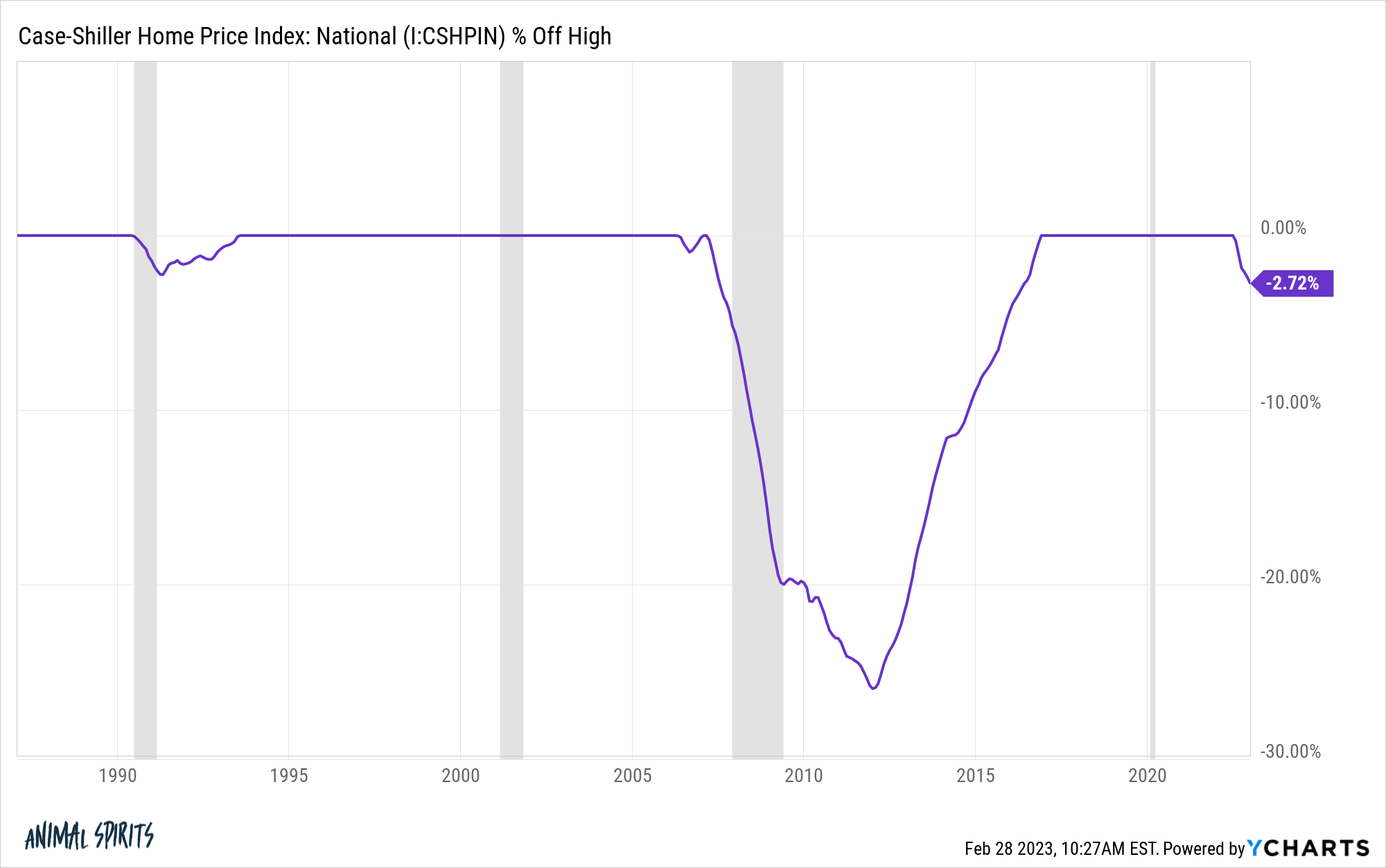

The latest Case-Shiller national home price index data was released this week. Here’s where we stand in terms of the drawdown from peak prices:

This is the third largest national home price drawdown since 1987 but I’m sure lots of people are surprised prices haven’t fallen more what with 7% mortgage rates and unsustainable price gains in recent years.

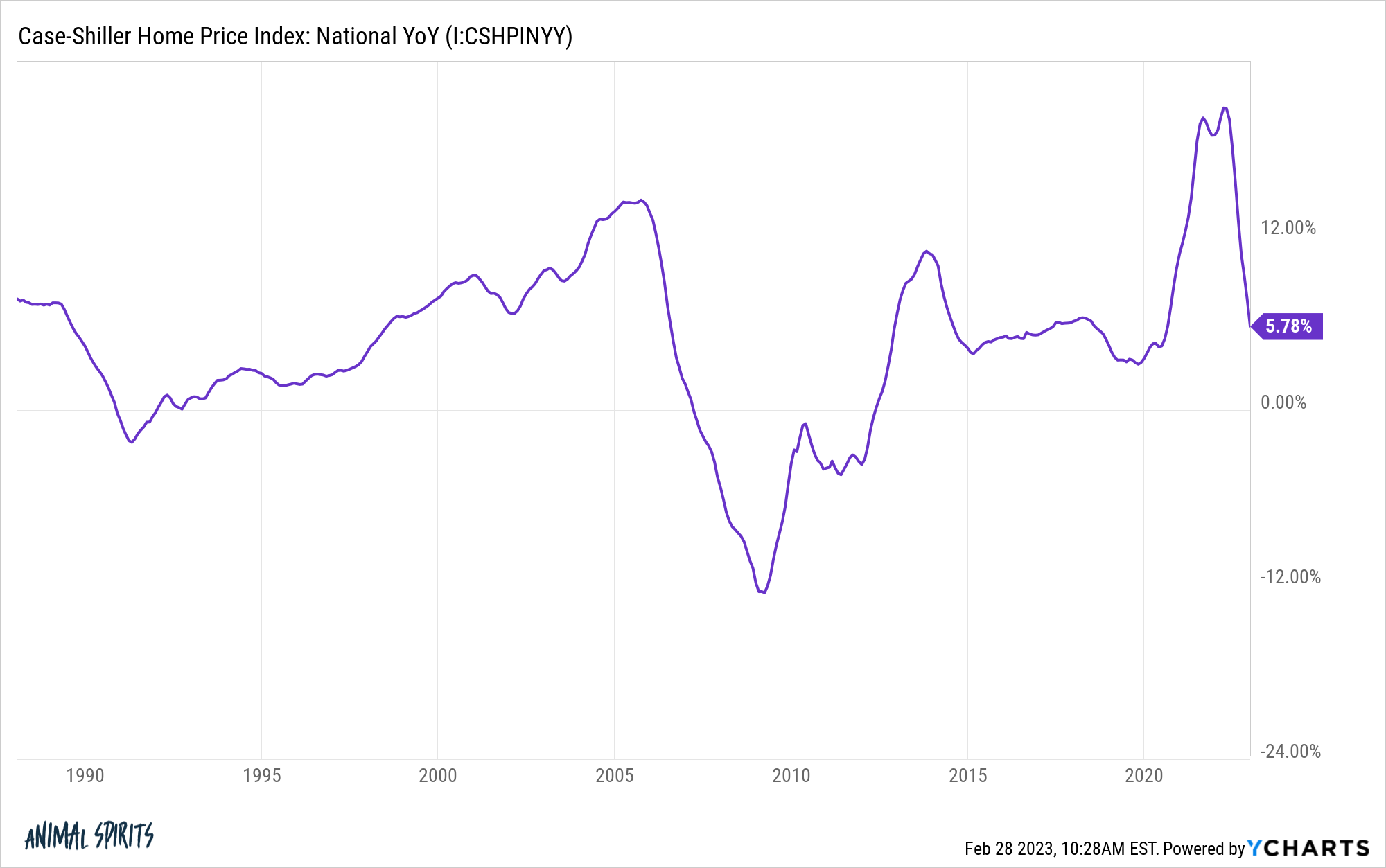

The latest data shows a year-over-year gain of less than 6%:

These kinds of gains are still relatively high but coming down from nosebleed pandemic levels.

To be fair, this data is only through the end of December 2022. Housing prices have probably come down a little more this year.

There are certain areas that are seeing larger price declines — places like San Francisco, Phoenix, Boise, Seattle Austin, etc. But those are also the places that experienced larger gains during the boom years.

There has yet to be a complete collapse in the national housing market despite the worst affordability levels we’ve likely ever seen.

With the caveat that housing prices can and probably will fall more from current levels if mortgage rates stay at 7%, let’s take a look at the data to see why prices have been relatively sticky even in a rising rate environment.

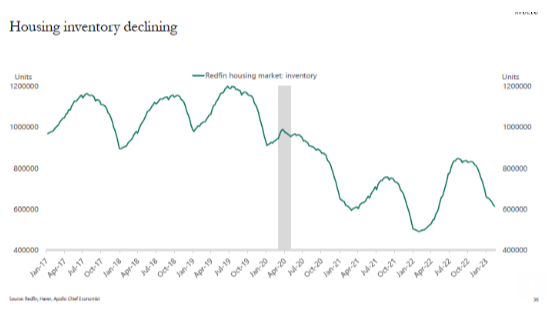

The simplest reason is the rapid rise in mortgage rates has slowed housing activity to a crawl.

Inventory levels rose for a bit but are crashing again so there just aren’t that many houses on the market:

Mortgage purchase application activity, basically the number of loans getting started, has fallen off a cliff to the lowest levels this century:

The seasonally adjusted Mortgage Purchase Application Index falls 5.6% to 138.8.

That's the lowest purchase apps reading of the 21st century.

On a year-over-year basis, total purchase apps are down 43.7%. pic.twitter.com/yYkkrAjqbF

— Lance Lambert (@NewsLambert) March 1, 2023

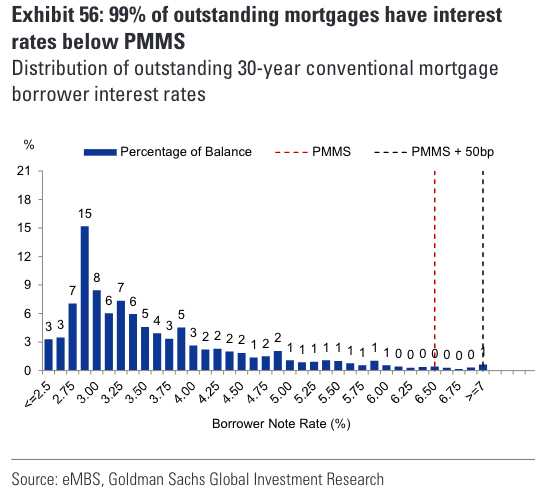

This makes sense when you consider no one wants to sell and no one wants to refinance since the majority of homeowners have mortgage rates that are well below current levels:

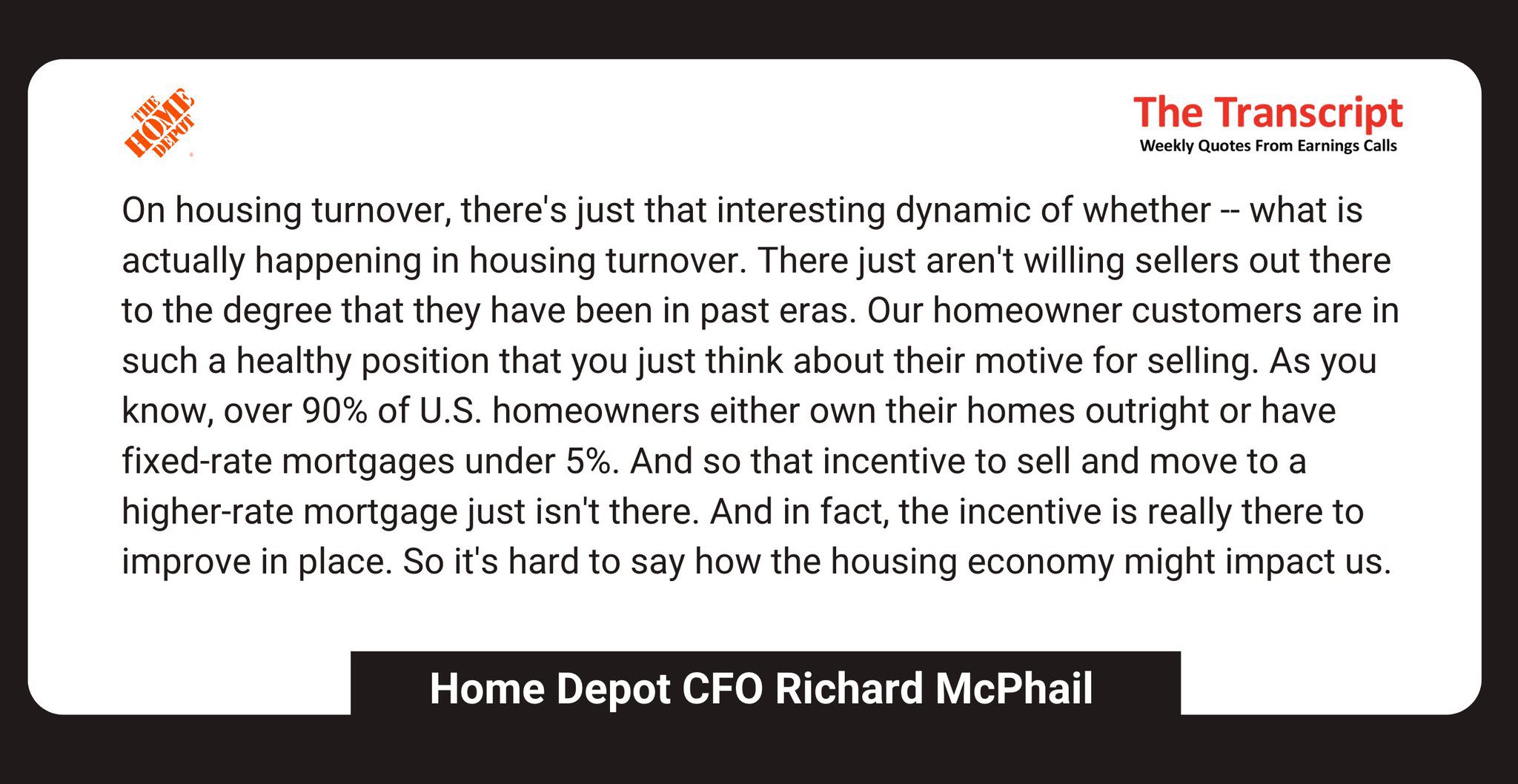

Home Depot’s CFO talked about how this dynamic has been a boon to their business because all of those people with 3% mortgages are opting to renovate rather than move:

It’s hard to see market clearing prices when there isn’t much of a market anymore.

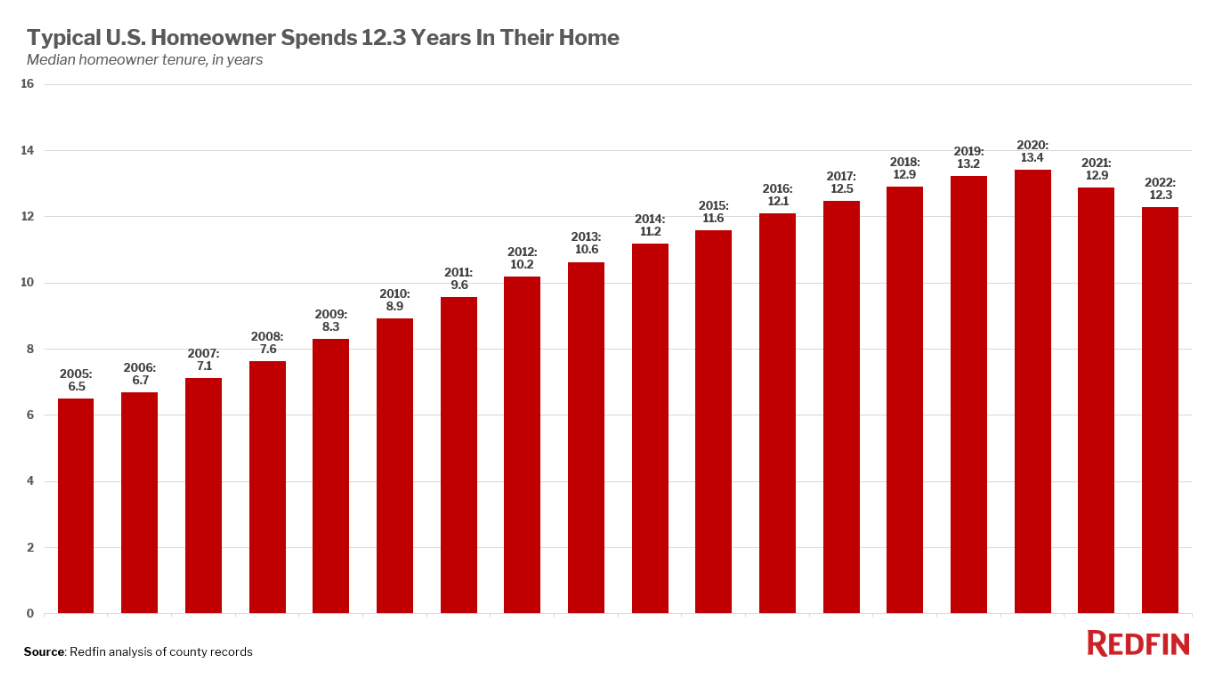

Homeowners were already staying in their homes for longer than they did in the past and it’s likely this trend will continue (via Redfin):

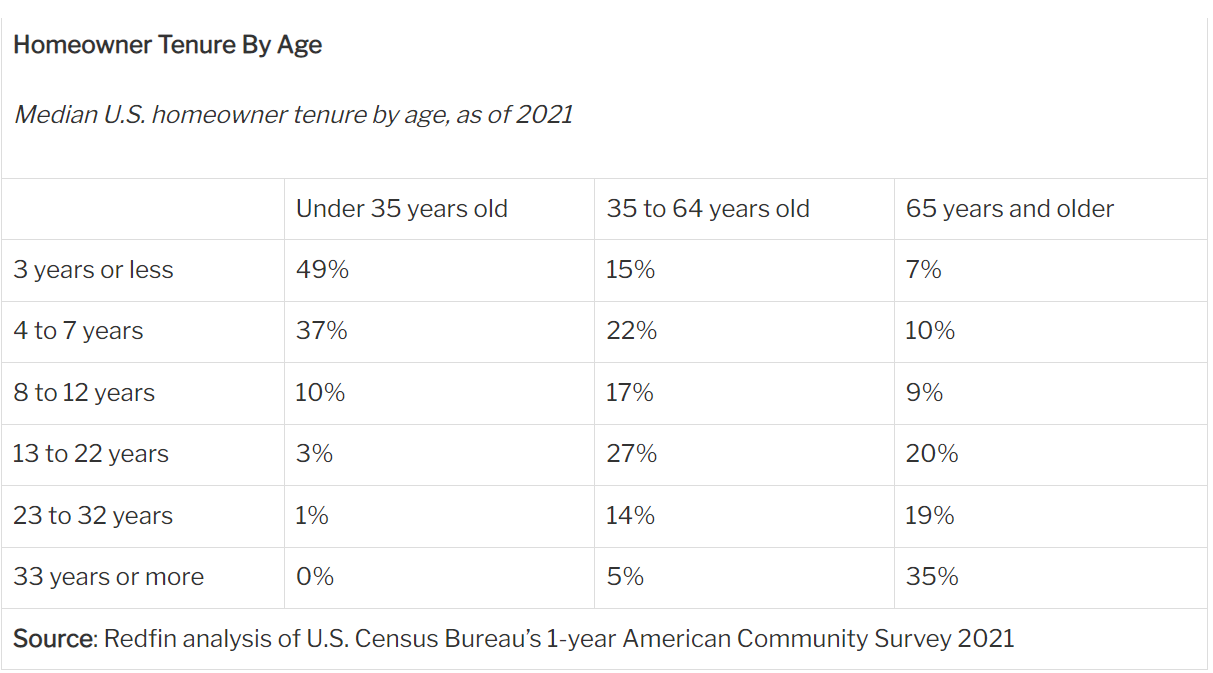

It’s possible younger generations won’t stay in their homes as long as older generations have because of changing tastes but 3% mortgage rates are going to make that decision more difficult:

The good news is demographics will force people’s hands eventually. Baby boomers will downsize, move to Florida or die off.

Millennials will desire larger homes once more of them begin having families.

Housing activity will pick back up at some point.

But if mortgage rates don’t get back down under 5% or 6% it’s difficult to see the impetus for existing homeowners to list their homes for sale in a big way.

The endowment effect is also strong in the housing market. This is the inertia that causes people to place a higher value on something they already own.

That house four blocks over is way overpriced but there’s no way I’m cutting the price on my house.

This behavioral bias could also mean people who are waiting for lower prices are going to have to be patient.

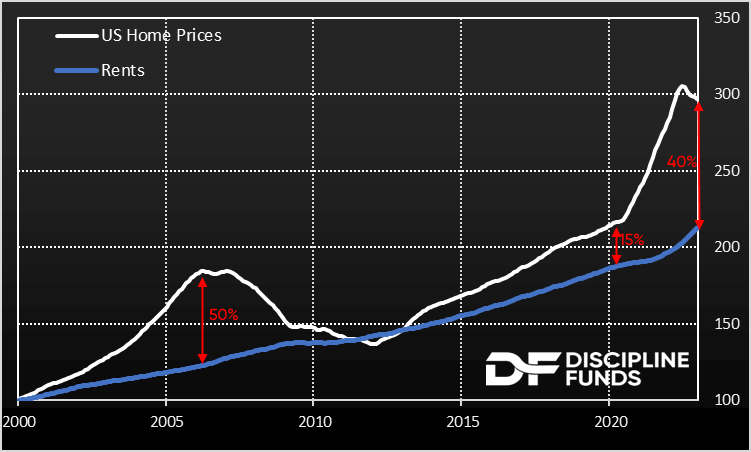

Cullen Roche had a piece this week that compares housing prices to rents since 2000:

Logically, you would think this gap would have to close at some point.

Cullen says we have to be patient to see prices fall:

If there are very few sellers and even fewer buyers then it’s not unreasonable to assume that the sellers will push prices lower as the low number of buyers demand lower prices. Said differently, to use a stock market analogy, if we were looking to buy a stock with a thin set of asking prices and a fundamental price that one bidder thinks is significantly lower than the current market price then that single bidder has pricing power despite the fact that there are only a few asking prices. And if the asks get desperate enough with a patient bidder then prices will fall regardless of the “low inventory”.

I’ve been saying this for well over a year now, but this environment remains one where patience is required. Housing is an inherently slow moving beast and we cannot expect anything to happen rapidly here.

There could be something to this. You can’t buy and sell your home as quickly as you can buy and sell a stock (and for good reason).

It could just be those people who really need to sell will take some time to bring down prices to more affordable levels.

If housing prices do fall in a meaningful way it’s probably going to be more of a slow burn than a crash.

Michael and I discussed the housing market and more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

What Happens if Housing Prices Fall 20%?

Now here’s what I’ve been reading lately:

- 17 stock market charts (TKer)

- The joke (Reformed Broker)

- What is Dunning Kruger explains everything? (Big Picture)

- How long does it take to double your money? (Dollars & Data)

- The true cost of car ownership (The Best Interest)

- Globe trotting curiosity (Freedom Day Solutions)

- Why the data makes no sense (Kyla Scanlon)