In my post that looked at housing as an investment I showed historical data going all the way back to 1880 on the investment returns in the housing sector. Then I looked at some of the investment characteristics on housing including the net expenses you pay and its low liquidity when you need to sell. I went on to show you that the after-inflation returns for the average home in the U.S. have not been as great you think. In fact, I challenged the statement that your home should be your biggest investment. It should be looked at as a long-term asset instead of a long-term investment.

So if your home should not be your biggest investment then you need to have a good comparison to see how the alternatives have fared. To get a good comparison let’s take a look at how the real estate investment returns against the stock and bond markets. Since no one really looks at real (or inflation-adjusted) returns we will look at these returns on a nominal (before inflation) basis.

The Case-Shiller Home Price Index will be used for the average return of owning a home. For stocks we will look at the S&P 500 and for bonds 10 Year Treasuries. All three of these do a nice job of showing the broad average return for the real estate, stocks and bonds over the long-term.

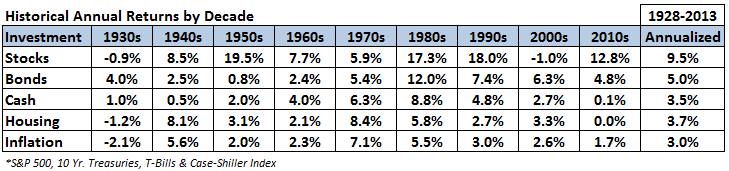

From 1928 to 2012 the Case-Shiller Home Price Index returned 3.71% per year. So it just barely beats the long-term rate of inflation (about 3.35% per year). Stocks returned 9.31% a year and bonds had an annual return of 5.10%. Obviously stocks are the big winner among the three in this 85 year period. Here is a chart that shows how these investments performed in each of the past 8 decades to get a better sense of how they match up over different investment periods:

As you can see the returns of each asset class have varied over time. Changing business cycles, interest rate environments and investor confidence have made each asset class a better bet at certain times of the investment landscape. You can see that during the highly inflationary decade in the 1970s housing actually did relatively well when compared to stocks and bonds. Each asset class had its day which is why diversification matters over the long haul.

Just because housing should not be considered your biggest investment doesn’t mean that it’s not an asset to you in the long-run. The common sense rule of being diversified means that you should have a wide variety of assets and investments in your portfolio. Your house should not make up the bulk of your investments just like you wouldn’t bet your entire retirement portfolio on one stock that you are purchasing with borrowed money.

This doesn’t mean you can’t make money on real estate investments. There have been many great opportunities over the years to buy real estate in different parts of the country. The most overused quote in real estate is location, location, location. I would argue that if you are trying to be a real estate investor a close second should be timing, timing, timing.

This is a game that is best left to the pros. Even they get it wrong as we saw from the carnage that the housing bubble caused in 2006 through 2008 and the ripple effects it had on the economy. In fact, you could argue that many property buyers will do pretty well on their purchases made in the 2009 to 2011 time frame in many markets with prices being slashed and interest rates at generational lows.

You just have to be realistic about housing as an investment. As you can see from the numbers above housing does not keep pace with stocks or bonds in the long-term. If you do consider investing in real estate you better have a good idea of what you are doing.

Leverage is a double-edged sword and taking out a mortgage counts as leverage. The longer your holding period in real estate, the lower your leverage turns out to be as it decreases over time. This forces you to be a short-term investor in real estate to make substantial money. That can be dangerous if you don’t know what you are doing.

Another option is to add Real Estate Investment Trusts (REITs) to your investment portfolio. These are securities that trade just like stocks but give you a diversified portfolio of real estate holdings in mortgages, offices, apartments, hotels and commercial properties.

They are a high yielding investment so you get the bonus of an income and growth component. Your 401(k) should have a REIT fund as an option. If not, all of the fund companies offer them as mutual funds or ETFs to be used in an IRA.

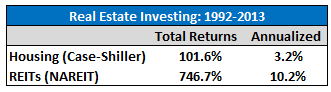

Not only do you get the benefit of having a diversified portfolio of real estate investments (by sector and geography), but you get better liquidity and better average returns over the years. From 1992 to 2012 the NAREIT Index had a total return of 720.46% or 10.54% per year. Over the same time frame the Case-Shiller Home Price Index had a total return of 81.14% or 2.87% per year.

Take a look at the table below to see how each has performed since 1992:

To recap, with REITs you get better liquidity, a source of income, diversification and historically better investment returns. Plus you have the added bonus of being able to make them part of the equity portion your investment plan through mutual funds and ETFs. This allows you to rebalance your real estate investments within your asset allocation.

There are many benefits to being a homeowner with a real estate investment. Just don’t be fooled into thinking it is the best use of all of your investment dollars in the long-run. As with all investments, the price you pay and valuation at the time of purchase can have a huge effect on your end result.

Make sure you diversify your investments across a wide variety of assets and always consider the alternatives before making an investment decision. This is especially true in the real estate sector.

Remember – the tax savings from the interest write off can also be substantial.

That is true. Especially for those with large incomes and expensive homes. For those with more modest homes and incomes the benefit isn’t quite as great because the standard deduction for married couples is $11,900 for 2012. So there is a larger hurdle to jump over. But it’s a good idea to look at all aspects (including tax benefits) when making this decision. Thanks for the comment.

[…] Home Price Index bears his name). Interesting thoughts on what some refer to as their biggest investment. Remember to consider all variables when making an investment. Real estate can be a good investment […]

[…] How shitty? A Wealth of Common Sense explains: […]

Most physical investments in real estate are active. Unless you are talking about investing in REITs which as your graph shows above is not exactly correlated to actual housing prices.