I get a lot of questions from investors, advisors, and institutions for my thoughts about alternative assets. I get it. Valuations in U.S. stocks are high. Interest rates are low. Investing globally can be a scary proposition for some. People have an aversion to volatility.

The strategy I’m asked about more than any other is managed futures and the fund I’m asked about more than any other is the AQR Managed Futures Strategy (AQMIX).

Managed futures performed really well in 2008, finishing that year very much in positive territory as a group when stocks got slaughtered along with just about everything else other than government bonds. And AQR, the firm founded by quant investor extraordinaire Cliff Asness, is the most well-known firm for implementing academically-tested quantitatively driven alternative investment strategies in mutual funds at a relatively low cost.

So financial advisors have taken a liking to this fund, so much so that it now has close to $13 billion in assets.

Advisors and investors alike are dealing with a difficult period in this fund’s history at the moment. From the start of March 2016 through the end of March 2017 the fund is down more than 13%. A double-digit drawdown is never any fun but this one may be even more painful considering the fact that the S&P 500 is up almost 25% in that time frame. Here’s a breakdown of these performance numbers along with bonds and a 60/40 portfolio:

Many investors would look at these number and assume that managed futures are obviously not worth the risk. Why would you ever venture outside of stocks and bonds? The problem with this type of analysis is that it’s far too short of a window to make concrete conclusions. Stocks have been lights out over the past year or so. Now take a look at the performance numbers in the first two months of 2016:

Now we see a much different story. Stocks got hit, bonds did pretty well but managed futures did very well. Of course, this is another short time frame but it’s a nice illustration of how alternative assets can work in different market environments. These funds often act as a form of insurance when things go wrong in stocks but that insurance comes with a price.

Managed futures is a strategy that, at its core, relies on trends or momentum. Momentum is the idea that assets that have performed relatively well (poorly) recently will continue to perform well (poorly) going forward, at least for a short period of time. The best explanation for trends is that people are slow to update their views when presented with new evidence, data or information.

This initial underreaction is eventually followed by an overreaction when things become more apparent. Both the under- and overreactions cause trends to go on for far longer than textbook theories of fundamentals would have you believe. Hence, managed futures is also known as ‘trend-following’ because the strategy is premised on the ability to ride trends up or down.

Managed futures strategies look to take advantage of this phenomenon by buying assets (through futures contracts) that are rising and short-selling assets that are falling to take advantage of trends in both directions. And they diversify among a wide number of different markets and assets including stocks, bonds, currencies, and commodities. These strategies are typically managed using systematic trading systems (a la AQR) while some do have discretion over their models. Managed futures funds use anywhere from dozens to hundreds of different assets and markets in the trends they follow.

Trends aren’t always so neat and clean so this strategy can run into troubles and it has performed relatively poorly since the crisis ended in 2009.

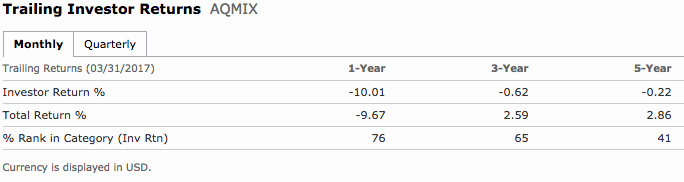

My guess is many investors or advisors don’t really understand how these funds work. They just heard that they did very well in 2008 and come with buzz words like ‘uncorrelated returns’ and the like. Not unlike most other mutual funds, this can lead to behavior gaps between investment and investor returns:

The point here is not to recommend that investors or advisors do or do not utilize managed futures in their portfolios. The point is that investors need to be much more informed when investing outside of traditional asset classes. You have to understand why something works enough to stick with it when it’s not working.

Here are a few thoughts on why investors tend to have a hard time with alternative investments:

- People want uncorrelated assets until they’re uncorrelated to the downside. Investors have a tendency to fight the last war so when people are looking for “uncorrelated assets” what they’re often in search of is “something that did well during the last downturn.” Those assets usually end up being the ones that underperform during the next upturn as well, making it difficult to stay put.

- Very few advisors or investors are experts in these types of strategies. Therefore they rely on fund firms to explain how things work. And very few people in this industry are any good at setting reasonable expectations for these types of funds or explaining how they work in plain English. The gap between perception and reality is often a mile wide. Clients don’t understand what they’re investing in or why. The funds that are marketed most heavily tend to be the ones that have done well recently so investors pile in and out at inopportune times.

- These funds are hard to benchmark. There are no real index funds to compare to in alternatives so it’s hard to make apples-to-apples comparisons on performance numbers. Investors have a hard time understanding if their funds are working or not.

- There are lots of choices in the alternatives space. If and when one fund has a dry spell, there’s always going to be another fund or provider waiting in the wings to take its place. So the performance chase can be never-ending if you never get comfortable with your holdings.

Further Reading:

How Should Alternative Investments Be Benchmarked