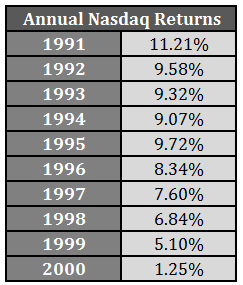

One of the most interesting aspects of asset bubbles is that they pull returns forward from future years. Or on the flipside, they lead to lower returns for a number of years when you invest closer to the peak. The NASDAQ was down 80% after the tech bubble burst following the nearly 500% performance during the last 5 years of the 1990s.

You can see from the annual returns at different starting points how this affected future performance (all returns through 2014):

This works in the opposite direction during a huge bull market as returns have been close to 20% annually since the 2009 recovery took hold. The NASDAQ has been either a horrible or pretty great market to be invested in depending on the starting date and your time horizon.

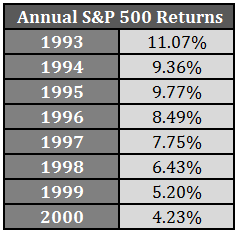

The S&P 500 didn’t rise or fall nearly as much as the tech-heavy NASDAQ in the 1990s, but it still got cut in half between 2000 and 2002. There’s a similar pattern of lower returns as the start date approaches the year 2000:

Alan Greenspan gave his famous Irrational Exuberance speech in December of 1996. Using the 1997 start date, you can see that the S&P 500 is up almost 8% per year since then. The longer-term returns since the mid-1990s have been right around the long-term averages. Since the tech bubble peak, the returns are well below average. Certain investors or pundits will try to use these numbers to their advantage by pointing out whichever data set applies to their narrative — markets either always work or are always risky.

What the perma crowd fails to tell you is that the only thing these numbers tell you — both above and below average — is that the markets are cyclical and come with risks to both the upside and the downside. Patience can be a great equalizer in the financial markets, but it usually has to be measured in decades, not just years.

Here is a quick thought on attitude, but I think an important one. When one states that asset bubbles pull forward returns from future years, this is a ‘glass half empty’ attitude. Equally true is that the glass is half full, that is, deep bear markets push returns into future years. I prefer the latter because it emphasizes that investors should plow money into stocks when they are deeply discounted if they want to maximize future returns.

Well said and that’s an attitude that not many people have unfortunately. If I could wave my magic wand to help people’s finances the two things I would do would be 1) make them save more money and 2) make them understand that stocks falling is a good thing if you’re going to be a net saver in the future.

It’s a very difficult concept for investors to grasp.

A Wealth of Common Sense is a blog that focuses on wealth management, investments, financial markets and investor psychology. I manage portfolios for institutions and individuals at Ritholtz Wealth Management LLC. More about me here. For disclosure information please see here.

Get Some Common Sense

Categories

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

Here is a quick thought on attitude, but I think an important one. When one states that asset bubbles pull forward returns from future years, this is a ‘glass half empty’ attitude. Equally true is that the glass is half full, that is, deep bear markets push returns into future years. I prefer the latter because it emphasizes that investors should plow money into stocks when they are deeply discounted if they want to maximize future returns.

Well said and that’s an attitude that not many people have unfortunately. If I could wave my magic wand to help people’s finances the two things I would do would be 1) make them save more money and 2) make them understand that stocks falling is a good thing if you’re going to be a net saver in the future.

It’s a very difficult concept for investors to grasp.

[…] 4) How Bubbles Impact Future Returns by Ben Carlson via Wealth Of Common Sense […]

[…] 4) How Bubbles Impact Future Returns by Ben Carlson via Wealth Of Common Sense […]

[…] 4) How Bubbles Impact Future Returns by Ben Carlson via Wealth Of Common Sense […]

[…] 4) How Bubbles Impact Future Returns by Ben Carlson via Wealth Of Common Sense […]