The Thrift Savings Plan (TSP) is the defined contribution retirement plan for U.S. Federal government employees. The TSP has nearly 5 million participants and over $500 billion in assets under management.

I’m on record saying I think the TSP should be offered to all U.S. workers in addition to their current plan (or those that aren’t offered one) because of its low costs and the simplicity in its design. Maybe it’s not the perfect plan and it doesn’t have all of the fund options certain investors would like, but it’s far better than the majority of the alternatives out there.

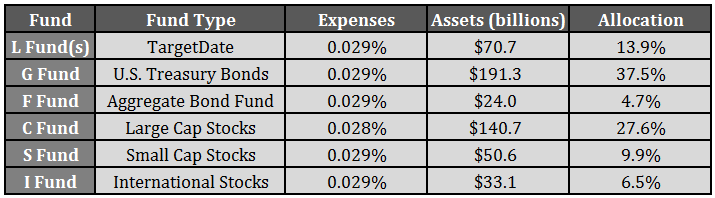

Each year the government posts a reports detailing each fund’s performance and other useful stats on the overall plan. Here are the relevant numbers for year-end 2014:

Here are a few of my takeaways from these numbers:

The fees are incredibly low. Each fund charges less than 3 basis points, which shows you the power of economies of scale on large retirement plans. For comparison purposes, the lowest cost fund I could find offered by Vanguard is the S&P 500 ETF, which charges 5 basis points (0.05%).

I love the fund names. One of the problems average investors have is that they often get confused by the sheer number of fund choices available in most retirement plans. Not to mention, most mutual fund names make no sense or just try to confuse investors. The TSP simply named their funds with a single letter and there are only six fund choices available. While there are certain fund categories that are lacking for more seasoned investors, I think a lack of choices is a net positive for 90% of individual investors to cut down on decision fatigue and switching costs between different funds.

The overall asset allocation is basically 60/40. Just over 40% of the funds are allocated to bonds while just under 60% are in stocks (assuming most of the targetdate funds are allocated to stocks).

There’s a huge home country bias in stocks. Only 6.5% of total assets are in the international stock fund. As for the stock market allocation, international stocks make up about 15% of the total even though U.S. stocks account for just over 50% of the global stock market cap. The home country bias is alive and well as most investors prefer to invest in their home country’s stock market.

Government employees are conservative investors. When setting your asset allocation you have to take into account all of your financial assets. Federal employees each receive a healthy pension at retirement. It’s a massive perk of being a government employee. A pension provides fixed income in retirement, which makes it very bond-like in nature. Yet by far the largest allocation by plan participants is the treasury bond fund. It’s impossible to know every investor’s situation and assets outside of the plan, but from this information alone, I’d venture to guess that these investors are being far too conservative with their investments.

The TSP holds a massive amount of treasury bonds. Scott Burns drew my attention to an impressive stat last week when he made the comment on Twitter that the G Fund assets would rank 7th when compared to foreign holders of U.S. Treasuries. That would rank the G Fund just behind Brazil ($245 billion) but just ahead of both the United Kingdom ($184 billion) and Switzerland ($178 billion) in terms of treasury bond holdings.

It is also interesting how little, less than 5%, goes into the F fund (stands for Fixed Income).

As a retired government worker I think very highly of the TSP although I will note neither the government or my old union (APWU) ever gave out much investment advice. Some of my former coworkers were C fund heavy, one was 75% G fund and still one more went the Beanie Baby craze of the late 1990s.

Good point. The F Fund is much more diversified. You’re not the first person to tell me that the TSP doesn’t offer very good educational opportunities. That’s a shame, especially with such a large investor base. That’s the next step to making this a much better plan,

Interesting information, Ben. I am surprised by the degree of home country bias in the stock allocation. Also, re: the G Fund, it’s my understanding this fund exclusively holds a special class of floating-rate Treasury bonds, so interest-rate risk is minimal or nonexistent. That’s a huge plus relative to “regular” indexed or managed bond funds. In my practice I see the TSP accounts of retirees or near-retirees, so the average age of participants may be quite high, in which case the overall allocation is perhaps not too conservative,

Interesting. Here’s what I found on the G Fund:

• The G Fund offers the opportunity to earn rates of interest similar to

those of U.S. Government notes and bonds but without any risk of loss

of principal and very little volatility of earnings.

• The objective of the G Fund is to maintain a higher return than inflation

without exposing the fund to risk of default or changes in market prices.

• The G Fund is invested in short-term U.S. Treasury securities specially

issued to the TSP. Payment of principal and interest is guaranteed by the

U.S. Government. Thus, there is no “credit risk.”

• The interest rate resets monthly and is based on the weighted average

yield of all outstanding Treasury notes and bonds with 4 or more years

to maturity.

• Earnings consist entirely of interest income on the securities.

• Interest on G Fund securities has, over time, outpaced inflation and

90-day T-bills.

Sounds to me like it’s something of a longer duration version of some of the fixed return funds you see in most 401k plans. Looks like the yield is basically t-bills+1-3%.

Great work, Ben. I’d heard of the TSP, but knew nothing about it.

Would that Social Security offered to the gen pop the enlightened choices available to federal employees. Or even one choice, a 60/40 balanced fund.

But at the sleepy SocSec HQ in Baltimore, a yellowed Norman Rockwell calendar from 1935 remains on the wall, and the whistles of steam locomotives still echo over the city.

‘National Tabulating Machine’ and ‘Nash Kelvinator,’ whisper the touts at the wirehouse office. But everyone knows stocks are for speculators.

I agree. Would be nice to have the choice.

Also, check out the info sheet on the G Fund:

https://www.tsp.gov/PDF/formspubs/GFund.pdf

Thought you might find that interesting that they issue their own t-bonds to this fund specifically. Putting “without any risk of loss of principal” is probably a big reason why so many are invested in the fund.

[…] A closer look at the government’s Thrift Savings Plan. (awealthofcommonsense) […]