My colleague Nick Maggiulli posed an interesting question on Twitter recently:

A lot of people try to pick winners in the markets. It’s interesting to think about what the losers will be as well.

Nick seems to think it will be private assets or housing.

Returns for both asset classes are slowing already.

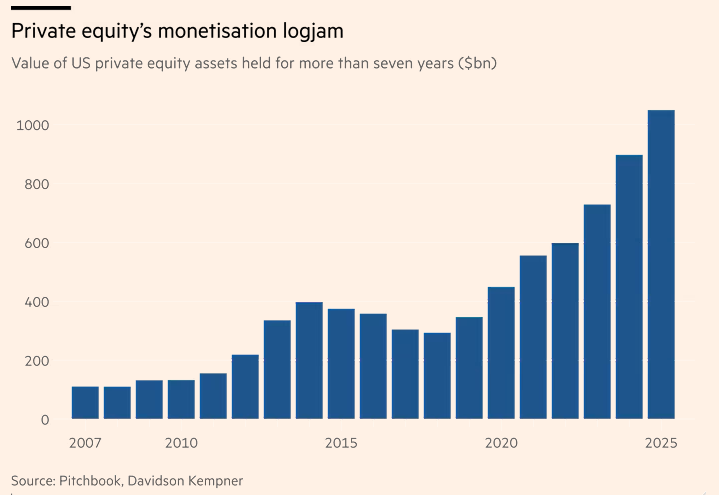

Look at the backlog of PE assets:

There’s a lot more money in private equity. There aren’t many exits happening right now. And there’s still a ton of dry powder waiting to be invested. Returns will likely be lower in this asset class going forward.

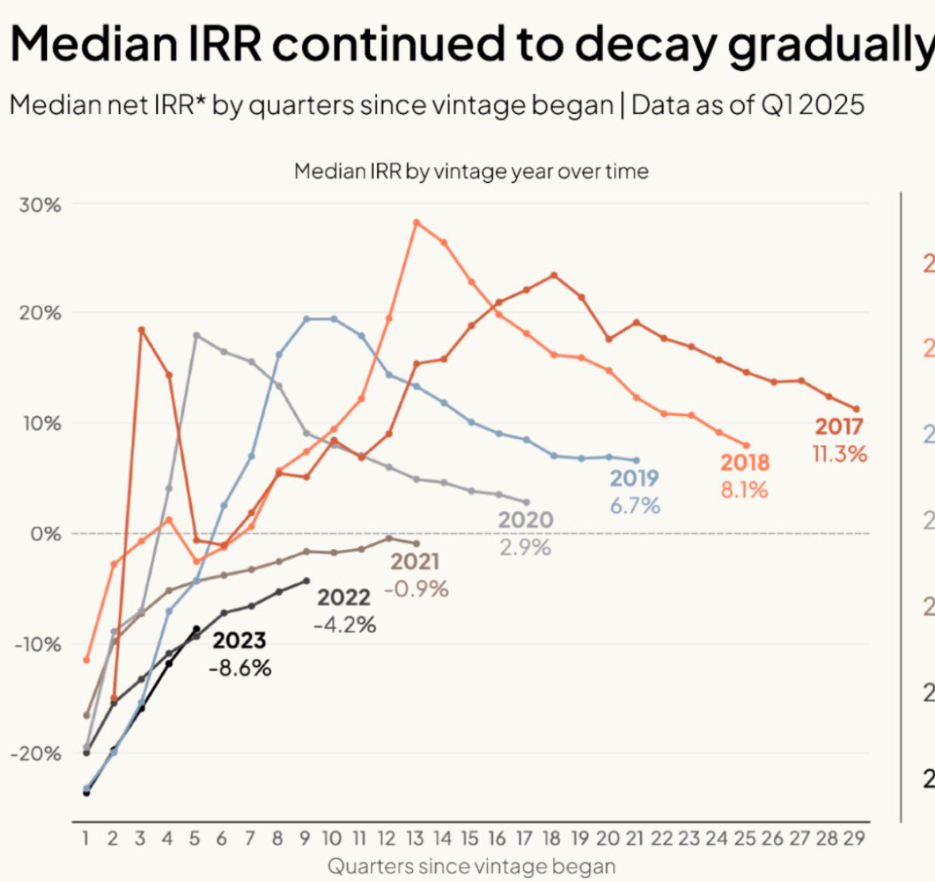

Returns are rolling over in venture capital too (via Rex Salisbury):

The IPO window is essentially closed. Companies are staying private for longer. My guess is most of these private marks are far above what the fair market value would be in public markets too.

These IRRs will likely keep trending lower unless something changes and investors develop a taste for IPOs.

I wrote about private credit redemptions earlier this week. Money flowing out of that space is probably not great for forward returns.

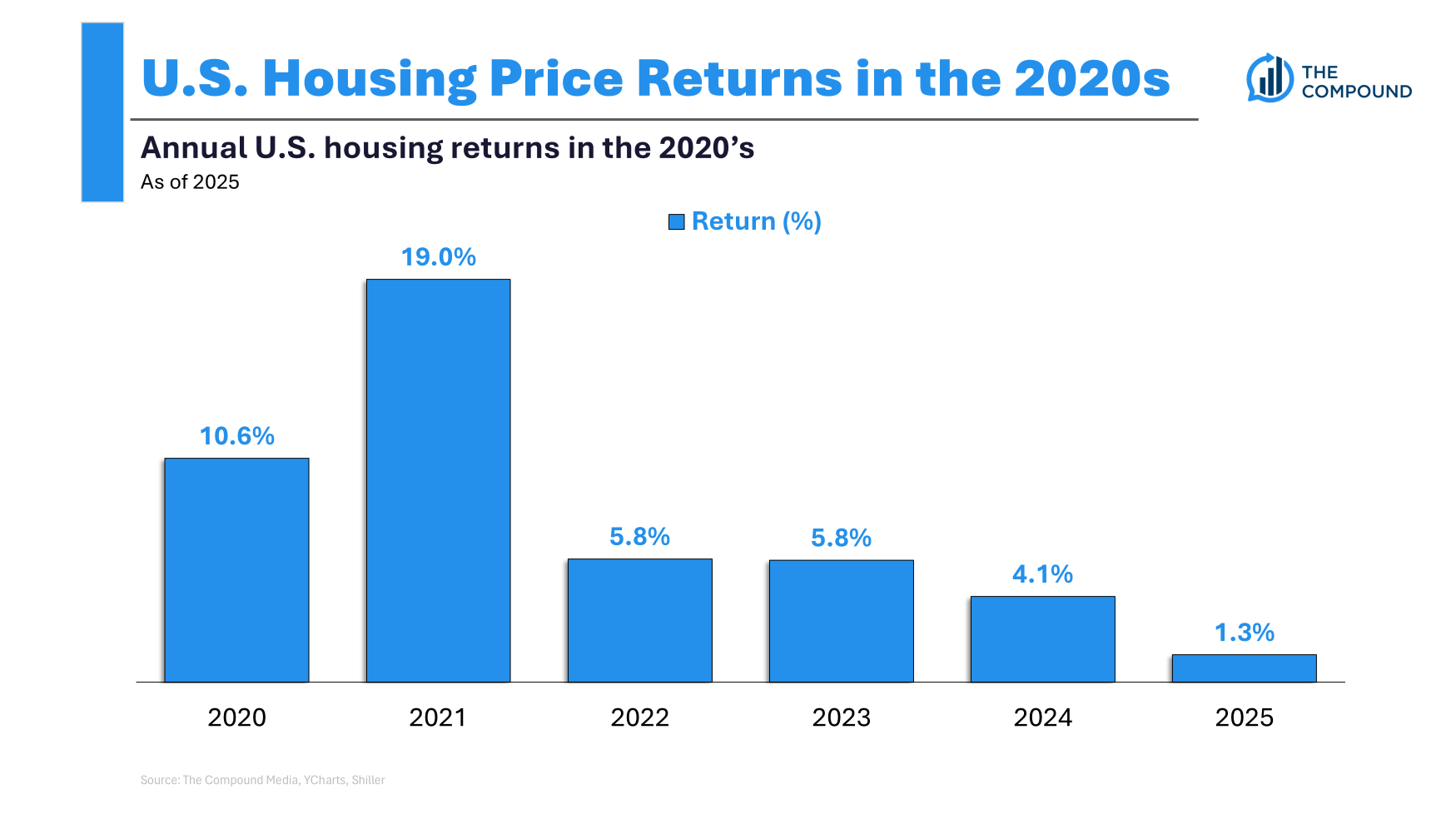

Housing price returns have also fallen off after a blistering start to the 2020s:

Nationwide housing prices rose more than 50% in the first half of the decade. There was no way that trend could continue. It would make sense that housing price returns would stagnate from current levels unless mortgage rates have a meaningful decline.

Even then, housing prices are so much higher it might not matter.

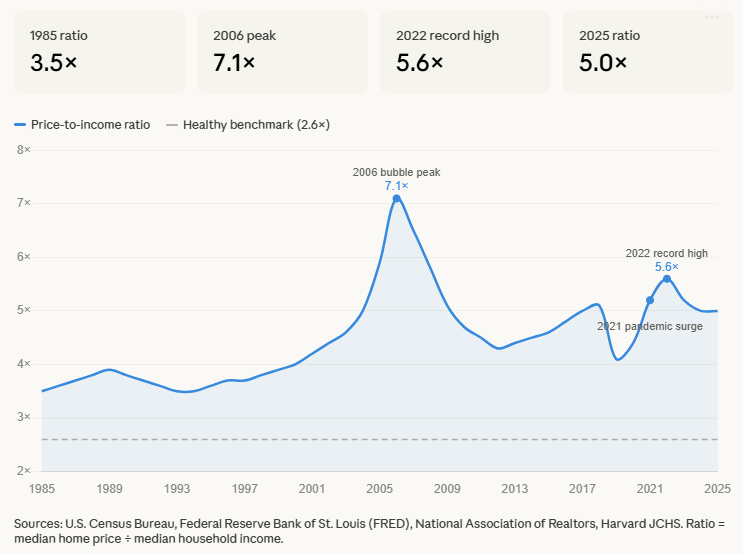

Interestingly enough, the median price-to-income ratio in the U.S. has come in a bit from the peak in 2022:

Wage growth has outpaced housing price growth. Some people will always predict a housing crash but housing prices don’t fall all that often. It would make more sense to me to see prices stagnate and have wages play catch-up than to see prices take a dive.

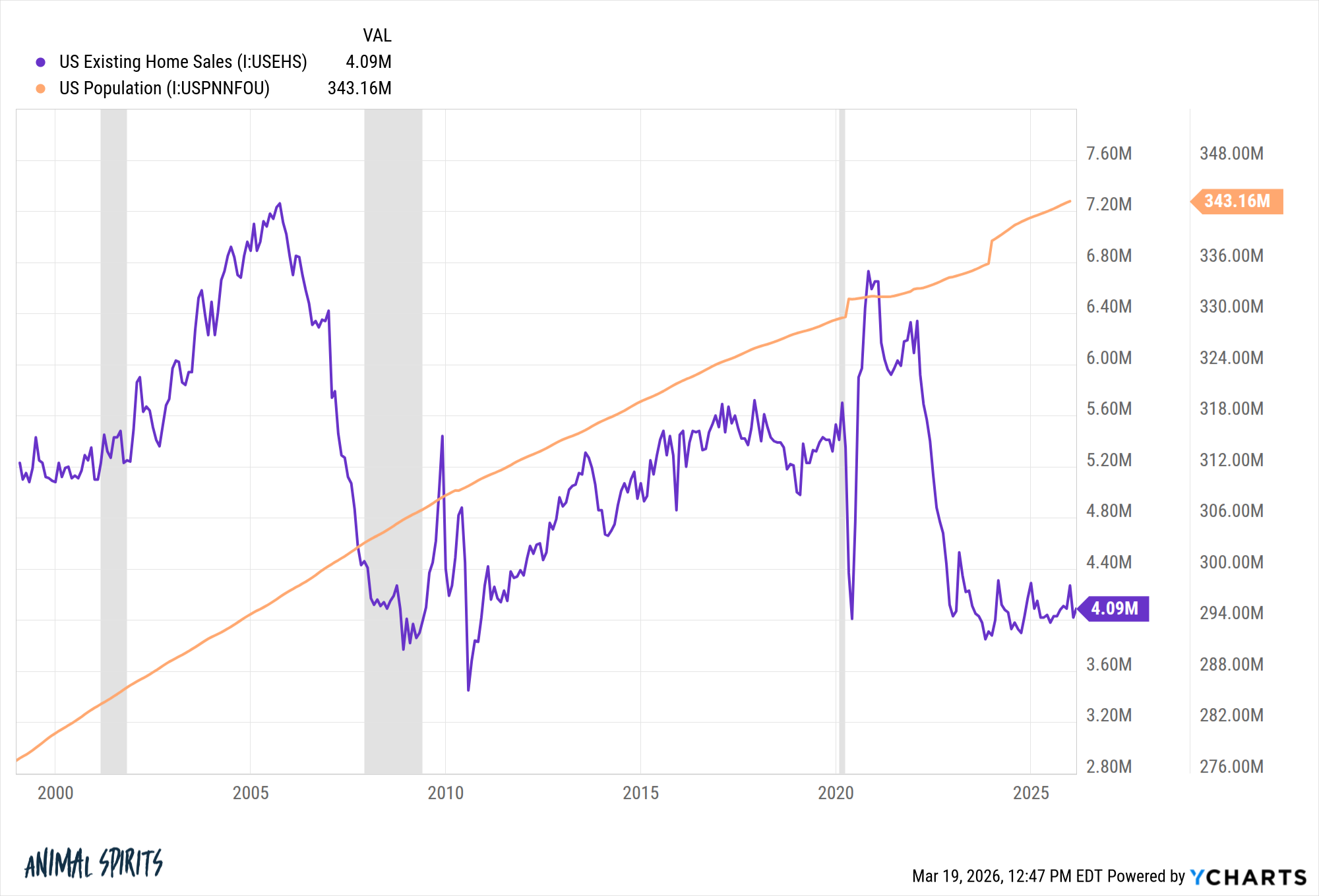

It’s important to note that there are still some houses being sold.

In the past 12 months there have been around 4.1 million existing houses sold in America. That’s lower than the longer-term average of 5.2 million which doesn’t seem that bad until you consider the population in this country has risen from 280 million to 343 million since the start of the century:

Activity is lacking and that’s not helping. We’re also not building enough homes, which also isn’t helping.

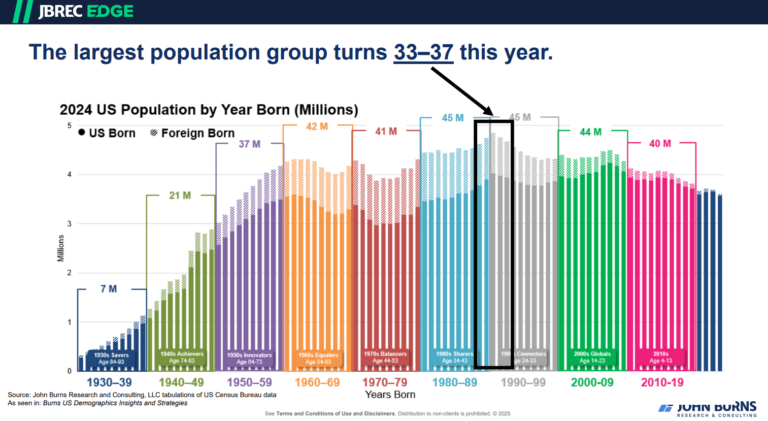

The interesting dynamic here is people in their prime homeownership years are the biggest demographic in the country:

Following the housing bust and the Great Financial Crisis, there was a narrative from the media that young people were never going to buy homes again. That simply didn’t make sense to me.

The big difference between then and now, of course, is that houses were much cheaper in the 2010s. Mortgage rates were much lower.

So maybe demographics will be the force driving better-than-expected returns in housing. We’ll see.

I don’t know if these will be the worst-performing asset classes of the next five years.

How many people thought the U.S. stock market would compound at 14-15% per year for almost 20 years coming out of the Great Financial Crisis? Or that gold would be one of the top performers in the 2020s?

Predicting returns is notoriously difficult.

But I like the idea of going through this process.

Regardless of how it plays out in private markets or housing, it probably makes sense to lower your expectations from here.

Nick hopped on Ask the Compound with us this week to answer this question:

We also discussed questions from our viewers about how buy/borrow/die works, guaranteed returns, 401k vs. brokerage accounts and saving for college in an AI world.

Further Reading:

An Asset-Liability Mismatch