A reader asks:

If the goal is long-term investing (let us say I will not look at this money for the next 15 years), then does it still make sense to invest in bonds since equities outperform bonds over a long period of time?

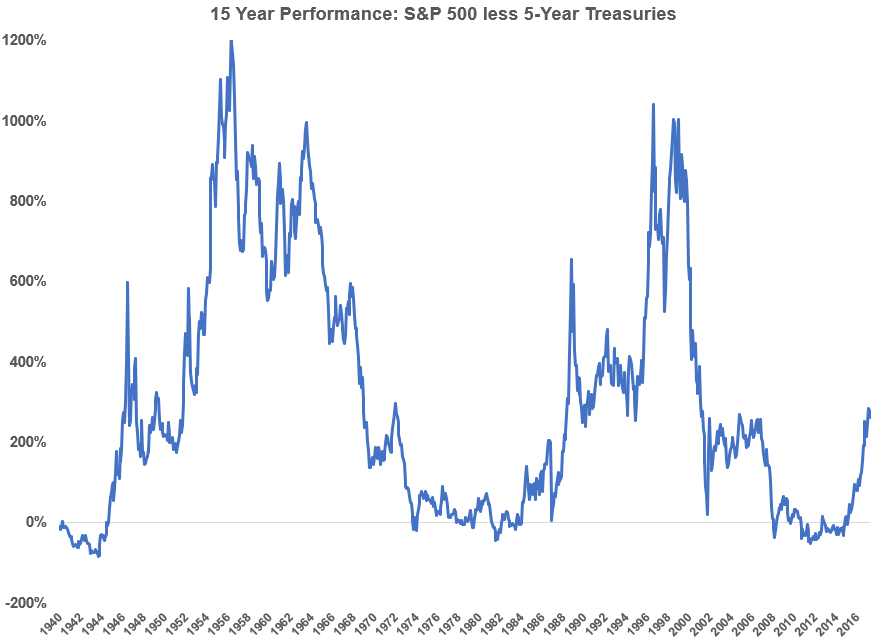

Before getting into the mushy psychological stuff, let’s run the numbers on this. The following chart shows the performance of the S&P 500 minus the performance of 5-year treasuries to show how often stocks outperformed bonds and by how much on a total return basis over rolling 15-year periods:

Since 1926, stocks have outperformed bonds more than 85% of the time on all rolling 15-year periods (using monthly returns). On average, stocks outperformed bonds by around 300% or so in total in this time frame.

Of course, investors don’t get to experience average. While stocks have outperformed the majority of the time there were three distinct periods that saw bonds outperform.

From the late-1920s to the early-1940s, 5-year treasuries outperformed the S&P 500 by more than 60% in total (stocks returned just over 1% a year while bonds gave investors almost 4% annually).

Then from the late-1960s to the early-1980s, 5-year treasuries outperformed the S&P 500 again, this time by almost 45% in total (annual returns were 5.1% and 6.4%, respectively).

And finally, from the late-1990s through the summer of 2012, 5-year treasuries outperformed the S&P 500 by more than 50% in total (4.3% vs. 6.0%).

Finance 101 tells us stocks should earn more money than bonds over the long-term most of the time. That’s the spreadsheet, historical side of the equation.

The risk tolerance side of the equation is a bit trickier because your perception of risk is constantly changing over time depending on your experience with the markets, how markets are performing and what stage in life you’re at.

Young investors should be able to invest every single penny of their retirement assets in stocks because it would give them the highest expected return. But young people also should exercise on a regular basis, eat right, get enough sleep, and of course save for retirement. These things don’t always happen, partly because of circumstance and partly because of psychological constraints.

Investing 100% of your retirement assets in stocks may seem like the right thing to do on paper but very few investors have the intestinal fortitude to pull it off in the real world. Investing all of your money in stocks sounds great until you actually have to live with seeing bone-crushing losses and volatility in your life savings.

I do know people who can handle this but the list is few and far between.

You can perform all the backtests, optimizations, and scenario analysis you want, but there’s no simulating the feeling you get when you lose actual dollars you once had.

My favorite quote on this comes from Fred Schwed, who wrote this all the way back in 1940 in his book, Where Are the Customers’ Yachts:

There are certain things that cannot be adequately explained to a virgin either by words or pictures. Nor can any description I might offer here even approximate what it feels like to lose a real chunk of money that you used to own.

Do you need bonds as a young investor?

Probably not, based on the spreadsheet answer. Current interest rate levels aren’t too far above the historical level of inflation and don’t offer investors much in the way of income.

Should you consider owning bonds as a young investor?

It’s impossible to say but there’s something to be said for the stabilizing effects bonds can have on a portfolio.

They can protect investors against deflation, recessions, and enormous stock market losses. They can also act as something of a hedge against making poor decisions in the stock market at the worst moments.

Bonds may not earn a high return going forward but if they can help you from making a bad decision during volatile markets they serve a purpose. And for those investors, young and old, who want to take more of a barbell approach to portfolio management (this would work for cash equivalents as well) they can diversify your risk buckets.

If bonds, or any other behavioral hedge, can give you a higher probability of sticking with a long-term investment plan then they’re worth holding.

It really comes down to your tolerance for volatility and large losses.

Further Reading:

Do Young Investors Need a Financial Advisor?