Bloomberg estimates retail demand for the SpaceX IPO was in the neighborhood of $70 billion.

That’s roughly 30% of the $250 billion total, higher than the typical 5-10% reserved for retail investors.

Retail investors are no longer the mom-and-pops of the past, openly mocked by the pros.

The growth of retail trading this decade is a massive sea change in the financial markets. No one could have possibly predicted that a pandemic would spark the largest retail trading boom in history.

Citadel Securities has some data on this trend:

Nine of the ten largest retail trading days ever observed on our platform have occurred in just the last month, including seven during the first half of June alone. Friday (June 12) marked the largest single day of retail net buying in our dataset, surpassing the previous record by 50%.

Rather than subsiding after the pandemic — as many predicted at the time — retail trading is only growing:

The same trend is showing up in the options market too:

Citadel Securities notes the average daily option volume for retail traders broke record highs in May, up 20% from a year earlier. There was another new volume record shattered in the first week of June followed by yet another the very next week.

I sense a theme here.

Some of this is speculative activity of course. No one trades zero day options for long-term investment purposes. But retail investors are beginning to exhibit institutional-like behavior.

Semiconductor stocks are all the rage right now and for good reason. The returns have been otherworldly.

In the past 12 months alone, SanDisk is up more than 4,000%. Western Digital and Micron are both up nearly 1,000%.

Retail investors have taken notice and poured money into this space:

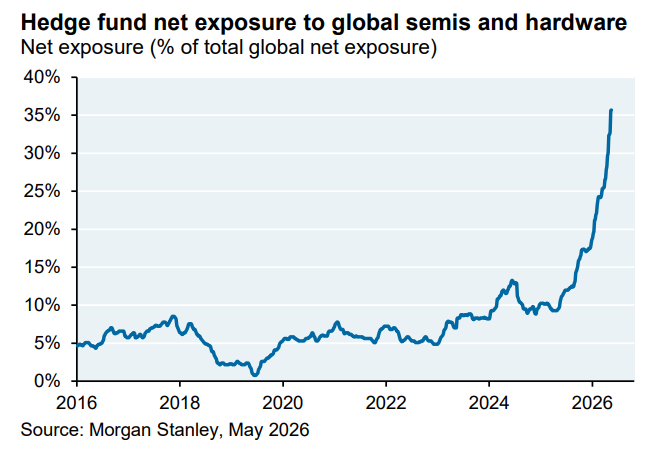

But so have the hedge funds (via Michael Cembalest):

These are the companies now driving index performance in the S&P 500 and Nasdaq 100. It’s not just meme stocks anymore.

Some pundits would have you believe the markets have turned into a speculative orgy of degenerate gamblers. Sure, there is some of that going on as one would expect during boom times such as this.

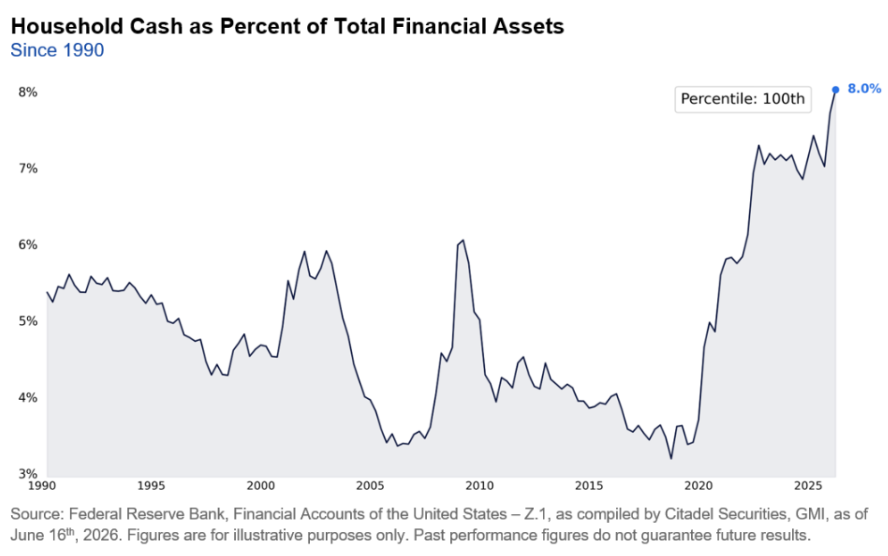

But this simply isn’t the case in all corners of the market. In fact, Citadel Securities also has data that shows cash as a percentage of financial asset is now at its highest level since 1990:

And it’s only growing.

How could cash balances be such a large percentage of assets in what many are calling a speculative mania?

For one, there are many different investor types out there these days.

Here are three other reasons cash holdings have been rapidly rising during a bull market:

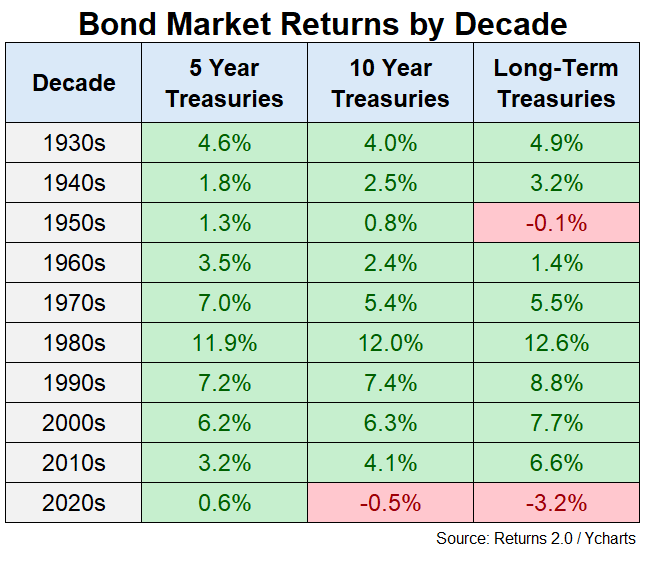

1. The bond bear market. The 2020s (so far) are the worst decade ever for bond investors:

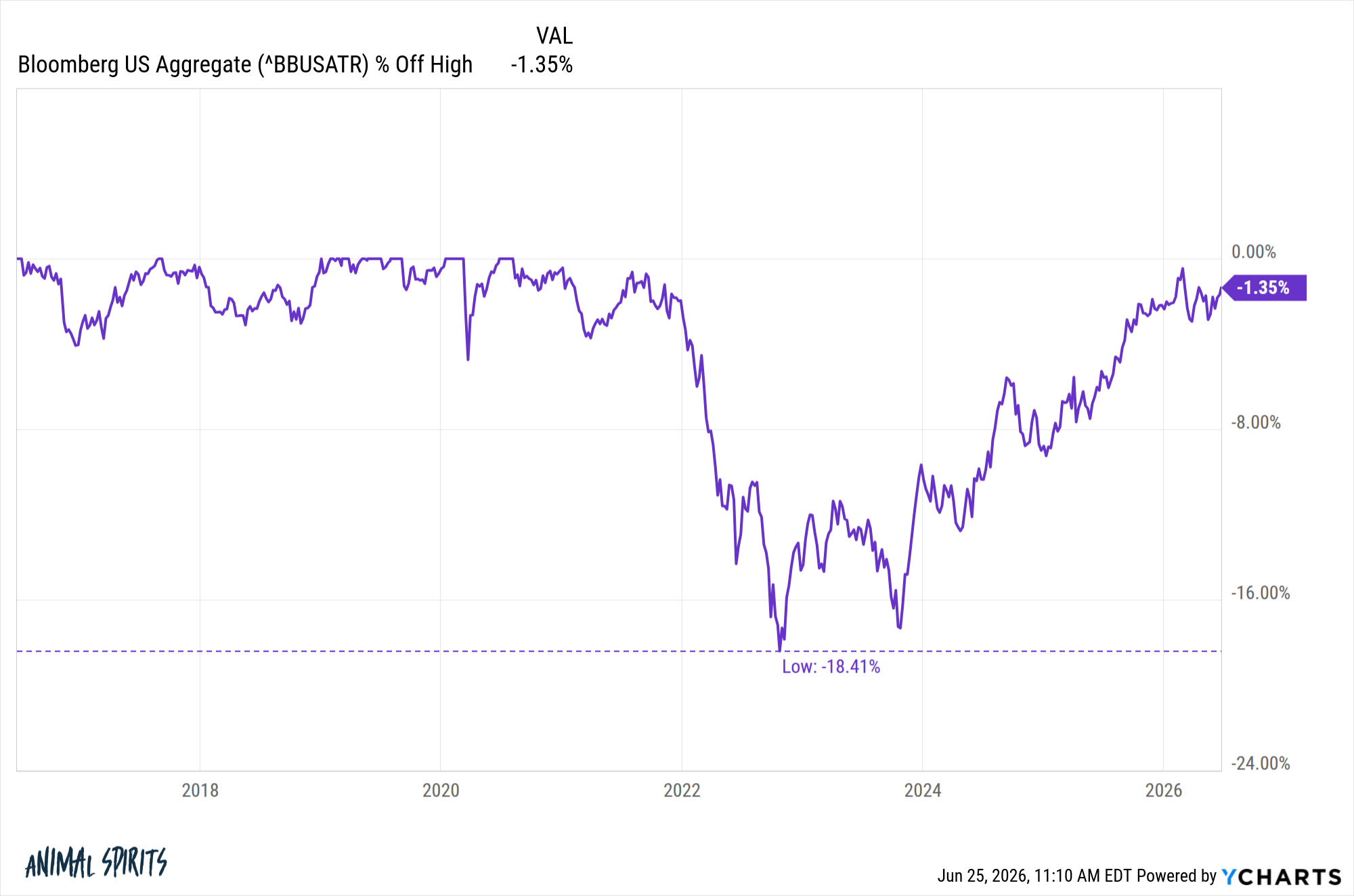

The Agg had by far its worst drawdown in history during the bond bear market that began in 2022:

Many investors decided to own cash in lieu of bonds for fixed income exposure after a rising rate, higher inflation environment crushed high quality bonds.

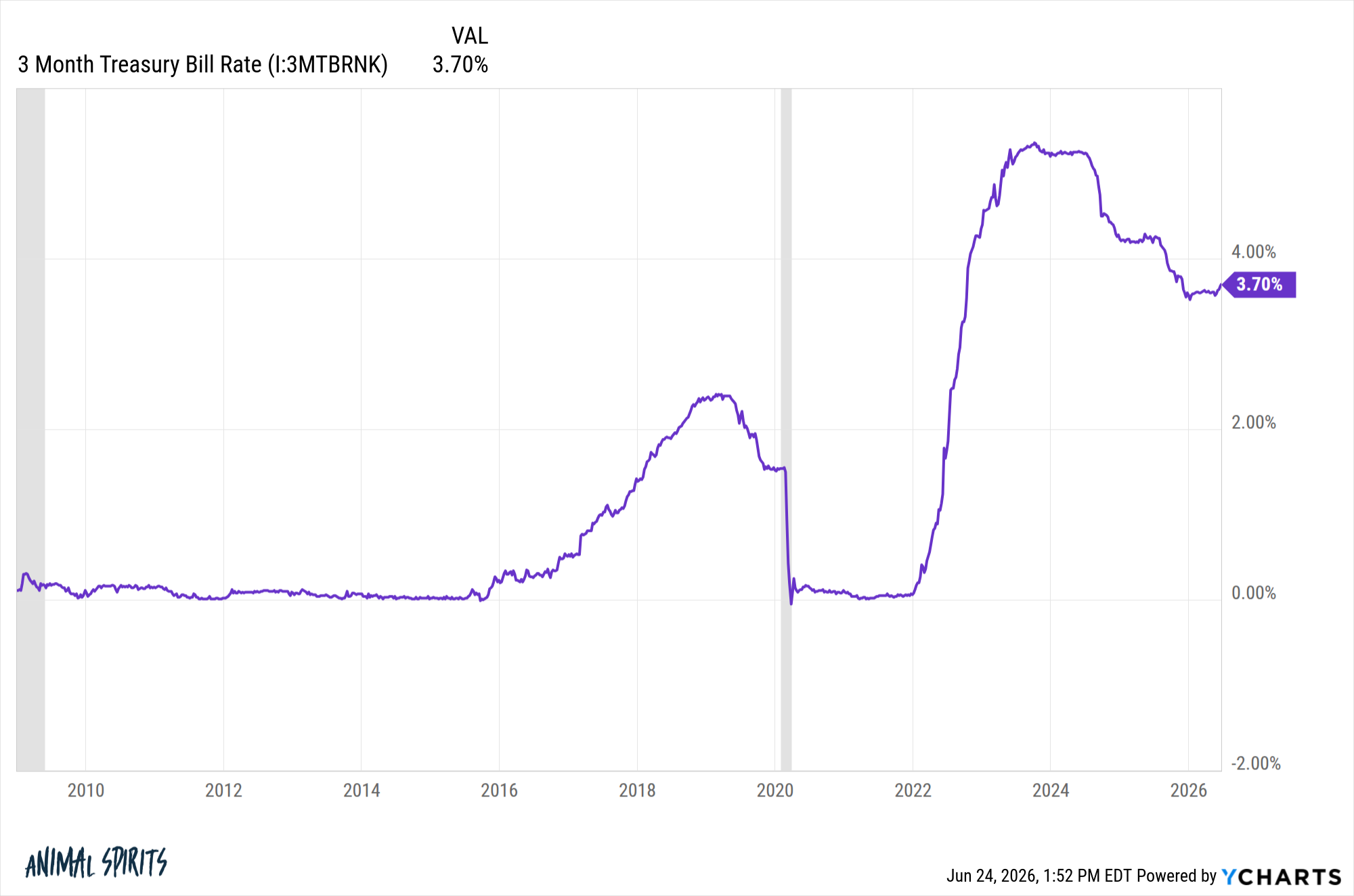

2. Cash finally has yield. It also helps that cash has much higher rates following well over a decade of yields on the floor:

Earning 3-4% on cash equivalents isn’t enough to move to the beach and live off the interest in a world of 3-4% inflation. But it’s much better than the 0% yields investors were subjected to for much of the post-GFC period.

3. Baby boomers are de-risking for retirement. There are something like 45-50 million baby boomers who are already retired. Another 20-25 million are closing in on their retirement.

Most investors seek more balance in retirement when it comes to risk assets. Many investors hold an allocation to cash as a margin of safety in retirement.

That’s how cash allocations could be moving so much higher in the midst of an AI boom that coincides with a retail trading boom.

Something for everyone when it comes to market narratives these days.

Michael and I talked about cash allocations, speculation and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

Is This the Worst Decade Ever For Bonds?

Now here’s what I’ve been reading lately:

- New World Order (Downtown Josh Brown)

- Who won’t be replaced by the machines (TKer)

- The adults don’t exist (High Agency)

- Why you need an investment philosophy (Morningstar)

- Kicking the can on Social Security (Abnormal Returns)

Books:

Risk & Reward podcast tour: