A reader asks:

Should most investors reinvest their dividends – why or why not? My initial thought is while still accumulating assets yes, but when withdrawing in retirement take the dividends in cash. I have read stats that say a large percentage of compound returns come from reinventing dividends so seems like a good move and another way to dollar cost average on a smaller scale but maybe I’m missing something.

This is a question that seems basic on the surface but is one a lot of investors probably don’t put much thought into.

Let’s look at the history of stock market returns to show how important dividends have been to performance over time.

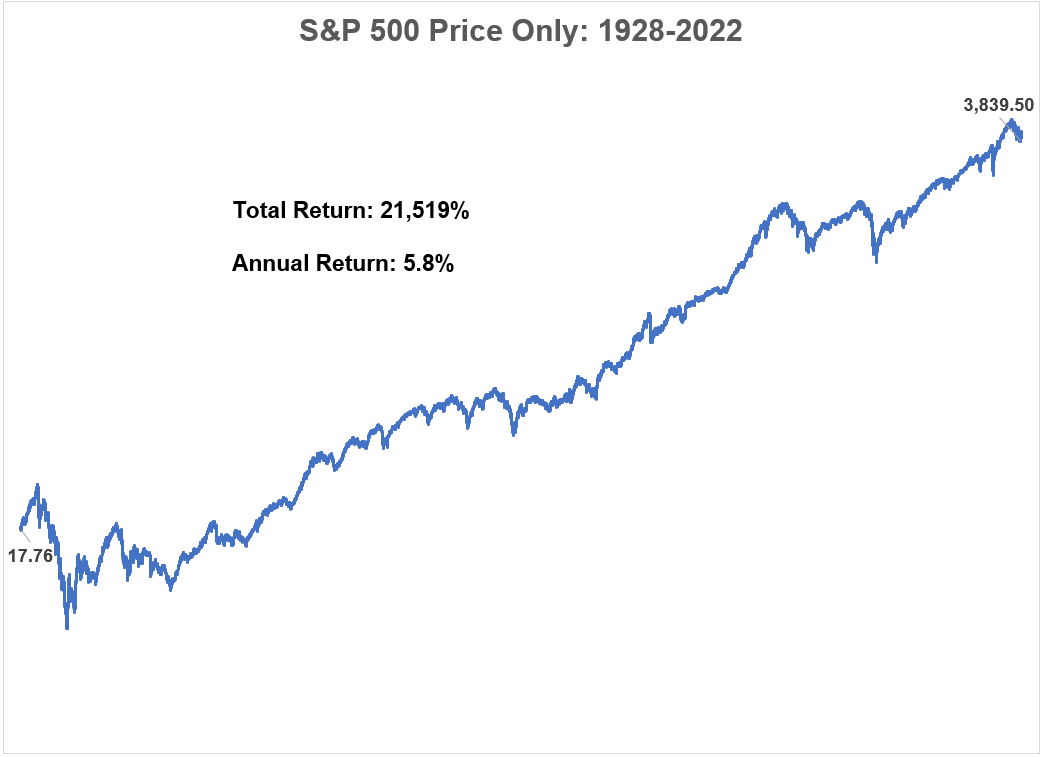

Here is a chart of the S&P 500 from 1928 through 2022 on a price basis:

This is the index without factoring in the reinvestment of dividends.

The price index has gone from a little less than 18 in 1928 to more than 3,800 by the end of 2022. That is good enough for a total return of more than 21,500% or an annualized 5.8% per year.

Pretty good right?

What if we factored in reinvested dividends for a total return number?

This gets us from 5.8% per year to 9.9% annually over the past 95 years of data.

So that’s 70% higher when you reinvest the cash flows back into the market. Does this mean the total returns would be 70% higher as well?

No, it’s far better than that because compound interest works exponentially, not linearly. The total returns are much, much higher.

With dividends reinvested, the total return goes from 21,500% at a 5.8% annual return to more than 750,000% at the 9.9% return.

The total return is around 35x higher than the price return alone. So $1 invested in the US stock market in 1928 in price returns would have grown into around $216 by the end of 2022. With dividends reinvested dividends, now we’re talking more like $7,500.

It should be noted – this doesn’t take into account things like taxes or fees or the fact that it was basically impossible to reinvest your dividends very easily until recent decades.

But that’s a pretty good bump in your ending value through dividends.

Does this mean dividends are the main source of returns?

Not necessarily.

Part of this is the fact that even a small increase in returns can lead to massive amounts of compounding over 95 years. Obviously, most of us don’t have the luxury of having a 95 year time horizon.

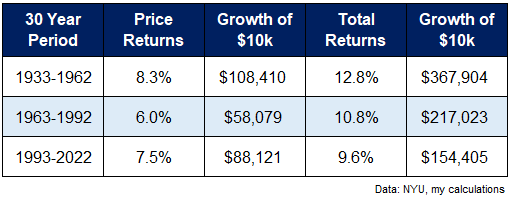

But even over more realistic time horizons, reinvesting dividends can play a large role in juicing your returns. I have roughly 95 years of stock market returns to look at which is good enough for three non-overlapping 30 year periods.

Most investors will have a 30 year time horizon if they’re saving for retirement (some retirees will have that long as well).

Here is a comparison of three separate 30 year periods for the U.S. stocks market along with corresponding price returns, total returns and growth of an initial $10,000 investment.1

The improvement from price to total returns was anywhere from 2-3x better for the growth of that initial $10k investment.

So dividends can have a huge impact on your long-run results if you diligently reinvest them over the long haul.

Now, for retirees, it does probably make sense to utilize dividends or bond income in your withdrawal strategy. You can also be flexible in terms of when you reinvest them or spend them depending on the market environment.

The point here is not that dividends are some magical source of returns. They’re not.

The point is that even slight edges compounded over decade-long time frames can add a ton of value to your portfolio. These slight edges can come from:

- Investing on a regular basis regardless of the market environment.

- Keeping your fees to a minimum.

- Keeping turnover low.

- Being tax aware with your portfolio.

Consistently applying a reasonable investment approach that gives you different sources of small edges and allowing the to compound over time can yield extraordinary results over decade-long time frames.

I know it’s hard to wrap your head around the idea of investing for 10, 20, 30 years or more but that’s where the real money is made.

Compounding truly is a beautiful thing as long as you get out of your own way and allow it to work in your favor.

We touched on this question for the latest edition of Portfolio Rescue:

Bill Artzerounian joined me on this week’s show to discuss questions about putting cash to work in the markets, when to buy a new house in a new city, changes to the tax code and retirement contributions for 2023, tax changes when you get married and when to hire a CPA.

Further Reading:

The Best Source of Investment Income?

Here’s the podcast version:

1I don’t know when we all agreed that $10k was the number but that’s the one we’ve all landed on.