“Volatility can prey on investors’ emotions, reducing the probability they’ll do the right thing.” – Howard Marks

Volatility is the most frequently used measure of risk in the finance industry as Howard Marks observed in his latest memo on what risk really means:

Volatility is the academic’s choice for defining and measuring risk. I think this is the case largely because volatility is quantifiable and thus usable in the calculations and models of modern finance theory.

However, while volatility is quantifiable and machinable – and can also be an indicator or symptom of riskiness and even a specific form of risk – I think it falls short as “the” definition of investment risk. In thinking about risk, we want to identify the thing that investors worry about and thus demand compensation for bearing. I don’t think most investors fear volatility. […] What they fear is the possibility of permanent loss.

Risk is a tricky factor to define and measure. In theory, higher volatility leads to higher risk, which should lead to higher expected returns. Over the long-term this has generally been the case as stocks have earned higher performance than both bonds and cash over very long time horizons with higher levels of volatility.

While you would expect these trends to continue, over shorter time frames these relationships don’t always hold. The performance and volatility numbers for the S&P 500 and long-term treasuries over the last decade or so are a case in point.

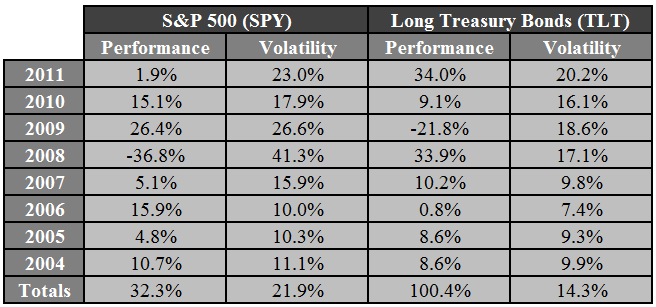

Here’s the data for each from 2004 to 2011:

Stocks experienced much higher volatility but lower returns than long bonds over this period, not what you would expect from the risk-reward relationship. It’s also interesting to note that the highest period for bond volatility was 2011, when long bonds were up 34%. Volatility isn’t only a downside phenomenon.

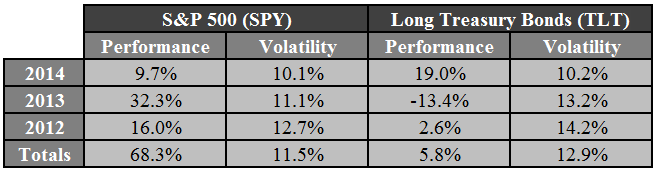

Now take a look at the data from 2012 to 2014:

Lately, the roles have reversed with stocks outperforming long bonds, but with lower volatility. Stocks have earned better returns with roughly 60% of their average volatility over the past decade. These numbers are also a good reminder of the fact that longer-dated fixed income doesn’t offer the stability that many investors look for in bonds.

Obviously, the financial crisis weighs heavily on these results, but they also show that the perception of volatility can play a large role in shaping investor tolerance for risk. Stocks were perceived to be much riskier after a period of higher volatility while bonds were perceived to be less risky.

If I was a pundit I would make the claim that this will end badly and that volatility in stocks is due for a spike. I’m sure that this will happen eventually, but it’s also true that bonds experience higher levels of volatility at lower interest rates and longer maturities, all else equal. Both could stay subdued for a period of time or both could see more fluctuations in price. They don’t necessarily have to follow the same path as the we’ve experienced historically.

There are many other factors at play here besides risk perception including the fact that the interest rate on long-term U.S. treasuries has dropped from 5.2% in 2004 to 3.2% in 2014. With rates not having room to fall much further, bond investors should be prepared for higher volatility and lower returns than we’ve seen in the past.

These numbers also show that it’s usually a good idea to buy stocks during periods of increased volatility and low returns. These times are often followed by periods of higher returns and decreased volatility.

I continue to believe that the biggest risk investors face is not volatility, but how they react to it.

Source:

Risk Revisited (Oaktree)

Further Reading:

Volatility is not your enemy

Subscribe to receive email updates and my monthly newsletter by clicking here.

Follow me on Twitter: @awealthofcs

[…] Role Reversal for Stocks and Bonds […]

[…] The biggest risk investors face is not volatility, but how they react to it. (WealthOfCommonSense) […]

I agree, volatility is not to be feared but welcomed, since it can be on the upside as well as the downside. The key, as one wise investor told me a long time ago, is NEVER SELL IN A DOWN MARKET! Always have sufficient reserves in a bond ladder to support your needs for at least five years, so that you are not forced to sell when you should not.

Well said. If avg investors simply stuck to the ‘don’t sell after a crash’ line of advice they’d all be much better off.

[…] Volatility is less important than our reaction to it. (A Wealth of Common Sense) […]

[…] Smart Beta: Not New, Not Beta, Still Awesome (Cliff Asness) A Role Reversal For Stocks and Bonds (A Wealth of Common Sense) Why the Guardian is smart to bet on live events and a membership model instead of paywalls […]