“Unless you can watch your stock holdings decline by 50% without becoming panic-stricken, you should not be in the stock market.” – Warren Buffett

We have had a really nice run up in stocks since the lows of 2009. Most U.S. stock markets are up well over 100% in that time. It hasn’t been easy as stocks have climbed the proverbial wall of worry (subpar economic growth, high unemployment, etc.) to get here. After the largest weekly losses of 2013 last week it’s a good time to remind ourselves that stocks can and will go down. Every investment will disappoint you at some point over the long haul.

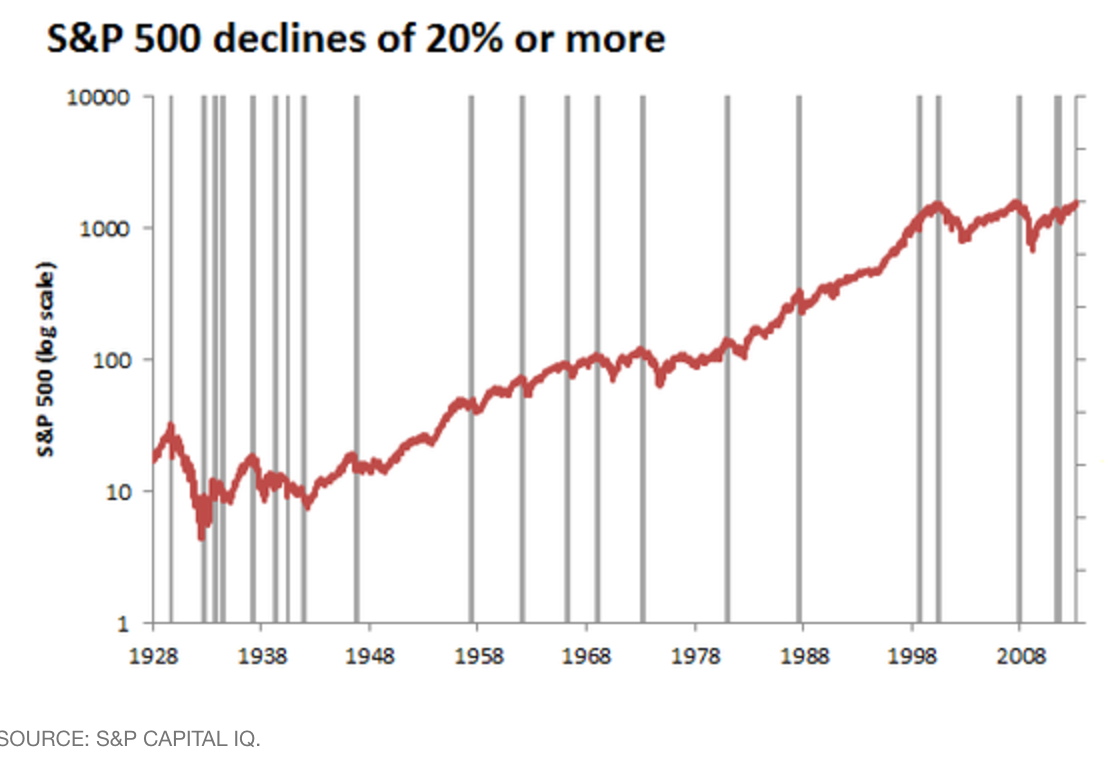

According to Morgan Housel at The Motley Fool, since 1928, there have been 20 periods of a 20% or more decline in the S&P 500. In this same time frame, after accounting for inflation and dividends, the stock market increased over 140-fold. So even though the market averaged at least a 20% decline every 4.5 years, investors still made 140 times their money after inflation. Here is a graph included in the article that shows this phenomenon (the gray bars are the 20% declines):

Housel goes on to tell us in another article:

“Take the highest level the S&P 500 traded at in every decade going back to 1880. At some point during the subsequent 10 years, stocks fell at least 10% every single time, with an average decline of 39%. Market crashes are perfectly normal.”

I broke down the monthly returns of the S&P 500 going back to 1956. In that time frame, the S&P 500 has lost more than 5% in a single month in 59 times (8.6% of the time). And there were 7 times where the market lost more than 10% in a month.

Another stat from The Reformed Broker that I’ve touched on before:

Over the last 110 years markets have averaged three 5% corrections per year, one 10% per year and one 20% every three and a half years.

I think you get the point. Stocks do fall periodically. The high frequency of losses is an unfortunate bi-product of investing in stocks. It’s a double-edged sword.

The reason that stocks tend to have higher returns than other asset classes (like bonds and cash) is because investors demand a higher return on their money to offset the risk of large losses. It’s sort of like the chicken and the egg problem. We get higher returns because of the potential for large losses. And we get large losses because of the potential for higher returns.

WHAT TO DO IF STOCKS FALL?

Don’t panic. Those who sold at the bottom in 2009 are really hurting at this point. If you know stocks will go down at some point in the future, what can you do to combat this? First of all, do not try to time the market on a consistent basis. This is a challenge for even the best investors.

Did Warren Buffett sell all of his stocks before the 2008 crash? No, but he did have some dry powder in cash to buy more shares when stocks did fall. His investment plan consists of holding stocks for a really long time while also having cash reserves to buy when stocks fall.

You don’t need to have Buffett’s plan to succeed. But the best thing you can do is to have a plan in place that allows you to know what to do whether the market keeps rising further or sticks to the historical script and has one of the average declines we’ve seen in the past. Your behavioral biases can affect your investment results so having a plan in place is one of the best ways to minimize mistakes.

Dollar cost averaging into the market by making your contributions on a periodic basis is a good place to start. Don’t try to make your buy and sell decisions based on the level of the market or the performance of the economy. If you had done this strategy in the past four years you probably never would have made any purchases of stocks and would have missed out on all of the gains.

If you are closer to retirement these periodic stock losses will really sting, especially if you need to take distributions. That’s why having a diversified portfolio with some cash on hand helps you ride out some losses. But if you are a younger investor who follows a dollar cost average program you should welcome the occasional loss. It’s no fun seeing your balance decline but you are buying more shares at a lower cost, thus increasing your future returns.

You can also rebalance to your targeted asset allocation weights to make sure you stay within your defined risk limits. A simple portfolio of stocks and bonds will allow you to make these changes on a periodic basis. You will sell stocks when they have run up to lock in some gains and buy stocks when they drop in price to increase future returns. You can add other investments to diversify further, as well (real estate, commodities, etc.).

Stocks may not perform as well in the future, but using the past as a framework for evaluating the present and future is a very sensible way to invest.

These strategies will keep you on the slow and steady track to building wealth. They don’t make the pain of losses any easier. But take a look at the red line on the graph above showing the stock market over a long time horizon. The trend is up even though there are bumps along the way and it’s not definitely a straight line. That should help you stick to your investment plan when things get dicey and stocks fall.

Sources:

Patient investors will always win

25 important things to remember as an investor

Now onto this week’s best reads from around the web:

- What would you do if money was no object? (Reach Financial Independence)

- Twitter is becoming your first source for investment news (Washington Post)

- The perils of investing in what you know (NY Times)

- What to do with your tax refund (Wall Street Journal)

- Big market drops happen more often than you think (CBS Moneywatch)

- Nate Silver: confidence kills predictions (Index Universe)

- Before housing bubbles there was land fever (NY Times)

- Best financial decision? (MarketWatch)

- Are you an investor or a story teller? (The Big Picture)

[…] Stocks Will Go Down, Ben Carlson wrote an excellent post reminding investors that markets do move in both directions. […]

When you look at Buffett’s plan that way it seems very simple and is something even the most inexperienced investor can emulate. If you’re in it for the long haul, can stay calm during the turbulent times and can pick up a few bargains along the way, then you should be sitting on a nice return in the decades to come. Great post.

Thanks. Buffett even says something along the lines of investing is simple but not easy. Investing is very counterintuitive. Your time horizon is also a big factor.

I like that quote from Warren Buffett and believe it is so true. You’ve done a good job pointing out that we can pretty much expect to experience some 20% or so market declines around every 5 years at least. It’s important to believe in the investing plan and realize that things will turn around. These drops in the market are times to take advantage and buy more shares rather than panic. It’s always good to remind investors of this.

Hard to believe but true that we have those periodic sells offs. I read today that this will be the first Jan-May period in 17 years we didn’t have at least one 5% correction. I can’t predict the future but I would say that doesn’t bode well for the next few months. But the next few months shouldn’t matter to long-term investors. Let the day traders worry about the short-term.

[…] Stocks Will Go Down – I really liked this article from A Wealth of Common Sense because it is a great reminder that the stock market sometimes will go down. It’s my opinion that if you won’t be able to handle a downturn of the stock market of 20% or more every few years then you shouldn’t be invested in the market. Market downturns are opportunities to take advantage of and purchase shares on sale, not a time to panic and sell. […]

[…] the market tends to have losses on a periodic basis it can be very hard for even the smartest investors to make these kinds of […]

[…] Stock losses do happen periodically as we have seen in the past and they will continue to occur going forward, but they are next to impossible to predict. […]

[…] able to accept in your portfolio. If you can’t handle the wild swings in price or the fact that stocks will go down periodically then you need to reassess how stocks fit into your […]

[…] Stocks will go down […]

[…] Further Reading: Time to Prepare for the Coming Crash? Stocks Will Go Down […]

[…] Further Reading: Stocks Will Go Down […]

[…] Stocks Will Go Down […]