Inflation and wages are kind of a chicken or egg issue.

Do higher prices cause higher wages or do higher wages cause higher prices?

I suppose it’s probably a little of both.

There is an obvious relationship when you look at the data.

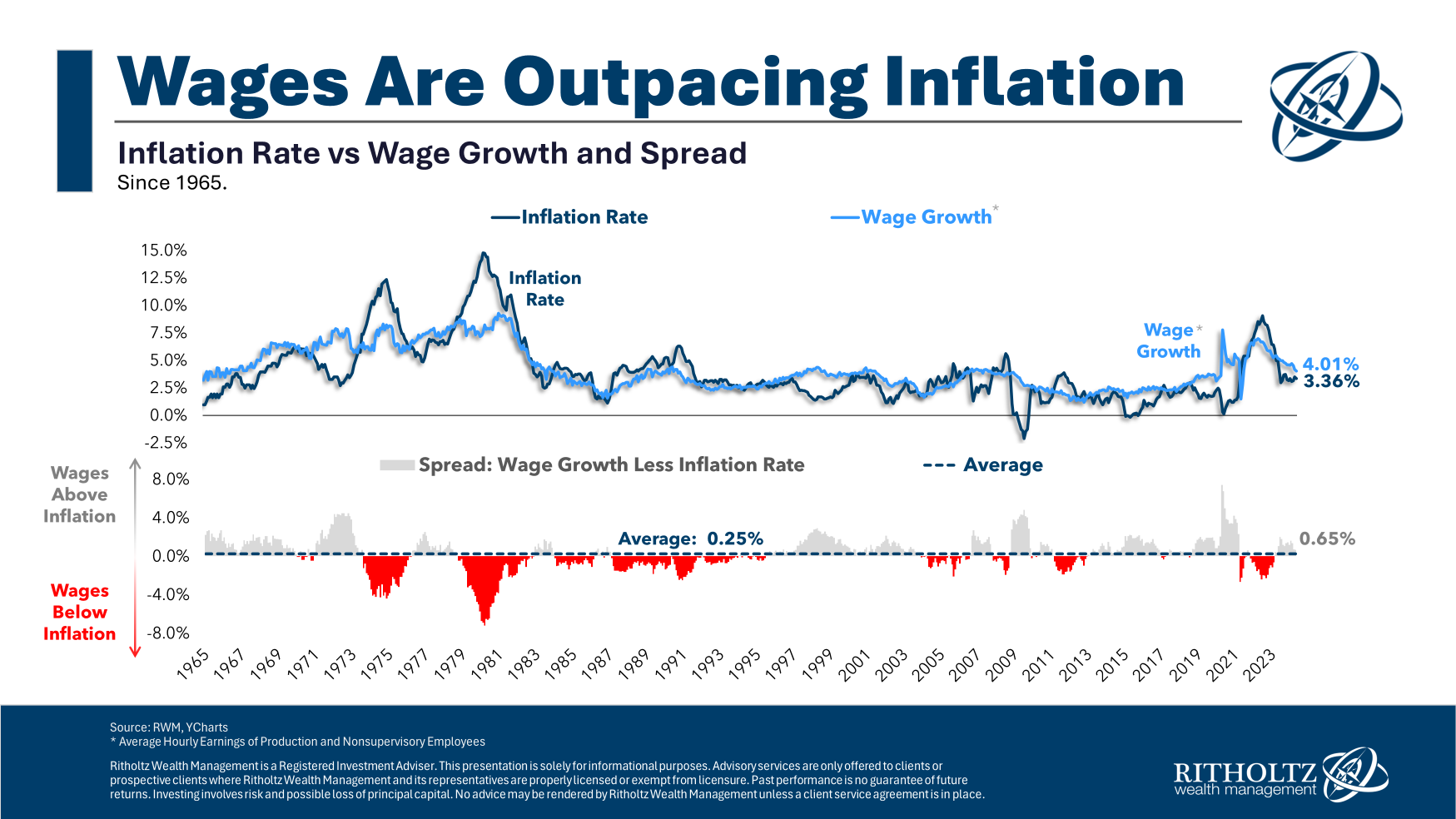

Here’s a look at year-over-year wage growth versus trailing twelve-month inflation going back to 1965:

Wages grow faster than prices most of the time, but not always. Since 1965, wages have been growing above the rate of inflation a little less than 60% of the time.

The worst period by far for wages falling behind prices was the 1970s.

From 1973 to 1976, wage growth was slower than inflation for 36 months straight. Then, from late 1978 through the end of 1982, real wage growth was negative for 50 consecutive months.

And it wasn’t just the length of time but the magnitude of the difference. At the worst point in 1980, inflation was outpacing wage growth by more than 7%.

Surprisingly, there was a long stretch from the mid-1980s through the mid-1990s when wages were growing slower than inflation. From 1984 through the summer of 1995, prices were rising at a faster clip than incomes 88% of the time.

You don’t hear much about that time frame producing economic misery but maybe that’s because at least it was better than the 1970s.

This time around, wage growth was lower than the inflation rate for 21 out of 23 months from 2021 through early 2023.1

We’re currently on a streak of 14 straight months where wages have outpaced inflation.

The good news is wages are growing faster than inflation. The bad news for many households is no one’s life ever matches up exactly with economic averages.

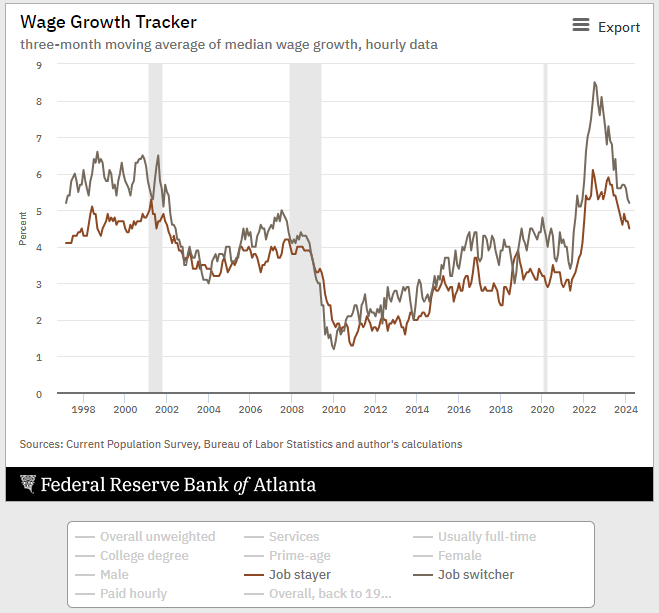

The people who changed jobs during the pandemic saw far higher wage growth than those who stayed with their current employer:

As always, some people are doing better while others are falling behind.

The problem with this relationship is people see higher wages as something they earned while higher prices are a form of theft.

This is one of the big reason economic sentiment has been off these past couple of years. People really despise high inflation.

But you can’t talk about the impact of inflation without talking about the other side of the ledger.

Wages have been rising too and they’re a big reason the economy has remained so resilient.

Further Reading:

The Psychology of Inflation

1It’s also worth noting that huge spike we had in wage growth at the outset of the pandemic is something of a myth. The only reason you see that massive rise (and subsequent fall) in the data is because so many people with lower incomes were laid off (think service professions).