The U.S. has the largest, most liquid financial markets in the world. We also have one of the most globalized set of corporations that make up our stock market. The S&P 500 now gets something in the order of 40% of its sales from overseas. Based on this information, I’ve been asked the following question dozens of times over the past year:

Why do I need to invest in foreign stocks when the U.S. companies are now so global and the markets are so highly correlated?

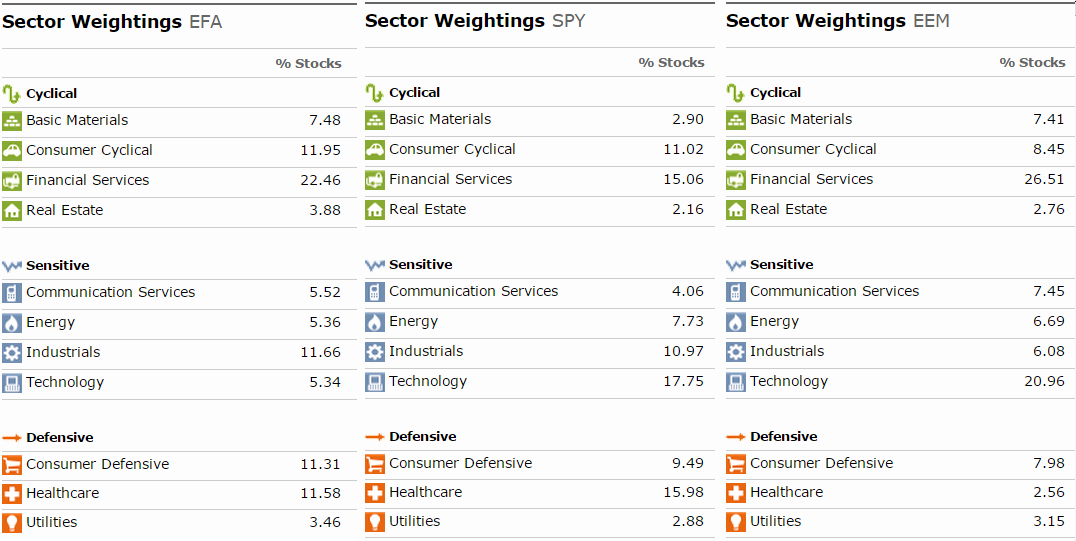

It’s a legitimate question. The way I see it, you’re not only getting geographic diversification by investing in overseas markets. The industry make-up of each market also varies by region. Take a look at the industry breakdown for the S&P 500, MSCI EAFE and MSCI Emerging Markets indexes:

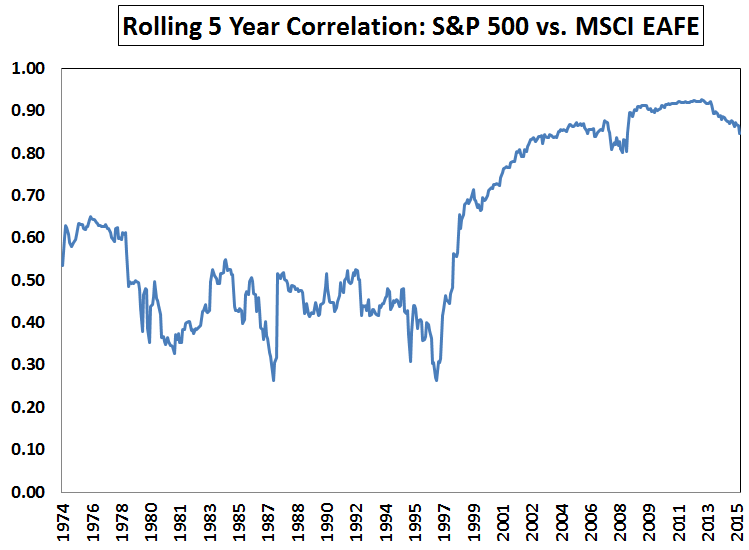

Also, increasing correlations among countries and global markets should be expected as globalization takes hold and economic policy is becoming more coordinated. But increased correlations don’t tell you anything about the outcomes of the different markets. Take a look at the following graph which shows the rolling 5 year correlations between the S&P 500 and the MSCI EAFE index of developed foreign markets:

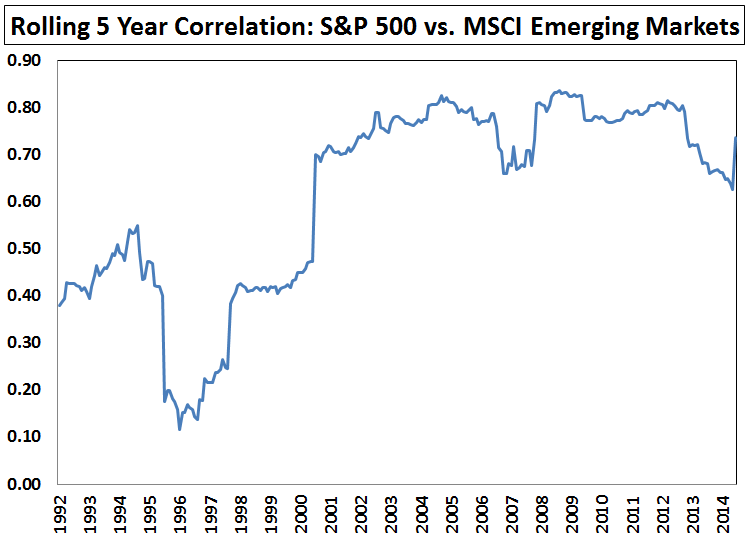

Now here’s the S&P against the MSCI Emerging Markets Index:

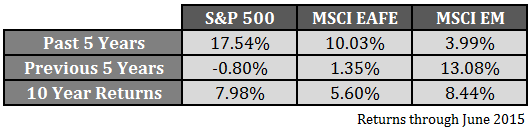

There’s a clear trend over time and it’s true that markets are becoming more correlated. But take a look at the past five year’s worth of returns for these markets along with the previous five years and the past ten years:

The correlations with the S&P 500 to foreign developed and emerging market stocks over the past 5 years were 0.86 and 0.75, respectively. In the previous 5 year period, they were 0.91 and 0.83. But this didn’t lead to similar returns numbers.

Since stocks generally go up over time, investors have to expect that different markets will be correlated with one another, but correlation says nothing about the differences in performance. It’s just statistical relationship that shows they’re generally moving in the same direction.

By investing abroad you’re not only gaining exposure to different countries, industries, currencies and individual companies, but there’s also a cultural element that I think is under-appreciated. No matter how globalized the world becomes, there will always be cultural differences. These differences will affect the way that investors in certain countries or regions will invest. Global diversification allows intelligent investors to take advantage of the reactions, biases and mistakes of investors in other markets. Even with increased correlations, investors around the globe are never going to be completely in sync with one another.

I cover diversification extensively in my book, because I think it’s one of the most important aspects of portfolio management. Here’s my take on global diversification from the book:

Globalization is making the world a flatter place, as technology is slowly leveling the playing field and allowing people from all walks of life to have access to insane amounts of information. There are also sure to be upheavals and crises in different countries and regions around the globe. Increased globalization will, at times, result in spill-over effects into the rest of the world. Other times, crises will be contained in certain areas that don’t have diversified economies or markets.

The United States has been one of the clear winners of the past century in terms of becoming an economic powerhouse and providing investors with juicy returns in risk assets. While the United States has many built-in advantages, remember, that America was once an emerging market too. From the late 1700s to the early 1900s, the United States averaged a recession every two years.

Owning risky assets such as stocks can be thought of as a way to ride the coattails of intelligent people as they continue to innovate. It has never paid to bet against human ingenuity. Investing in foreign markets is a bet that people in other parts of the world wake up every morning wanting to improve their standing in life as well.

In a recent Q&A with Wes Gray I said I view diversification as a willingness to admit that you have no idea what’s going to happen in the future. I’m sure investors who stick exclusively with U.S. stocks will probably do just fine in the future. But why take the risk?

Further Reading:

How Much International Diversification is Necessary?

Global Diversification: Accepting Good Enough to Avoid Terrible

How Diversification Smooths Investment Cycles

Here’s what I’ve been reading this week:

- Never invest in something you cannot understand (Prag Cap)

- Parenthood is indescribable (Kottke)

- Life lessons from Byron Wein (Wall Street Week)

- We’re all products of our environment (Bason)

- 10 reasons you’re not rich yet (Money)

- Neuroscience trumps investing expertise in gathering AUM (Advisor Perspectives)

- 3 business lessons from JD Power (Reformed Broker)

- All strategies “blow up” (GestaltU)

- Why budgets don’t work (Sandi Martin)

- The hierarchy of investor needs (Motley Fool)

- How companies really get valued (Marc Andreessen)

- Michael Kitces: “I live below my means to create that environment of financial flexibility.” (Bloomberg)

- Why the sunk cost fallacy keeps you wrong (Mullooly)

Patriotism is a lofty idea but in investing home bias is not the most rational stance. I live in Hungary (a small conutry) so it is natural for me to invest globally.

I’m curious, if you had to guess, how much does the typical investor from Hungary have in US stocks?

I prefer all country indices but a lot of investors and fund managers in Hungary invest 100% in US stocks because most of the hungarian stocks are illiquid and small. http://bse.hu/

By the way there is a hungarian (was born here) investor who is very succesful in the US market too and You know his success: https://en.wikipedia.org/wiki/George_Soros

[…] Is international diversification worth the risk: https://awealthofcommonsense.com/is-international-diversification-worth-the-risk/ […]

You ask: “I’m sure investors who stick exclusively with U.S. stocks will probably do just fine in the future. But why take the risk?”

My answer to this is that since investors who stick exclusively with U.S. stocks will probably do just fine in the future, why take the risk of investing elsewhere? I and many U.S. investors have a deep understanding of the U.S. economy, and I stay abreast of it on a daily basis, which gives us an ability to make investments on a rational basis. Does anyone know (just as examples) how the Chinese government will next rig its stock market with massive market interventions, which Asian companies have decided to use “fake” financial audits, which companies Russia will decide to confiscate, or whether Tsipras and the Greeks will come to their senses and avoid a Grexit, and what will happen to currency values (and hence foreign stock values in dollars) if a Grexit happens? The answer is that nobody, even those who live in those countries, have much visibility into what might happen next due to the capriciousness of these governments and lack of business regulations. In comparison, the transparency and rule of law in the U.S. means that investing here has substantially less volatility and risk, and as you note, U.S. companies still get you international exposure with 40% of sales from overseas. My sticking with U.S. stocks has nothing to do with patriotism as Gregory implies, it is simply good and solid risk-averse investing!

That’s fair but you also have to consider the role of luck and the possibility that US markets don’t have the same types of returns going forward.

https://awealthofcommonsense.com/the-role-of-luck-in-your-portfolio/

See page 37 of this report:

https://publications.credit-suisse.com/tasks/render/file/?fileID=0E0A3525-EA60-2750-71CE20B5D14A7818

The US has gone from 15% of global stock market cap to 50%. What if that reverses in the future? I don’t know if it will but it’s a possibility. I still have the bulk of my stocks in US shares, but I think this is something to consider.

The US went from 15% to 50% of market cap over 114 years. I have a long time horizon, but that strikes me as a bit too long for the average investor. I am also reminded of three of Warren Buffett’s quotes:

“It’s never paid to bet against America.”

“Diversification is a protection against ignorance. It makes very little sense for those who know what they’re doing.”

“As Mae West said, ‘Too much of a good thing can be wonderful’.”

[…] Is international diversification worth the risk? (awealthofcommonsense) […]

The sector breakdown of the EAFE and the S&P is interesting; thanks.

In the U.S. at least, the two most knowledge-intensive sectors would be Technology and Health Care (e.g. pharma, biotech, medical equipment, etc.). Tech and Health Care comprise 34% of the S&P, but only 17% of the EAFE.

This substantial difference in sector weighting doesn’t necessarily mean that the S&P will outperform the EAFE in local currency terms, as value tends to outperform growth in the long term.

But for those who want growth exposure, the EAFE is way underweight technology with a pitiful 5.34%, while giant lumbering european banks produce a fat 22.46% weighting in financials.

Good point. That’s pretty much the underperformance over the last 5 years in a nutshell.

[…] Is International Diversification Worth The Risk? by A Wealth of Common Sense […]

[…] The edited excerpts above, and those below, are from an article* by Ben Carlson (awealthofcommonsense.com) originally entitled Is International Diversification Worth The Risk? which can be read in its entirety HERE. […]

[…] Wealth of Common Sense wondered if international diversification is worth the risk. Here’s Ben’s take: “Global diversification allows intelligent investors to […]