 10% Emerging Market Stocks, 15% U.S. Bonds and 20% Global Bonds.

[…] Spotting Bubbles […]

As someone who invests money for individual investors I can tell you that if a fund drops by 45% in one year, most investors will bail out. The research backs this up. Just look at the average investor’s return in mutual funds vs. the actual returns. The Grantham Absolute Return fund was down less than 15% in 2008. The individual investor can live with that type of decline. Logic dictates to invest in an index fund and stay invested. Reality proves that “mom and pop” will bail out and fire their advisor if there investments drop like many funds did in 2008 – 2009. Grantham can be an important part of a diversified portfolio.

Very valid points. I agree. I like to say that investing is about regret minimization. You either miss out on some of the gains or some of the losses but not both. There’s not a perfect way to hit the upside and miss the downside. Unfortunately, most average investors don’t want to miss out on the gains but they can’t handle the losses. Pick your poison.

[…] Just how well has GMO done “sidestepping” bubbles. (A Wealth of Common Sense) […]

[…] Just how well has GMO done “sidestepping” bubbles. (A Wealth of Common Sense) […]

I find the coverage (not yours, which is very good, but most of the rest) on Jeremy Grantham’s thoughts as very strange, since most of it has painted him as being bearish. In actual fact, he is bullish, since he states that the market will rise another roughly 20% over the next year or two. I will take that with my SPY holdings anytime! Further, articles are selectively quoting “I am sure it will end badly” when he is actually saying that when the current bull market ends, this will end badly. Yes, and just as surely as nasty bear markets follow bull markets, the sun will set after it has risen, and it will get dark. Talk about truisms. And yet the press reports this as something that is very insightful.

His actual bullish conclusions are:

“The bull market may come to an end any time, indeed as I write it may already have happened. It could be derailed by disappointing global growth, profits sagging as deficits are cut, a Russian miscalculation, or, perhaps most dangerous and likely, an extreme Chinese slowdown.

But I believe it probably (i.e., over 50%) will not end for at least a year or two and probably not before it reaches a level in excess of 2,250 on the S&P 500. Prudent long-term value investors will of course treat all of the above as attempted entertainment (although I believe all statistically accurate) and be prepared once again to prove their discipline and man-hoods (people-hoods) by taking it on the chin.

I am not saying that this time is different (attention Edward Chancellor). I am sure it will end badly. But given this regime of the Federal Reserve and given the levels of excess at other market peaks, I think it would be different to end this bull market just yet.”

True and people forget that Grantham pretty much called the bottom in ’09. Problem is that not all of grantham’s mkt calls are exactly how GMO runs the money in there funds. He even admits this himself. That’s what many don’t understand. Impossible to time these event which is what some people are looking for when reading his quarterly reviews.

Ben, thanks for all of your work on this blog – it has become one of my new regular reads.

Just curious why you chose the GMO Global World Allocation fund. Might the GMO Benchmark Free Allocation fund (GBMFX) be a better representation of their “best ideas?” 10 year return for GBMFX according to Morningstar is +9.77% vs +7.7% for the S&P 500. 200bps of outperformance certainly isn’t what I would call “crushing the market” but most people would be happy with it. As one reader alluded to, I think the value they add is their ability to navigate down markets and keep clients invested during difficult times. In 2008, GBMFX returned -11.23% compared to the S&P 500 drop of -37%. While nobody likes losing money, I think it is safe to say GMO’s clients were quite satisfied with their performance during this time period.

Valid point. I could have looked at both funds and it’s very difficult to benchmark asset allocation funds with any precision. It really comes down to investor preference and what they hope to get out if the fund…if it’s tactical or all-in-one or whatever.

“And GMO’s risk-adjusted returns are better than the overall market because they didn’t fall nearly as much in 2008.”

It comes down to what’s important to the investor. If you can’t stomach the wild swings — because you’re uncertain when you’ll need liquidity, or just because it makes you anxious — then drawdown minimization matters. If you’re a long-term investor who doesn’t mind the the whipsaw of equity markets, then by all means move towards more aggressive equity exposure.

True. Can’t have it both ways. The problem is many long term investors try to be market timers sometimes and buy and hold investors at other times. The temptation is strong in both directions.

[…] Spotting bubbles is just half the problem – A Wealth of Common Sense […]

What do the annualized volatilities on those funds look like relative to s&p500 or the appropriate benchmarks. Obviously with lower volatility and smaller drawdowns, and market matching returns these Gmo funds would be appealing.

I don’t have the exact stats on me right now (I’m traveling) but I did run these numbers and GMO did have better risk-adjusted returns. The problem is, most individual investors don’t understand the concept of risk-adjusted returns and at the end of the day volatility is meaningless with a long enough time horizon (unless you let it affect you int he short-term). I guess it all comes down to choosing whether you want to miss out on gains or miss out on losses.