A reader asks:

I live in Miami and my friend’s daughter is looking at colleges, and I saw the tuition for UM is $80,000 a year. If the kids need student loans, they will leave college with $320,000 in student loans. If they want to go to grad school after, the amount of loans will easily exceed $500,000. So they would be 25, over $500,000 in debt, and very likely not finding a job that is close to $100,000+. The question is, how are people thinking about the future economy where 70%+ of the economy is consumer driven, but the consumer is going to be in so much debt that it may seriously affect spending habits? Is there a tipping point for this? Also, I am looking at buying a house, and prices are at all time highs over here. If I’m relying on the next generation to buy my house, but the next generation is so overwhelmed with debt from student loans that they can’t get a mortgage, what happens to home prices? I know there will be the greatest transfer of wealth in the history of ever that will occur, is that supposed to fill in the gap? What are your thoughts?

Young people face a lot of financial challenges that previous generations didn’t have — student loans, high housing costs, healthcare, higher transportation costs, inflation, AI’s impact on the labor market, etc.

The area where I sympathize with young people the most is on the housing front. Through no fault of their own, many young people missed out on generationally low mortgage rates and a historic housing bull market.

Having said that, things aren’t nearly as bad as this reader lays out.

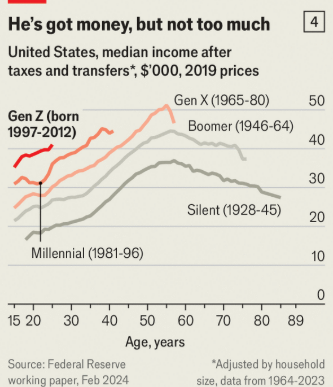

For one thing, Gen Z makes more money than previous generations. The Economist looked at inflation-adjusted wages by demographic at the same age and Gen Z towers above the rest:

The typical Gen Z income is 50% higher than baby boomers at the same age (again adjusted for inflation). It helps that this is the most highly educated generation ever.

But what about student loans?

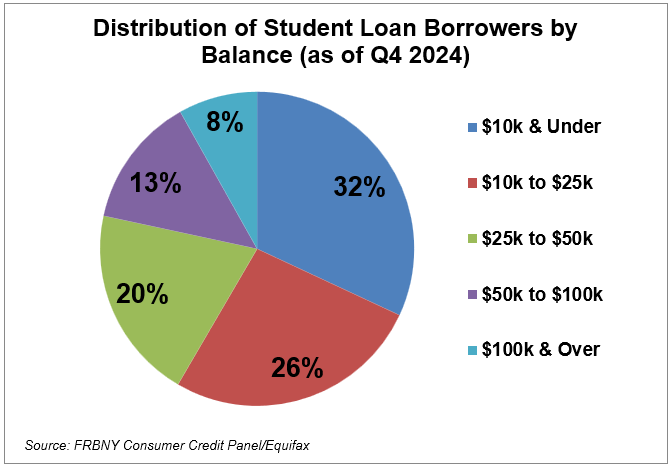

While there are people who have six-figure balances it’s not as widespread as you might think:

Data from the Federal Reserve Bank of New York shows that 58% of borrowers owe $25k or less while nearly 80% borrowed $50k or less. Just 8% are in debt to the tune of $100k or more.

I found a range of different numbers for average student loan debt but it seems to fall somewhere between $30-$40k.1

So why aren’t these student loan balances higher? I’ve seen the crazy high tuition rates too.

The thing you need to know about these numbers is basically no one pays the sticker price.

Ron Lieber has a really great book that examines this in detail called The Price You Pay for College. Some stats from the book:

- The average first-year, full-time student gets a discount of 52.6% off the list price.

- The average grant for public universities is more than $4,100 per year.

- Approximately 89% of students at private colleges receive a need-based or merit-based tuition discount.

Lieber notes, “On average, what families are actually spending hasn’t gone up by completely unreasonable amounts over the past twenty years, even as the list prices have gone to the moon. That’s because the discount rate has gone up steadily over time as well.”

People who do pay full freight are those who attend more selective schools, rich people and international students. The average price actually paid for private colleges is around $24k a year. For in-state public universities, it’s a little more than $15k annually.

That’s more than the $250/semester my dad used to spend on college but it’s not nearly as bad as it looks at face value.

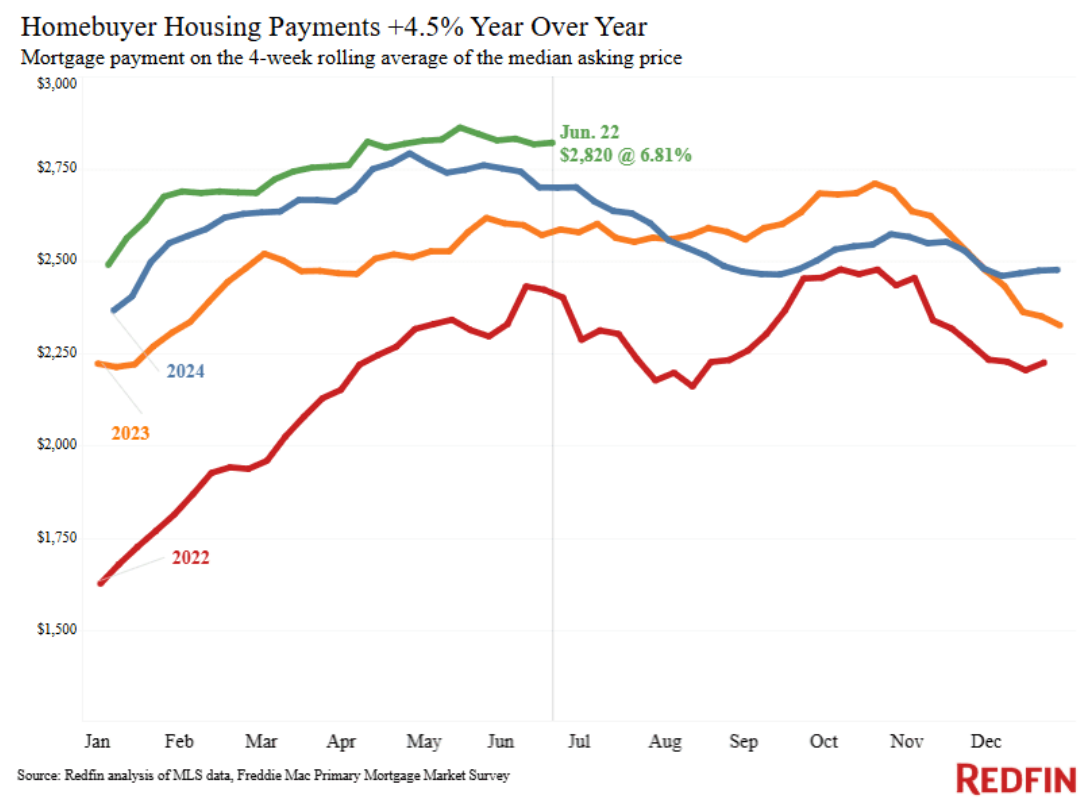

What about housing?

If you take median housing prices and current mortgage rates, the average monthly mortgage payment is at all-time highs:

Even with higher incomes, it remains unaffordable for many young people to buy in today’s environment.

But somehow many young people are sucking it up — or getting help from their parents — and buying.

Look at homeownership rates by demographic at the same ages:

Gen Z is ahead of the curve on income but behind when it comes to buying a home at the same age as boomers, Gen X and millennials. That’s not surprising but it is closer than you’d think.

It wouldn’t surprise me to see this line stagnate for some time as incomes slowly but surely play catch up to monthly mortgage payments.

Young people certainly have challenges in today’s economy. So did every other generation in their formative years.

The baby boomers had sky-high inflation in the 1970s and 15% mortgage rates in the early-1980s. Gen X had the bursting of the dot-com bubble leading into 9/11 and a lost decade in stocks. Millennials entered an awful labor market following the Great Financial Crisis.

Gen Z is dealing with high housing costs and inflation following the pandemic.

I’m not trying to downplay anyone’s struggles of course. There are plenty of young people being left behind or struggling to stay afloat financially.

But I’m a glass-is-half-full kind of guy.

Gen Z will figure it out just like previous generations did.

I discussed this question on this week’s Ask the Compound:

We also covered questions about healthy corrections, a dating budget, balanced portfolios and investing in stocks at all-time highs.

Further Reading:

When Does Housing Become THE Issue?

1For context, I graduated in 2004 with ~$25k in student loans, which is around $42k in current dollars. The big difference is that borrowing rates back then were 2-3%. If I were the finance czar, my plan would be to cancel interest on student loan debt. Simply require people to repay what they owe.