“If you have trouble imagining a 20% loss in the stock market, you shouldn’t be in stocks.” – John Bogle

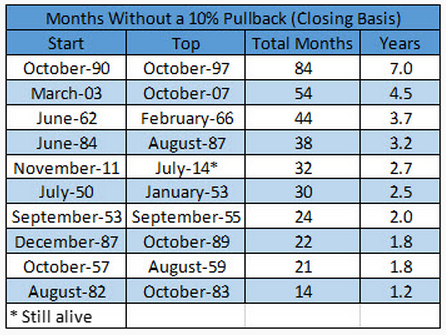

Ryan Detrick shared an interesting chart on his blog this week:

He showed that going back to 1950 there have only been four bull market streaks that lasted longer than the current one without the S&P 500 experiencing a 10% correction. Many are saying we are overdue for a correction but the market doesn’t always cooperate with cliches. These things can last much longer than most people realize.

Some investors are sure we’re heading for a crash because we’ve had such an uninterrupted rise in stocks. While a crash is never out of the realm of possibilities, just because stocks are up doesn’t mean they have to immediately crash.

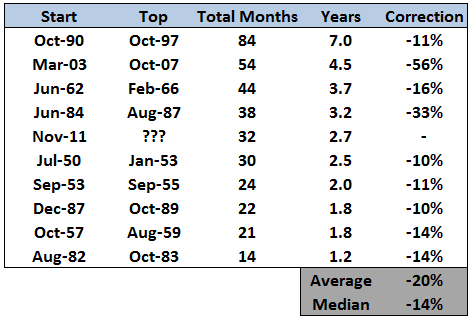

I shared Ryan’s chart on Twitter and was asked how large the subsequent losses were once the market did finally pullback following these rallies. Here’s what I found:

There were a couple of crashes after these lengthy rallies, but the majority of these were run-of-the-mill corrections that you should plan on experiencing every few years in the stock market.

It can be difficult to remember this fact after it seems like the market only goes up in the midst of a strong bull market. Periodic losses help weed out the real long-term investors from the bull market groupies. It’s an unfortunate byproduct of the zero sum nature of investing.

Plenty of pundits have been calling for a pullback for a while now. Eventually they will be right. It’s the timing that gets you on these type of calls.

Wow, seven years! And followed by only an 11 percent correction? That’s insane!

Honestly I’m not sure what to tell clients when they ask about whether we’re “due” for a correction. Obviously, as you’ve pointed out, these things can last a long time without the market behaving “rationally”.

So my answer is always, I don’t know, and that you should just stay focused on a long term strategy.

[…] at A Wealth of Common Sense gathers data on stock market corrections after long winning streaks. Double digit losses are common following a strong bull market, but the timing is difficult to […]

[…] How bad will the correction be when it finally occurs? And should people be spending every f*cking waking second of their day preoccupied with this question? (AWealthOfCommonSense) […]

They are in the sense that for every buyer there is a seller and there will be winners and losers. You could pick nits on the definition of the term zero sum but Bogle explains it thus:

“Trying to beat the stock market is theoretically a zero-sum game (for every winner, there must be a loser), and after the substantial costs of investing are deducted, it becomes a loser’s game.”

There is a key distinction between the stock market (i.e. trading) and the underlying companies that make up a stock market that I think you might be getting mixed up:

Stock market – Let’s take the entire U.S. stock market as an example (represented by the CRSP U.S. Total Market Index). Last year, the index delivered a total return of 33.6%. That was the weighted average return of every company within the index, regardless of who owned what at any time during the year. No matter how the market was traded, the end result was 33.6% (before fees and taxes of course). That is the very definition of a zero-sum game.

Companies – On the other hand, the companies themselves (as participants in a wealth-creating economy) are not playing a zero-sum game. Through innovation, they are able to reduce costs, deliver better products/services, and create things that never before existed. Consumers and businesses who trade money for products/services they place greater value on than the money they gave up are obviously better off. However, to bring it full circle, the companies created an aggregate amount of wealth that is not impacted (in any meaningful way) by how their shares were traded on the stock market.

[…] Conditions Index carolabinder.blogspot.com shared by @MarkThoma, @davidmwessel, @petercoy Stock Corrections After Long Winning Streaks awealthofcommonsense.com “If you have trouble imagining a 20% loss in the stock market, you […]

[…] Stock corrections after long winning streaks (A Wealth of Common Sense). For all who think this bull market is getting a little long in the tooth, there are four that lasted longer. […]

In addition to knowing stats such as these, defining the “risk profile” of the market that is present, can be productive towards knowing if an impending market pullback/correction will be of lower risk to reward (towards allocating new assets towards equities) than at a later time.

[…] Quant study: The history of long winning streaks in the stock market | A Wealth of Common Sense Analyzes historical duration of rallies in which $SPX hasn’t undergone a correction (10% drawdown): – Sample size: 10 postwar bull markets (1950-2014) – Average duration: 36.3 months (3.04 years) – Today’s: 32 months (2.7 years from 11/2011 – 7/2014) – Average subsequent drawdown: -20% mean, -14% median [More evidence that today's secular bull market is still young. Previously: Complete guide to bull & bear markets] #Bullish […]

[…] themselves.” That’s largely because big crashes (as opposed to corrections — which are common) don’t happen all that often. The worst one-day market loss occurred on Black Monday, October […]

A Wealth of Common Sense is a blog that focuses on wealth management, investments, financial markets and investor psychology. I manage portfolios for institutions and individuals at Ritholtz Wealth Management LLC. More about me here. For disclosure information please see here.

Get Some Common Sense

Categories

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

[…] Stock Corrections […]

[…] Corrections happen: you just don’t know when. (A Wealth of Common Sense) […]

Wow, seven years! And followed by only an 11 percent correction? That’s insane!

Honestly I’m not sure what to tell clients when they ask about whether we’re “due” for a correction. Obviously, as you’ve pointed out, these things can last a long time without the market behaving “rationally”.

So my answer is always, I don’t know, and that you should just stay focused on a long term strategy.

[…] at A Wealth of Common Sense gathers data on stock market corrections after long winning streaks. Double digit losses are common following a strong bull market, but the timing is difficult to […]

[…] How bad will the correction be when it finally occurs? And should people be spending every f*cking waking second of their day preoccupied with this question? (AWealthOfCommonSense) […]

The stock market/equities/investing is NOT a zero sum gain. Options and Futures are.

They are in the sense that for every buyer there is a seller and there will be winners and losers. You could pick nits on the definition of the term zero sum but Bogle explains it thus:

“Trying to beat the stock market is theoretically a zero-sum game (for every winner, there must be a loser), and after the substantial costs of investing are deducted, it becomes a loser’s game.”

Antony,

There is a key distinction between the stock market (i.e. trading) and the underlying companies that make up a stock market that I think you might be getting mixed up:

Stock market – Let’s take the entire U.S. stock market as an example (represented by the CRSP U.S. Total Market Index). Last year, the index delivered a total return of 33.6%. That was the weighted average return of every company within the index, regardless of who owned what at any time during the year. No matter how the market was traded, the end result was 33.6% (before fees and taxes of course). That is the very definition of a zero-sum game.

Companies – On the other hand, the companies themselves (as participants in a wealth-creating economy) are not playing a zero-sum game. Through innovation, they are able to reduce costs, deliver better products/services, and create things that never before existed. Consumers and businesses who trade money for products/services they place greater value on than the money they gave up are obviously better off. However, to bring it full circle, the companies created an aggregate amount of wealth that is not impacted (in any meaningful way) by how their shares were traded on the stock market.

[…] Conditions Index carolabinder.blogspot.com shared by @MarkThoma, @davidmwessel, @petercoy Stock Corrections After Long Winning Streaks awealthofcommonsense.com “If you have trouble imagining a 20% loss in the stock market, you […]

[…] Stock corrections after long winning streaks (A Wealth of Common Sense). For all who think this bull market is getting a little long in the tooth, there are four that lasted longer. […]

In addition to knowing stats such as these, defining the “risk profile” of the market that is present, can be productive towards knowing if an impending market pullback/correction will be of lower risk to reward (towards allocating new assets towards equities) than at a later time.

presentation here … https://docs.google.com/presentation/d/1GlQ9kfz20G_qWcEZpIaAdkGa8Vr5mD8_A-dFRGvEE0s/edit?usp=sharing

http://stockmarketmap.wordpress.com/

[…] Quant study: The history of long winning streaks in the stock market | A Wealth of Common Sense Analyzes historical duration of rallies in which $SPX hasn’t undergone a correction (10% drawdown): – Sample size: 10 postwar bull markets (1950-2014) – Average duration: 36.3 months (3.04 years) – Today’s: 32 months (2.7 years from 11/2011 – 7/2014) – Average subsequent drawdown: -20% mean, -14% median [More evidence that today's secular bull market is still young. Previously: Complete guide to bull & bear markets] #Bullish […]

[…] From A Wealth of Common Sense. […]

[…] themselves.” That’s largely because big crashes (as opposed to corrections — which are common) don’t happen all that often. The worst one-day market loss occurred on Black Monday, October […]