The Iran war started in late-February.

In a matter of weeks, the S&P 500 was down nearly 10%.1

Those losses have been erased in a hurry as the stock market raced back to new all-time highs in no time.

According to Bespoke Investment Group, this is the first time in the past 100 years that the S&P 500 made new all-time highs in 11 trading days or fewer after falling 5-10%.

The market is supposed to take the stairs up and the elevator down. The past 10 years or so, it’s been the elevator down and the elevator right back up again.

Just look at all of those V-shaped recoveries:

It happened following the mini-bear market in 2018. It happened following the Covid Crash in 2020 which was the fastest run-up to new all-time highs following a 30%+ bear market in history. It happened after Liberation Day and it happened again with the Iran conflict.

The only time we didn’t get a V-shaped recovery was the 2022 inflation spike but even that was more of a run-of-the-mill non-recessionary bear market.

I first wrote about market cycles speeding up back in 2014. This is what the head of fixed income at Vanguard had to say about this phenomenon back then:

One big difference between when I arrived at Vanguard and today is the speed of the markets. In 1981, when a news event occurred, you could sit and contemplate it. If something happened overseas, it might not affect U.S. markets, and if it did, it took a day or so. Now geopolitics is so much more important. Everything is instantaneous. We have to make snap decisions all the time without waiting.

In the past decade and change things have only gotten faster. And it’s not just the stock market.

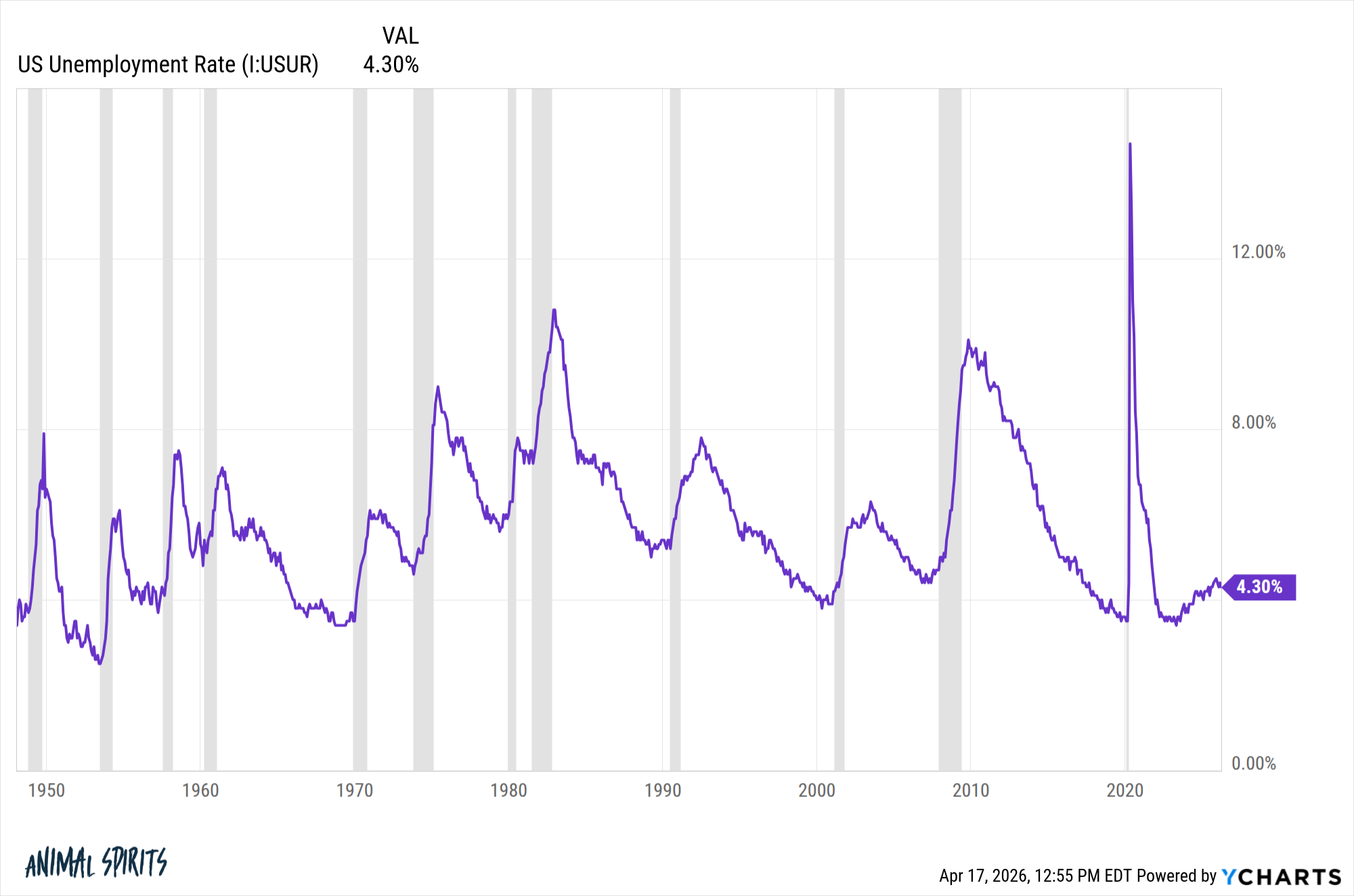

After the brief Covid recession, we had the fastest labor market recovery in history:

We went from 3.5% to almost 15% back to 3.5% in just two years.

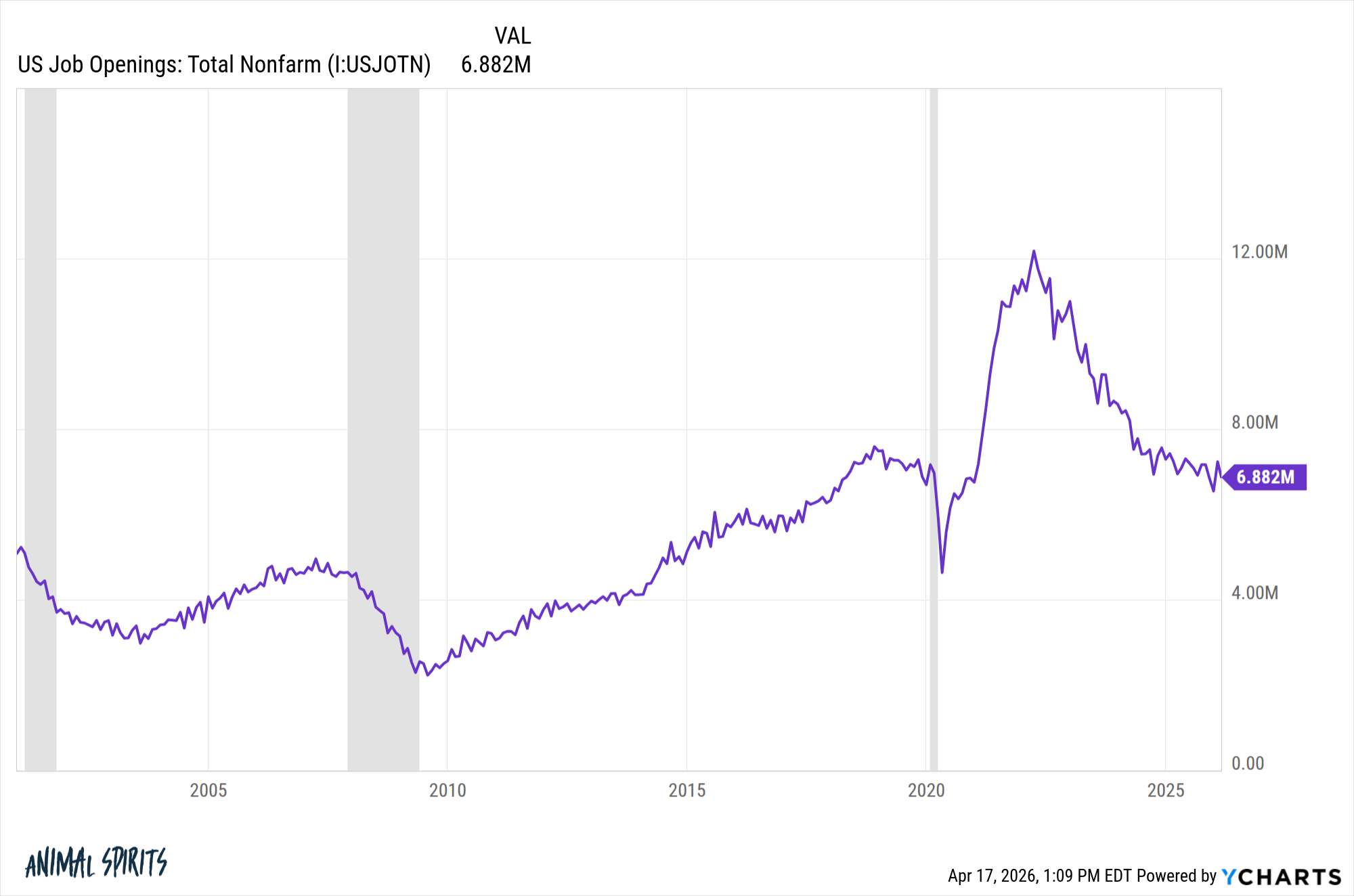

The pandemic also led to one of the strongest job markets we’ve ever seen. Job openings surged from 7 million in the pre-pandemic days to more than 12 million at the height of the labor market craziness:

And now it’s back down again. That’s light speed in the labor market.

Workers went from having the upper hand in 2021 and 2022 to now worrying that AI is going to destroy millions of jobs.

The oil market has been on an even bigger rollercoaster ride in the 2020s.

The price per barrel went from around $60 at the end of 2019 to negative $37 in early 2020 all the way back up to more than $120 following the Russia-Ukraine war. Prices fell immediately after that and got as low as $55/barrel late last year before briefly shooting back above $120 when the Iran war began. Now it’s close to $80.

Phew.

How about interest rates?

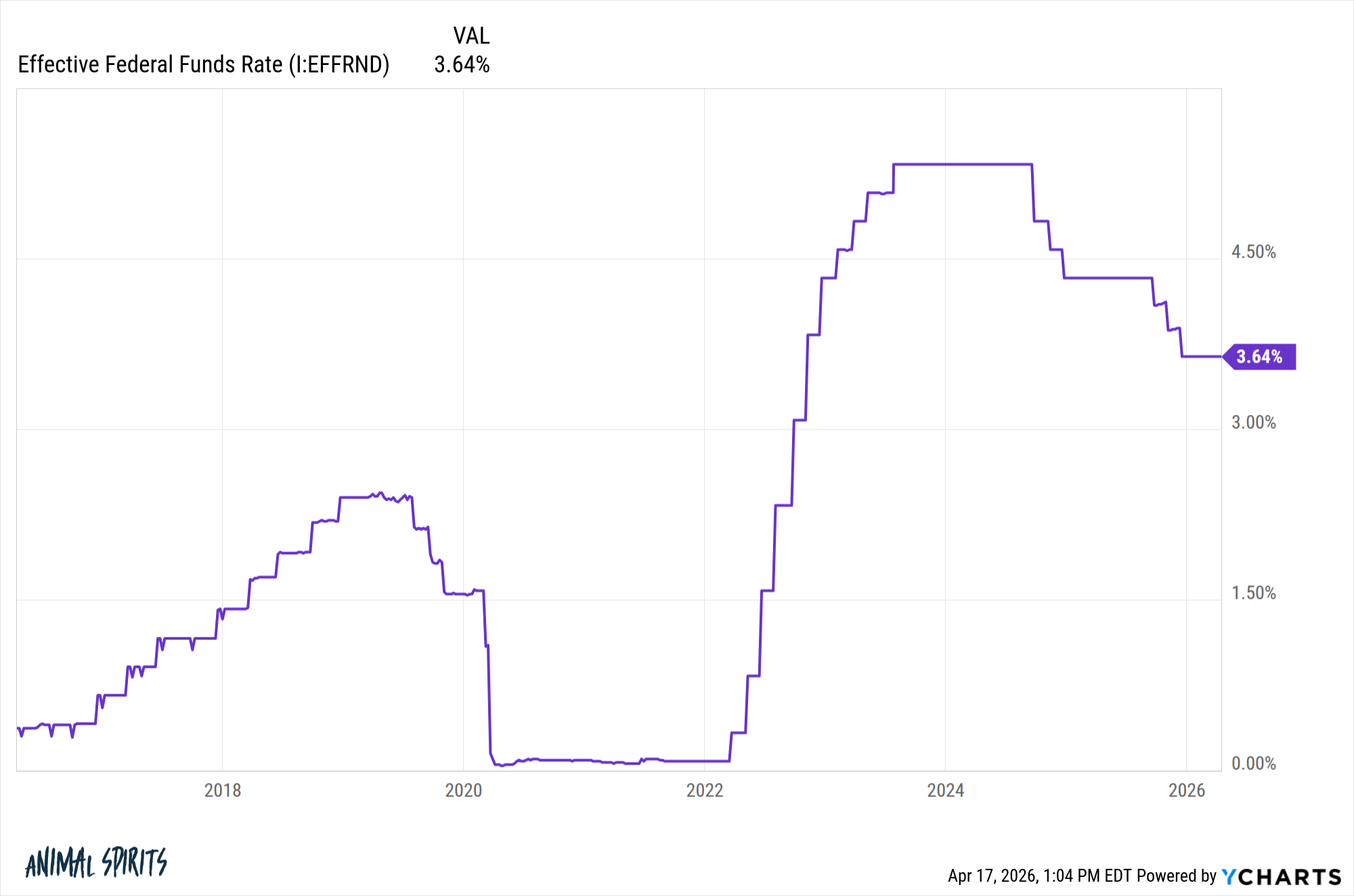

The Fed Funds rate was on the floor for much of the 2010s following the Great Financial Crisis and economic malaise that followed. The Fed tried to bring them back up by the end of the decade but the trade war slowed that and then Covid dropped rates right back to the basement:

Once inflation spiked Jerome Powell and company went on one of the most aggressive hiking sprees in history, taking short-term rates from 0% to more than 5% in a little over a year.

The 30 year mortgage rate went from less than 3% by the end of 2021 to more than 8% by the fall of 2023.

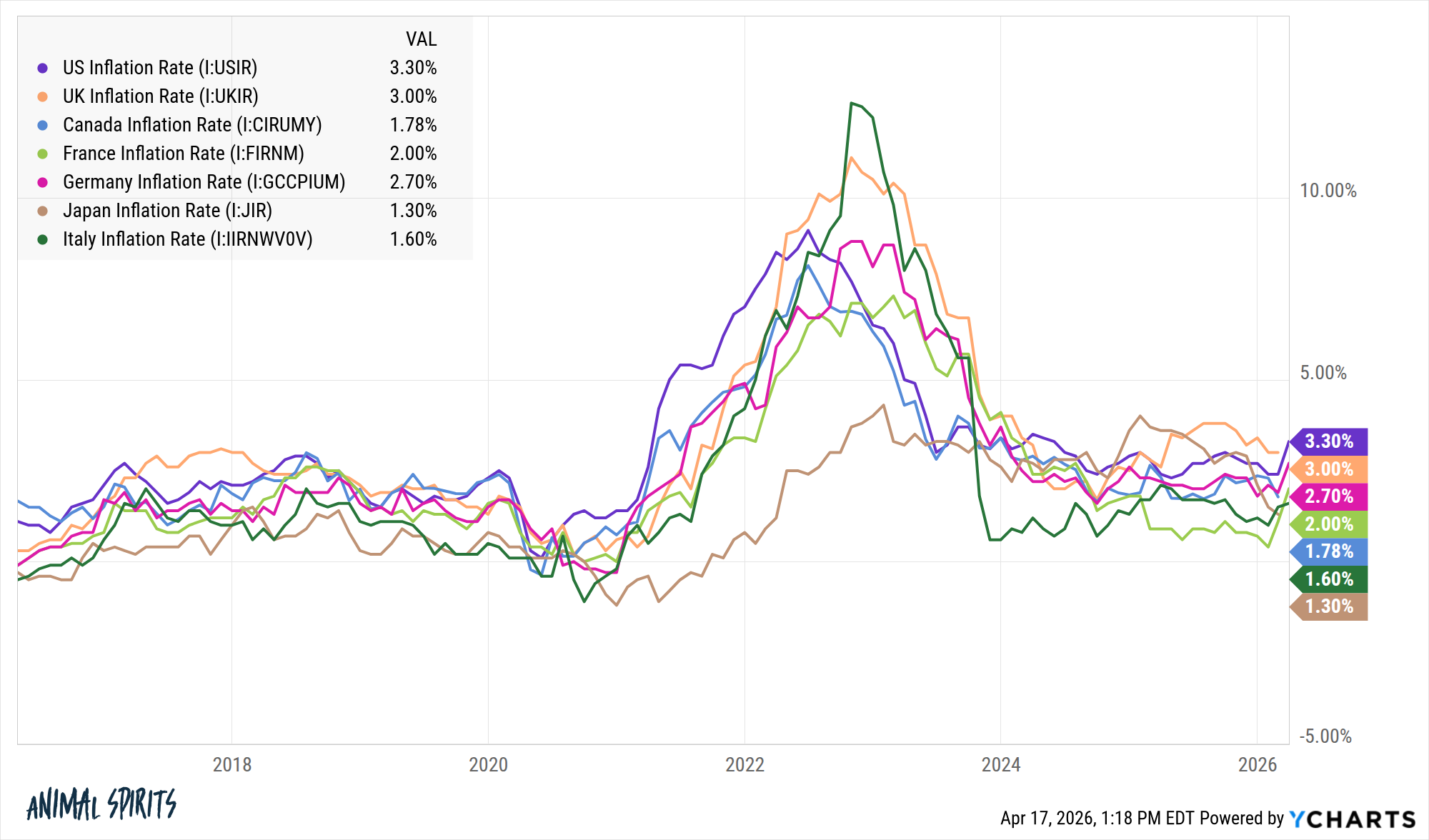

Inflation around the globe went from very low to very high and now around average again all in a matter of a few years:

Of course, one of the biggest reasons for many of these changes, outside of the pandemic, was the stimulus the government provided.

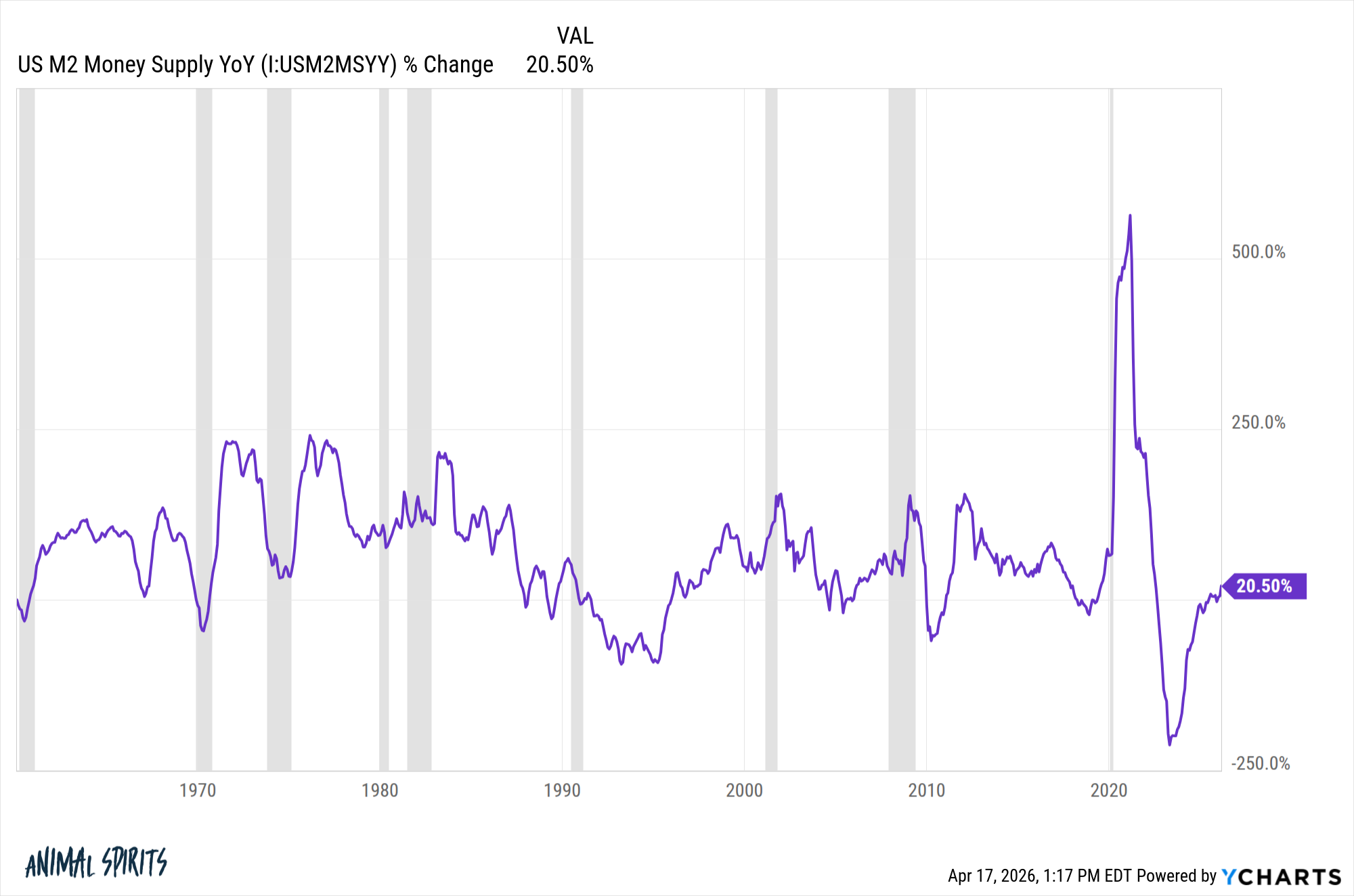

The change in the supply of money supply has also witnessed a massive spike followed by a pullback:

The challenging part of these kinds of moves is that they can be so psychologically difficult to deal with.

One of the reasons consumer sentiment has been so poor these past few years is because prices and mortgage rates moved higher so quickly. People didn’t get a chance to acclimate to the changes over time. Gas going from $3/gallon to $4-5/gallon so quickly is a shock to the system.

You can’t expect to see the stock market always recover in a V-shaped fashion. Eventually there will be a financial crisis or recession that leads to an extended bear market. The labor market won’t always come back this quickly. Mortgage rates won’t have such a wide range in such a short period of time.

It’s certainly possible that most of these moves can be explained by the pandemic and its aftereffects.

But I think we are now living in a world of faster-moving markets because of the information age and government intervention, and it’s here to stay.

What does it all mean?

- Prepared to be wrong more than usual.

- Strong opinions, loosely held.

- The temptation to trade will increase exponentially.

- New risks will emerge.

- Prepare for the possibility of more flash crashes.

Just because markets are moving faster doesn’t mean you have to. Slowing down in a faster world can be your advantage.

Michael and I talked about fast-moving markets and more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

Ignoring the Noise is Impossible

Now here’s what I’ve been reading lately:

- Money tips for people who hate money (The Root of All)

- Round number bias (Behavioral Scientist)

- You have 12 good years (Humans vs. Retirement)

- More millionaires than ever (MSN)

- Chart Kid Matt’s golden rules (Chart Kid Matt)

- Clout is a depreciating asset (Your Brain on Money)

Books:

1It was -9.1% from all-time highs to be exact.