I track all of my savings and investments on Excel.

Guess I’m old school and, yes, kind of a personal finance dork.

I can’t help it.

It’s nothing fancy. Just a collection of the holdings in our various accounts along with some simple calculations — net worth, annual retirement contributions, asset allocation, how much we’re saving each year, etc.

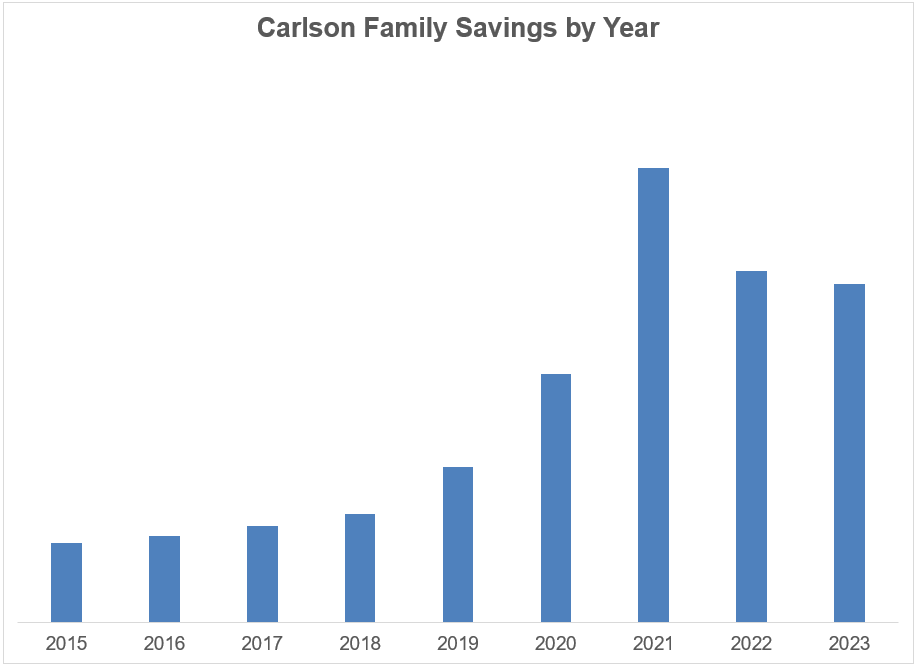

I was looking at my annual savings figures recently and decided to perform some analysis on the changes from year to year:

The numbers don’t matter as much as the trend. A couple of things stood out.

There was a nice breakout starting in 2019 and throughout the pandemic. Not to brag, but I started making more money, and my savings went up commensurately.

Except for 2021, which was an outlier. Our savings took a massive leap that year.

There are a few reasons for that spike.

We weren’t spending as much because of the pandemic. Travel was in a bear market.

If I’m being honest, there was also a bit of FOMO going on. That was the year it felt like everyone was investing in everything — stocks, start-ups, real estate, crypto, private deals, etc. I got caught up in that and put a lot of money to work.

The younger version of me would have been mighty proud of that all-time high in savings. Looking back now, it feels like more of a mistake than an accomplishment.

Don’t get me wrong, saving and investing is still a priority. But it’s not the only priority in our financial plan.

For as long as I can remember, I’ve been a saver through some combination of my personality and upbringing. I’m still a saver, but I now have a more balanced attitude when it comes to money.

I don’t want to delay all gratification until I’m in my 60s or 70s. These past few years, I’ve been getting regular reminders that the future is promised to no one.

I’m no longer impressed or driven by specific goalposts in my portfolio.

I prefer to save a reasonable amount of money and enjoy the rest.

I’m still maxing out my retirement accounts, saving for the kids in their 529 plans, keeping enough liquid reserves for unexpected expenses and putting money into my taxable brokerage accounts.

But I no longer feel it’s necessary to go over and above when it comes to saving. I want to enjoy some of my money now while I can.

That’s the biggest reason our savings fell off a little in 2022 and 2023. We took a bunch of trips. We did some minor renovations to the house that added hangout spaces. We bought a boat. We own a lake house.1

I could add up all those expenses and slap a forward return on them to see how much compounding I’m missing out on.

But so freaking what?!

That money in 10, 20 or 30 years won’t make up for the experiences and memories we’re investing in now while our kids are young.

Call this bull market behavior if you’d like. Savings rates tend to go down when financial asset prices go up.

For me this has nothing to do with the markets and everything to do with priorities.

I’m dollar cost averaging my spending while I can enjoy it with loved ones rather than saving it all up for when I’m older.

Michael and I talked about saving, spending, perspective and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

You Probably Need Less Money For Retirement Than You Think

Now here’s what I’ve been reading lately:

- The C word (Humble Dollar)

- Wealth and money are two different things (Darius Foroux)

- Why stocks are the greatest asset class (Of Dollars & Data)

- How to succeed on Substack (A Writer’s Notebook)

- Only a fool gets rich twice (Allocator Mindset)

- The magic of one day (Money with Katie)

- Bowling alone (Ali Montag)

Books:

1At some point I’ll do a more detailed write up about how this was the best investment I’ve ever made.