If you only followed the daily swings in the market it may not feel like stocks are going gangbusters in 2019.

The average daily gain for the S&P 500 this year is up just 0.19% (the median is 0.14%). There have only been 9 daily gains in excess of 1% this year (with 3 down days of 1% or worse).

But through Friday’s close, the S&P 500 is up than 18% on the year.

That’s the best start to the year since 1987. Since WWII, there were only three other years that were up 15% or more in the first four months of the year, the others being 1967, 1975, and 1983.

Yet even with these massive gains, it’s been more of a slow, methodical move up as opposed to rip-roaring gains every single day.

And this is generally how compounding works over time. Small gains can eventually add up into big gains if you let them.

The same idea applies to dividends as well.

The S&P 500 SDPR ETF (SPY) was introduced in 1993. In its first full year, the fund paid out a grand total of $1.10 in dividends per share. Based on the year-end price in 1993, that was a dividend yield of around 3.8%

Fast-forward to 2018, and SPY paid out $5.10 in dividends per share on the year. This was a lower yield based on the prevailing price at the end of the year (just over 2%). But if you purchased shares of SPY in 1993, you would now be earning almost 18% on your cost basis in dividends alone.

From 1993 through 2018, the dividend grew over 360% or 6.1% per year.

Six percent in any given year doesn’t feel like much but it can surely add up over time through the power of compounding.

For example, let’s say you have $100,000 that earns a return of 6% annually over the long haul. Assuming an unrealistic world where you earn that 6% every single year you would earn $6,000 in the first year. Then in the second year, you’re earning 6% on $106,000 so your return in dollar terms in $6,360.

That’s not exactly enormous growth in earnings.

By year 10 your 6% would yield more than $10,000. By year 20 the return grows to over $18,100. And if you let your original $100,000 investment grow for 30 years, the 6% return would give you $32,510 at the end of year 30.

That’s good enough for a 32.5% yield on your original $100k. Obviously, it helps that you balance grew to almost $600,000 in that time but this is how compounding works.

It goes slowly at first and you barely see any results. Most of the gains are back-loaded as the snowball picks up steam.

This is one of the reasons it’s so difficult for young people to stick with a long-term savings plan. You don’t see much in the way of investment gains when you’re starting out for some time.

Your savings will trump your investment results for the first couple of decades. And then, all of the sudden, your investment returns take over once you’ve built up a decent-sized nest egg.

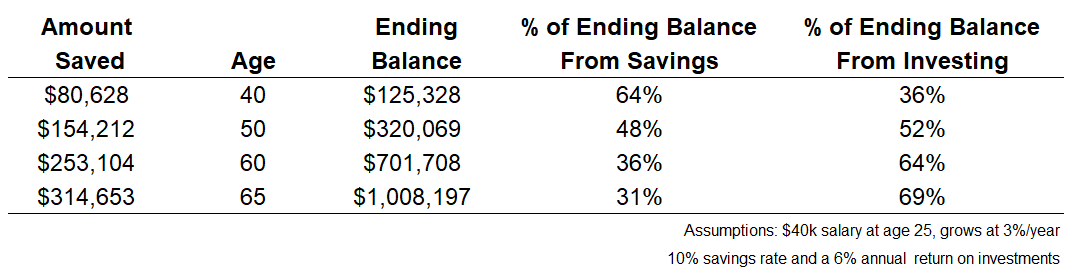

Let’s pretend someone starts out savings 10% of their salary from age 25 and does so through age 65. And in this imaginary spreadsheet world let’s also assume this young person starts out making $40k/year and that salary will grow 3%/year over time for inflation. And let’s keep things simple by again assuming a 6% long-term annual return.

By age 40, our diligent saver would have socked away a little more than $80,000 in savings, with an overall balance of around $125,000 from investment growth. That means almost 65% of the balance comes from saving alone.

As you age that ratio begins to flip but it takes a while.

Here’s how things stack up by different ages using this simple example:

Even by age 50, a whole 25 years after starting saving, the contributions from saving and investing are basically equal. It’s not until 35 or 40 years of saving that the compounding from investing finally begins to overwhelm the amount saved.

Compound interest is extremely back-loaded, which is something that’s hard to see unless you actually plot it out on a spreadsheet.

Small gains can add up over time even though it may not feel like it in the moment.

Further Reading:

When Saving Trumps Investing