“Keep one eye fixed on the details; the other, on the horizon.” – Unknown

Although we have experienced some wild swings along the way, stock market returns over the past 10 and 20 year periods are actually not that far off the long-term averages. Through September 30, the 10 year annual returns for the S&P 500 are 7.6%. The 20 year annual returns are 8.8%.

Not bad considering we’ve lived through two huge crashes and the worst economic downturn since the Great Depression. It’s not easy sitting tight with your plan through the ups and downs that we’ve experienced but if you can the payoff over the long-term has historically been worth it.

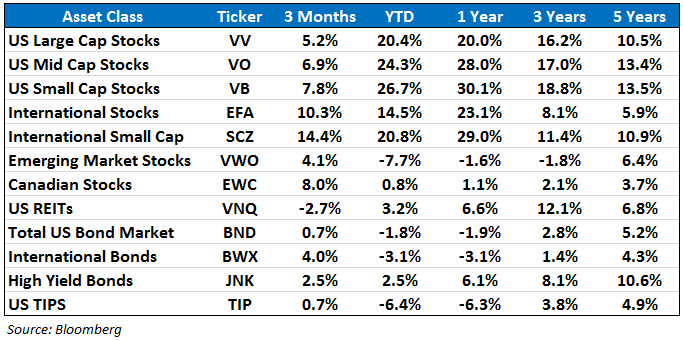

Here’s a snapshot of how some of the other major stock and bond markets are performing through the end of the third quarter based on various ETFs over different time frames:

US stocks continue their almost uninterrupted rise as large, mid and small stocks are all up over 20% three-quarters of the way through the year. The 5 year numbers look excellent as well, but be aware that the performance from the financial crisis is now starting to drop off for 5 year numbers.

Wall Street salespeople will use this to their advantage.

Many investors tend to base their investment decisions on the ‘what have you done for me lately?’ philosophy. Don’t let past returns affect your long-term investment plan as it’s easy to play the ‘what if?’ game after seeing solid gains in the recent past. Chasing performance is a great way to buy high and sell low.

Focusing on long-term performance is the key for investors but they are not a useful indicator for making short-term investment decisions. No one knows what the market will do in the short-term.

It’s also interesting to note that bonds have been a loser on a relative and absolute basis this year, although the losses are still fairly contained up to this point. TIPS (inflation protected bonds) have seen the largest losses this year as inflation has continued to stay much lower than the experts have been predicting.

You may not be invested in all of these markets but as your quarterly statements start to roll in it makes sense to check your performance numbers and make sure you are still on track with your savings goals.

You can use these performance figures to see if any markets look undervalued for rebalancing purposes. Your asset allocation might be out of whack from rising stock prices or falling bond prices. If your plan calls for a periodic rebalance, stick to it and don’t try to guess what the markets will do over the short-term.

In the absence of a periodic rebalance, doing nothing and sticking to your long-term plan are your best bets.

[widgets_on_pages]