A reader asks:

I’m a 33-year-old movie producer in LA and have my own company, so no steady salary, but it’s safe to assume I will make anywhere from $40,000 to $150,0000 (impossible to predict). I currently have $125,000 (70% stocks, 30% cash). Personal finances are in good shape (no kids, no debt). I’m currently renting and have a roommate and it sucks. My goal is to get a house by mid-2023 in the valley, preferably sooner. Most of the houses are about $650,000 – $850,000. I have two questions:

Do I need to put myself in a larger cash position since I want to spend the money soon-ish? What is a good ratio?

Should I wait until I have a big enough down payment or go when I find the right place? Is it better to save for a nice large down payment since my annual income varies?

The assumption most people have when going through this process is you need a minimum of 20% down when buying a house.

There are some benefits to having a 20% down payment.

It’s less debt to take on. It gives you an equity cushion in case housing goes in the toilet for a while. And it saves you from paying private mortgage insurance (PMI) which can run you something like $75-$150/month depending on the size of your mortgage.

I get why many homeowners would want to have that 20% down before buying.

But it’s not a prerequisite.

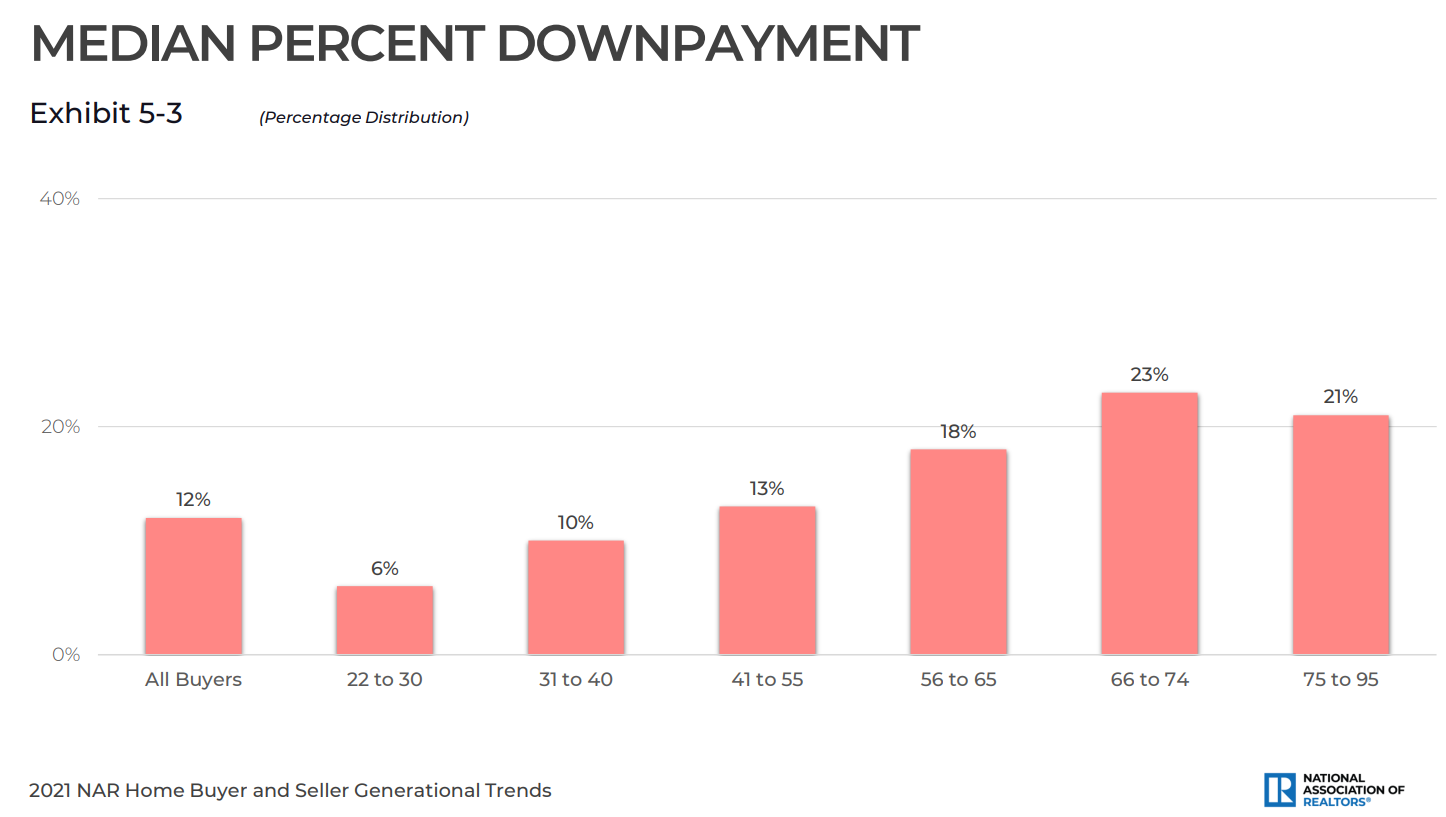

According to a research report from the National Association of Realtors, this is what the median down payment numbers look like overall and across various age brackets:

The median down payment is 12% but you can see it’s much lower for people in their 20s (6%) and 30s (10%).

This makes sense when you consider older people have more financial assets or equity in their current homes to fund a bigger down payment.

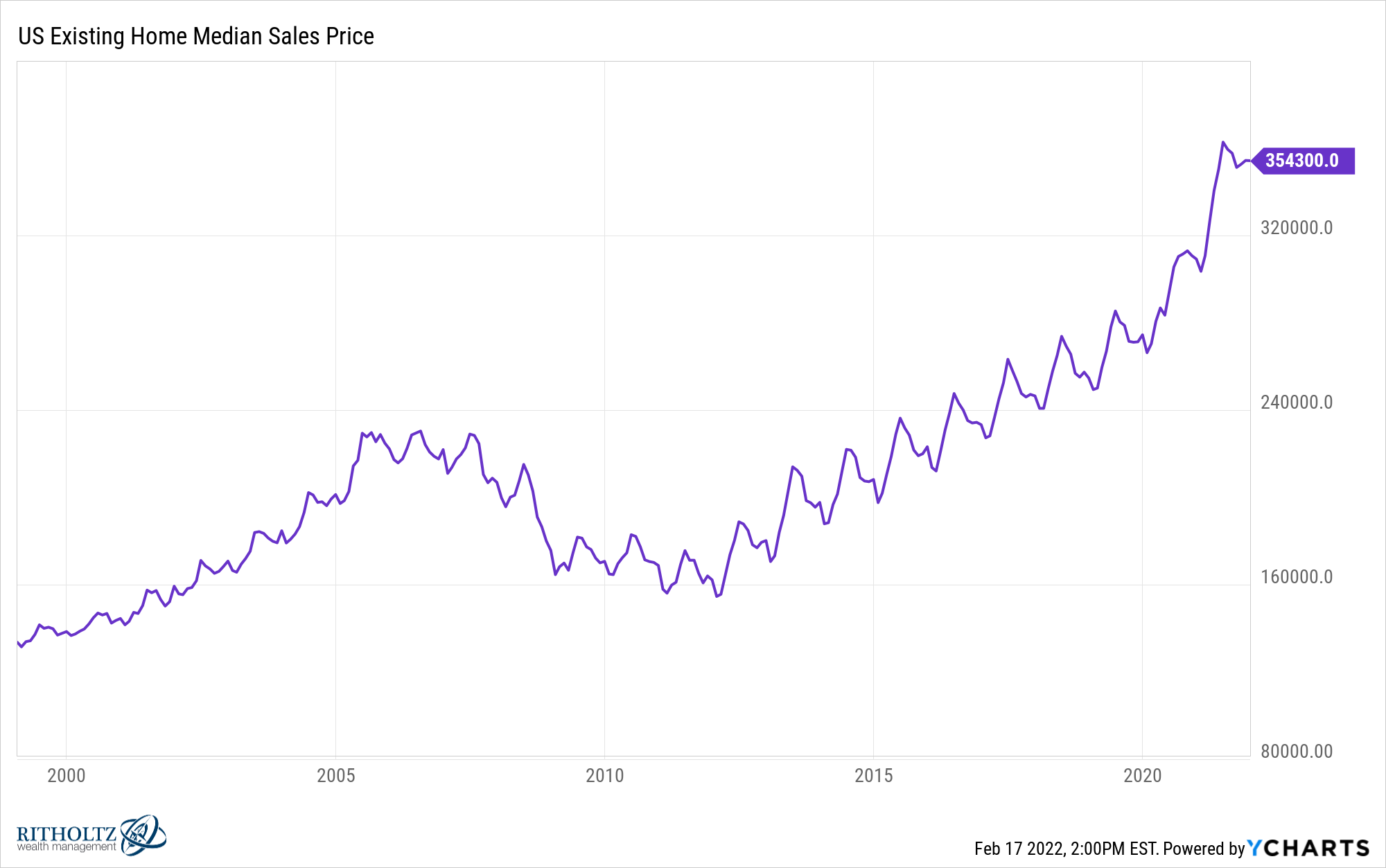

The median sales price for an existing home in the United States is now more than $350,000:

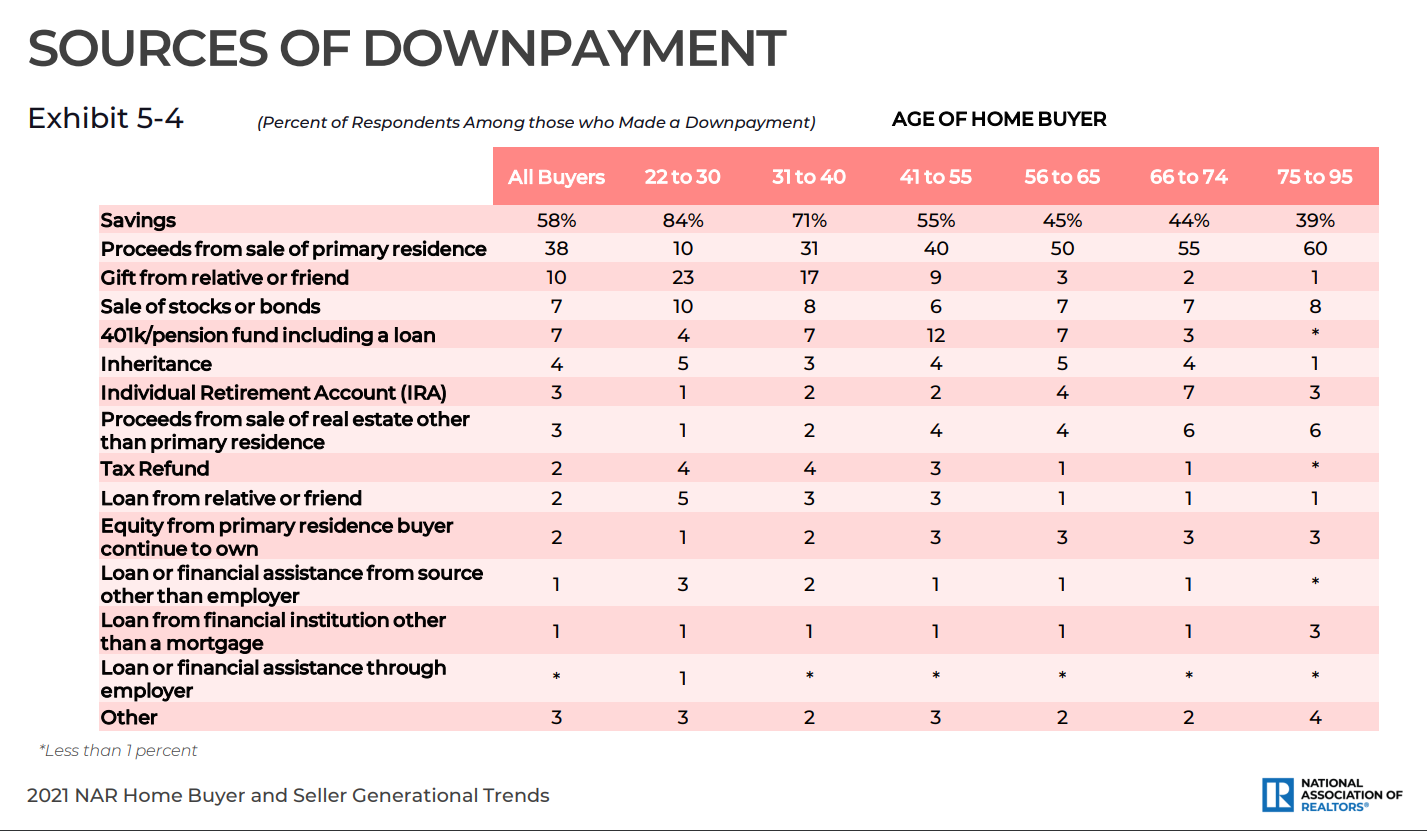

You can see the majority of down payment money for people in their 20s and 30s comes directly from savings:

Here are the down payments at various points for a $354,300 house:

- 5% – $17k

- 10% – $35k

- 15% – $53k

- 20% – $71k

If you saved for 5 years for a house at this price that’s nearly $1,200/month for a 20% down payment. Not everyone can afford to save $1,200/month for 5 years for the luxury of buying a house.

A 20% down payment on a house in the $650k-$850k range is $130k-$170k.

The down payment we made on our first home was just 5%.

And it’s not like we were trying to use as much leverage as possible. That’s all we could afford to be able to move into a house at that time. It would have taken years for us to come up with 20%.

There are options for young people who don’t want to live on ramen noodles every night just so they can save for a down payment.

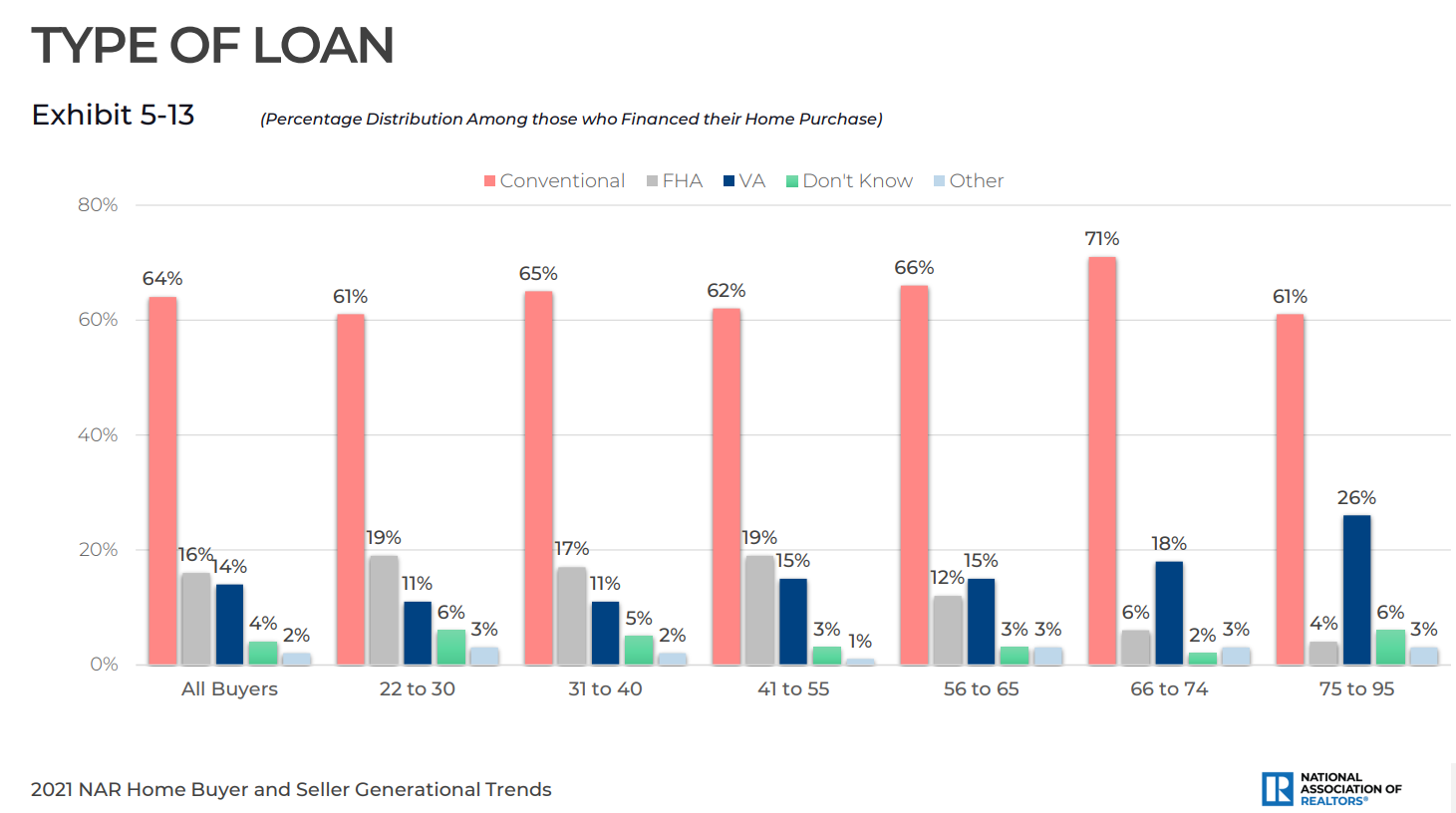

An FHA loan requires just a down payment of as little as 3.5%.

Now some people would scoff at this number and say FHA loans are rare. They certainly aren’t the most prevalent loan. Here’s the breakdown by loan type:

It looks like 1 out of every 5 homebuyers in their 20s and 30s are able to secure one of these loans. It would be nice if that number was higher but it’s not out of the question.

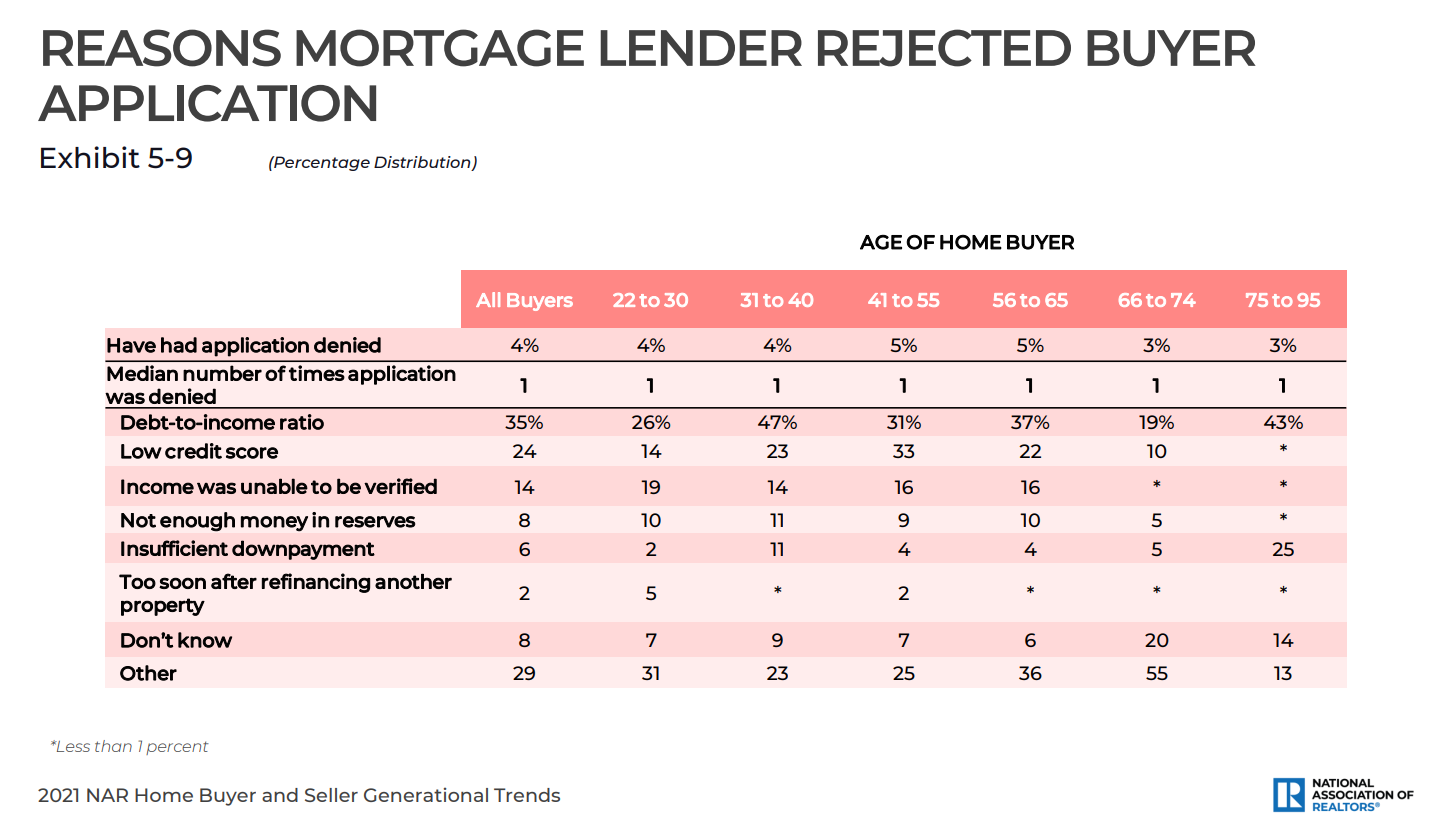

This question probably depends mostly on the lender you choose and your credit score and financial situation. The NAR has a list of the reasons people are rejected on a mortgage application:

It’s actually pretty rare to see an application get denied but the number one reason is a poor debt-to-income ratio.

This is good news for the reader who asked this question. They don’t hold any debt. The variable income component might come up in the application process but that’s why I would suggest shopping around for a number of different lenders.

The Internet makes it much easier to compare rates, fees and such. Beyond banks, you can also check out credit unions and online lending platforms.

Here’s what I would do in this situation:

Shop around for a lender. See what kind of down payment they are looking for. See how much money they are willing to lend you. See what kind of mortgage you get pre-approved for.

And if your variable income is a problem then at least you know maybe you will need a bigger down payment.

Figure out the payment you can handle based on certain down payments. The down payment is important to get started but the only thing that really matters is your ability to meet the monthly payments, taxes, insurance and maintenance involved in homeownership.

Start looking for houses. The process can take longer than you expect, especially with supply so low these days. I would be more worried about finding a house than reaching some mythical down payment goal.

You can always pay down your mortgage early if you go under the 20% down payment threshold to get out from under the PMI payment.

The thing I would not do is try to time the housing market by waiting for prices to fall or a recession or some other macro event.

Buy a house because you like it, you can afford it, you can service the debt and you want to live in it for a number of years.

We talked about this question on this week’s Portfolio Rescue:

I also had Blair duQuesnay back on to answer some questions about 529 plans and employee stock options.

And if you prefer to listen to this episode in podcast form see here:

Further Reading:

What’s a First-Time Homebuyer To Do Right Now?