“Education is what remains after one has forgotten everything he learned in school.” – Albert Einstein

Common sense reader mailbag: I have two young children. How will I ever be able to afford to send them both to college?

Obviously, with the high cost of tuition and the amount of student loans that younger generations are being saddled with upon graduation this is an important topic for parents to consider.

According to Brett Arends of the Wall Street Journal, in the past 40 years the cost of tuition and fees at private universities has tripled. At public universities it has quadrupled. And that is after accounting for inflation. Unbelievable, but true.

And here is his take on the state of student loans:

“It is, as a result, no surprise that total student loans are now approaching $1 trillion. They have easily overtaken credit-card debts and car loans. According to the Federal Reserve Bank of New York, total student loans have basically tripled since 2004. Fed researcher Lee Donghoon says that in the last eight years the number of borrowers has gone up by about 70%, and the average amount owed has also gone up about 70%. Donghoon calculates that about 17% of those with student loans are more than 90 days’ delinquent on their interest payments. Yet he also calculates that 44% haven’t even entered the repayment period at all.”

With the importance of the college degree in a tough job market I don’t see this changing anytime soon. It’s easy to complain about these numbers, but focusing on the problems of higher education won’t help you pay the tuition bills. You still need a plan of attack.

TAKE THE STANDARD ADVICE?

The general rule of thumb from financial experts is that saving for your children’s college fund should never take precedence over saving for your own retirement. In the event of a plane crash they always tell you to put on your oxygen mask before attending to your children.

Not a pretty metaphor, but that’s the general idea behind this theory. If you sacrifice your retirement to put your kids through college and end up woefully unprepared when you leave the workforce they will probably have to take care of you anyways. That’s why it doesn’t make sense to make that tradeoff.

And this does make sense in theory. But try telling a parent that they should look out for their own well-being ahead of their child’s. It’s just not realistic to assume that this will happen in the real world. Parents generally want the absolute best for their kids.

SO, WHAT ARE YOUR OPTIONS?

As with all financial decisions, you don’t necessarily have to choose one extreme or the other. It doesn’t have to be all retirement savings with no college savings or vice versa.

There should be room in your financial plan for a balance of both options. You definitely should not let saving for college supplant all of your retirement savings. The longer to save now the less you have to save in the future because of the benefits of compound interest. This is especially true if you get a company match through a 401(k) plan.

You just have to be realistic, plan ahead and be honest with yourself and your children. Here are some tips to consider how you can look at saving for your children’s college education:

(1) Start Early: The earlier you start saving the less you have to save overall (again, this is because of compound interest). College costs are obviously increasing at a greater rate than inflation so you will have to gradually increase the amount you save over the years as well.

By starting early you give yourself almost 20 years to save and invest. Small amounts of money saved over that period of time can really start to add up. If you save $75 a month, increase that amount by 2%* per year for inflation and are able to earn 6% on your money, you would end up with over $40,000 after 20 years.

*Increasing that amount by 2% a year means in the last year you would only be saving a little over $100 so feel free to increase by more than that to increase your odds of success.

You could also tell family members to forgo the usual toy and clothes gifts when your kids are young and instead ask for contributions to your 529 plan to further increase the balance. This could make for a boring birthday party but a better (or at least less stressful) graduation party.

(2) Be Realistic: There do have to be some sacrifices made if you are having trouble saving for all of your financial goals. Not every family will be able to foot the bill for their children to go to the best private schools.

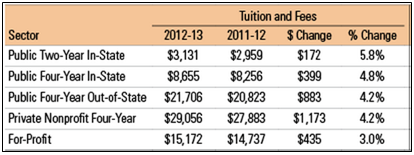

Here are the latest average tuition numbers from The College Board:

As you can see, private colleges average close to $30,000 a year in tuition (and this doesn’t include room and board). But moving down the line a four year in-state public university averages less than $9,000 a year while community colleges are closer to $3,000 per year.

If you run the numbers and realize your savings will never be able to stretch for a private school then there’s no shame in trying to save enough for the average public university. In fact, this is exactly what you should do if you plan on retiring someday.

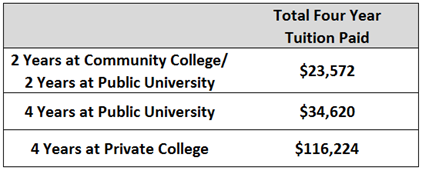

Another option could be sending your kids to a community college for the first two years (where they will be taking their core classes anyways) and then paying for them to finish at a public university. The experience won’t be quite the same, but the end goal of getting a degree will still be achieved.

Here is how these options look at the current tuition levels (although this doesn’t account for future inflation):

(3) Be Honest: Being realistic about paying for college will require that you are honest with both yourself and with your children. No one likes to talk about their financial situation, especially among family members. This is as good of a topic as any to get started.

Tell your kids early on in their high school years that you will only be able to save enough for them to attend a public university (or a combination of community college and a public university). Anything above and beyond that will be up to them through a combination of scholarships, jobs and student loans.

This would also be a good time to discuss the dangers of debt (both credit card and student loans). Obviously, student loan debt is a much better investment than credit cards so if they would still like to pursue a private school education at least part of it can be paid for from your end.

This way you can feel good about the fact that you are giving your children the option of having a fully paid college education without completely sabotaging your retirement goals.

TRACK YOUR PROGESS

You also need to remember that circumstances change. Track your progress on an annual basis and make course corrections along the way. If you start early enough you should be able to compare how you are doing with your actual results versus your retirement and college savings goals.

If it looks like your investment returns aren’t coming in as you expected you might need to save a little more to get back on track. Or maybe you change jobs and have a higher salary so now you are able save more. Whatever your situation may be, you have to be flexible to make changes with any long-term financial goal. This one is no different.

Sources:

Trends in Higher Education

Dear Class of ’13: You’ve Been Scammed

Five Really Dumb Money Moves You’ve Got to Avoid

Further Reading:

Morningstar Names Best 529 College-Savings Plans for 2012

How Much Does Your College Degree Matter?

Don’t Send Your Kids to College

[widgets_on_pages]

Why in society today are we still struggling to pay for education? We are still talking about whether a parent’s retirement plan should take precedence over a child’s ability to go to college. We are still trying to make financial decisions that can make education for our children possible.

We continue to tread this path when there is already a solution. The World Education University (WEU) has made education accessible at anytime, anywhere for FREE. WEU provides online, self-paced, competency based education to citizens around the world for free.

We can stop questioning how we are going to help our children achieve their dreams of college because WEU has given the world an answer to today’s education crisis. Their goal is to educate and inspire global citizens by breaking down economic barriers to education.

So instead of worrying about the finances behind higher learning focus on giving your child an excellent education expense FREE.

Sounds similar to the Khan Academy. Unfortunately most of the free web-based education platforms are not accepted as currency for gainful employment. Until that happens, a college degree is going to continue to be important, whether it’s fair or not.

World Education University currently offers 43 different degrees and certificate programs in high demand fields such as computer and information science, healthcare and business, with new programs being created continously to meet international job market trends.

WEU has created a cognitive learning environment consistent with the demands of the 21st century. It is unique in its mission to create a difference and help world consumers who lack, need, and demand educational content.

How could you not encourage people to be in control of their own future at NO COST to them?

You can research their degrees and courses at http://www.theWEU.com

[…] example, let’s say you know for sure that you have to make your first college tuition payment in five years and would like to buy a relatively safe investment based on that time […]