The way I see it there have been two big shifts in the past 20-30 years in the wealth management space.

One, financial advisors went from selling products to offering holistic, goals-based financial advice.

And two, most advisors gave up on the idea of seeking alpha as a way to provide value to clients.

This isn’t the entire industry. There are still products being sold. People are still looking to outperform the market.

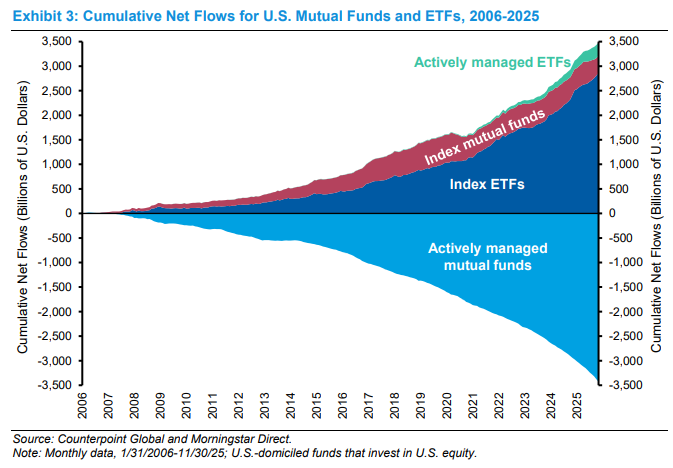

But for all intents and purposes, indexing won over active management (via Morgan Stanley):

So what’s next?

I’m sure AI will have something to say in the coming decades but the biggest trend I’ve witnessed firsthand in recent years is the desire for tax alpha. Most clients and advisors recognize beating the market is difficult and there is no persistence in outperformance.

If you want to add value it’s much easier to focus on what you can control — things like fees, asset allocation, withdrawal strategies, financial planning and taxes.

Bloomberg recently had a lengthy profile about how tax alpha is all the rage in wealth management.

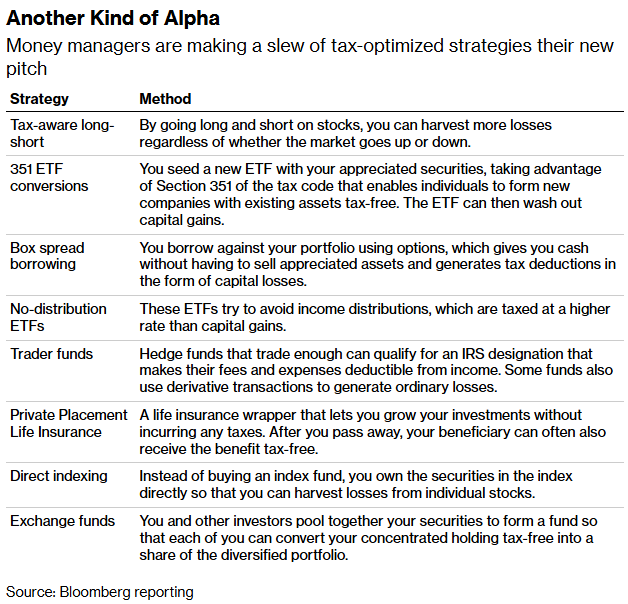

Investors have always cared about tax efficiency but there have never been more options at your disposal when it comes to managing taxable portfolios:

If you’re not in the wealth management space you may not be familiar with many of these strategies.

Some have been around for years. Others are relatively new and have quickly become more popular because of improved technology and lower trading costs.

Speaking from experience, the popularity of these strategies is exploding. We’re having clients come to us in search of these solutions.

Typically, it’s clients who are sitting on large gains from concentrated stock picks, funds they’ve held for the long-term or capital gains from some other transaction (sale of a business, real estate, stock options, etc.).

People are well aware that it’s your net returns — what you take home after tax — that matter most.

Tax loss harvesting through direct or custom indexing has seen the most interest this decade but that’s now expanding into 130/30 funds, 351 exchange funds, exchange funds and the like.

Most investors are looking to create losses to offset gains elsewhere, diversify their portfolio out of concentrated positions and generally defer paying taxes on gains for as long as possible to avoid interrupting the compounding process.

I am of the opinion that the tax tail should not always wag the portfolio dog. Most of the time you shouldn’t be making investment decisions based exclusively on tax efficiency. But it’s actually kind of shocking how many tax-efficient strategies exist these days that add value on top of what you’re already trying to do with your client portfolios.

The solutions are getting better and better.

We use many of these tools at Ritholtz Wealth. One of our partners is O’Shaughnessy Asset Management. We’ve been using their Canvas custom indexing platform since day one and the tools have been an enormous value-add to the financial planning process.

Last week I sat down with Ehren Stanhope from OSAM on Talking Wealth to discuss:

- The difference between direct indexing and custom indexing.

- How long/short funds can help lower your tax bill.

- The trade-offs of complicated vs. simple portfolio solutions.

- How to transition highly appreciated stock into a more diversified portfolio.

- The role advisors play in tax-managed strategies and more.

Watch the whole conversation here:

Or listen to the podcast version here:

Subscribe to our Talking Wealth Newsletter here.

Further Reading:

Why Do Rich People Still Borrow Money?