A reader asks:

Inflation was already out of control. Now the war has made gas prices spike. How does this not end in a recession?

This is a valid question.

Inflation was already at its highest level in four decades before war broke out with two countries that are vital to the global supply chain of both energy and agriculture. This is going to make inflation worse.

This morning’s inflation number was 7.9% and that was before the war broke out putting us on the verge of an energy crisis. It wouldn’t shock me to see a double-digit inflation print in 2022.

The probability of a recession is much higher today than it was just two weeks ago.

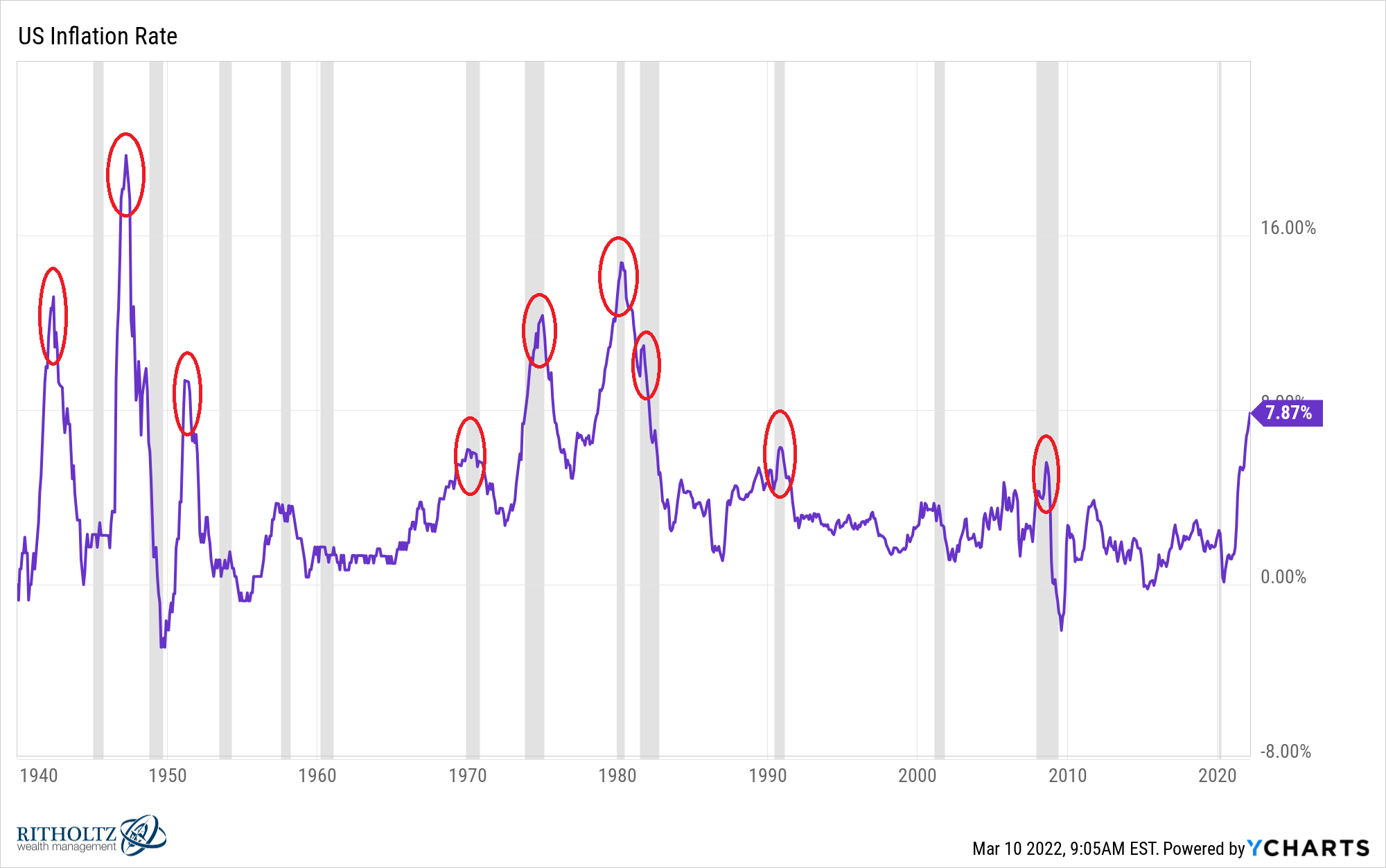

Inflationary spikes don’t cause every recession but every inflationary spike has only been alleviated by a recession.

On the following chart I’ve highlighted every instance since 1940 that the U.S. has experienced an inflationary spike of 5% or more:

Each time inflation went over 5% in short order there was a recession either right away or in short order.

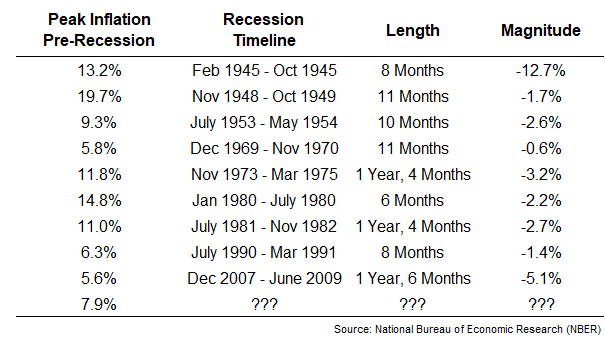

Here’s a list of these inflationary spikes along with the ensuing recessions:

The timing is the tricky part here. Sometimes the slowdowns have occurred after inflation began to fall. Sometimes it happened concurrently. And sometimes the recession was going to happen anyway (like the Great Financial Crisis).

This makes sense when you think about it.

Economies typically go into a recession from overheating and excesses. An overheating economy tends to lead to inflation, which itself is a form of excess. The way those excesses get wrung out of the system is through a slowdown in growth and demand.

So it’s not a surprise that we would see inflationary spikes followed by recessions.

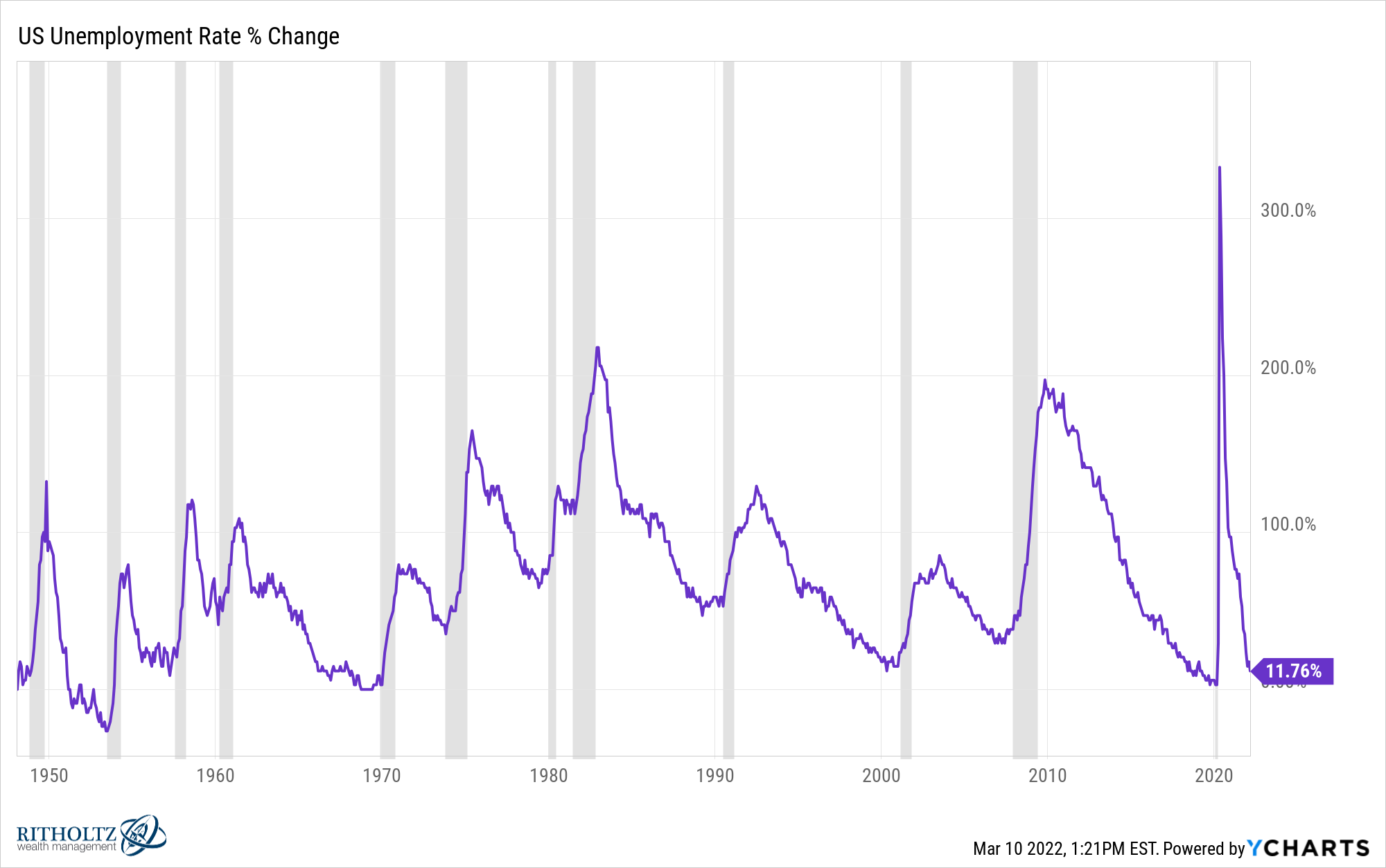

Recessions are obviously bad because lots of people tend to lose their jobs during a recession. You can see the upticks in the unemployment rate coincide with recessions:

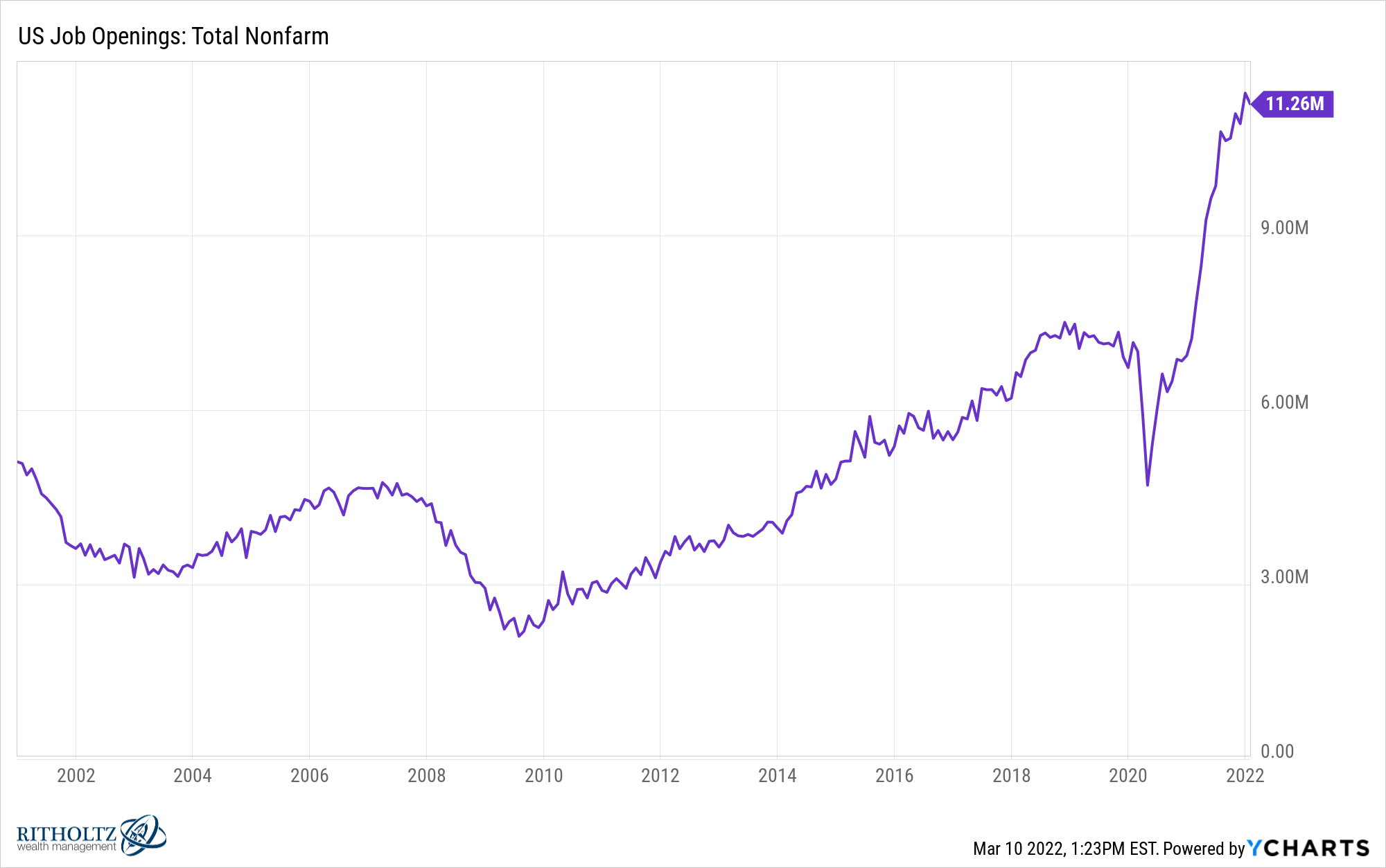

If we do experience an economic contraction, it would occur in the face of the strongest job markets on record. Just look at the number of job openings right now:

The pre-pandemic high for job openings in the U.S. was 7.5 million. We’re now sitting at more than 11 million.

Obviously, the job market can change in an instant, as we saw in early-2020. But my hope is that a combination of a strong job market and sturdier consumer balance sheets would make for a minor recession if it comes to that.

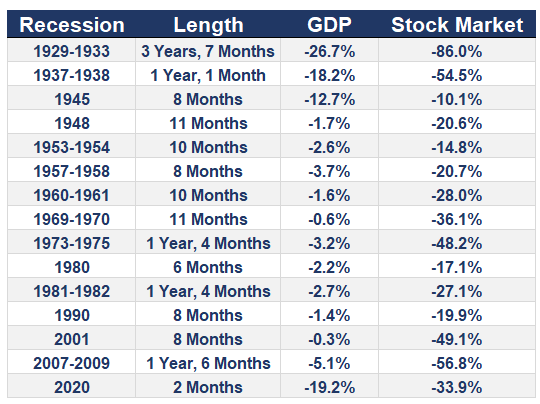

As far as the stock market is concerned, there is a wide range of outcomes in terms of how it reacts to a recession historically:

This list is littered with some of history’s great crashes. But there are also some forgettable corrections and run-of-the-mill bear markets as well.

I don’t know for sure if we will go into a recession or not. If the past couple of years has taught us anything it’s that predicting the future is a fool’s errand.

But I do think it’s important for investors to prepare for a range of outcomes to help set realistic expectations.

There is now a higher probability today than there was just a few short weeks ago that we go into a recession.

We talked about the prospect for a recession and more on this week’s Portfolio Rescue:

Kevin Young also joined me to discuss questions about borrowing against your portfolio to fund a down payment and how to invest a lump sum of money in an uncertain environment.

Further Reading:

The Relationship Between Recessions & Market Crashes