As I pointed out earlier this week on Twitter, this Goldman Sachs online savings account now pays a higher interest rate than the 10 year government bond yields in Japan, Germany, France, Belgium, Switzerland, The Netherlands and Sweden:

(Side note: There are a number of these online savings accounts, so it’s not just Goldman that offers this kind of deal. Online savings accounts are typically able to pay a much higher rate than the brick and mortar banks because they don’t have physical branches or as much overhead to pay for.)

The 10 Year Treasury yields just shy of 2% at the moment, so needless to say, investing in high quality fixed income land isn’t such a lucrative opportunity set right now.

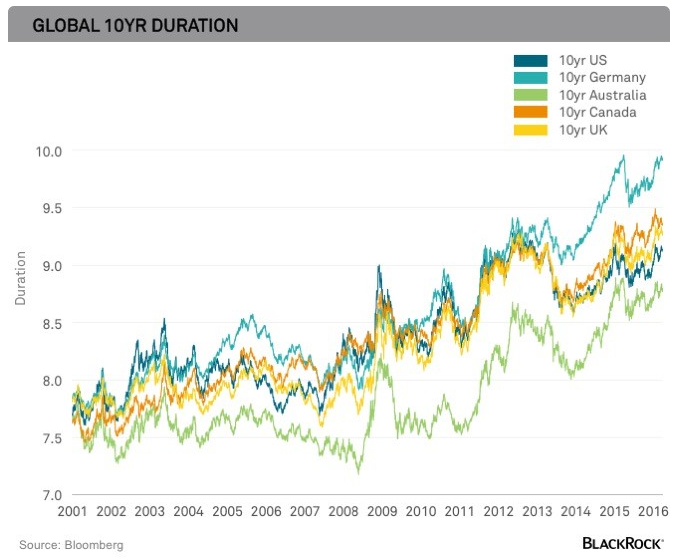

Extremely low interest rates are something of a double whammy of bad news for bond investors. Not only does it mean that returns will be lower than they were in the past, but investors should also prepare for an increase in the volatility of bond prices. BlackRock had a nice piece on their blog last week detailing this issue. Here’s a graph they used to show the decrease in rates has led to an increase in bond duration on a handful of developed country sovereign bond markets:

As rates have continued to plunge since the turn of the century, duration has continued to climb. As a reminder, duration is simply a measure of a bond’s price sensitivity to changes in interest rates. A handy rule of thumb is that duration tells you how much the price would change on a bond in percentage terms for a 1% change in interest rates. For example, a duration of 5 years would imply a 5% increase (decrease) in price from a 1% decrease (increase) in interest rates (remember bond prices and interest rates are inversely related).

Lower yields give investors a much smaller cushion when rates change. The same magnitude of an interest rate move will have a much larger effect on the price of these bonds, all else equal, than it would have at higher yields. So there will be much higher volatility at lower interest rates, thus a lower margin for error.

What’s an investor to do in this low rate world?

- Understand why you’re invested in bonds in the first place. Bonds can still soften the blow from an equity bear market, even at lower rates. If stocks drop 30%, it’s not going to affect total returns all that much if your bonds earn you 2% instead of 6% during an upheaval in the stock market.

- Be aware of the increased potential for fraud. Baby boomers are retiring every day by the thousands. They want stable income during retirement. There will be many hucksters out there promising higher income with much lower risk and this goes beyond the usual chase for yield. With rates on the floor already, it’s not going to take much in terms of a promised yield to get retirees to pay attention. My guess is we could have a number of Bernie Madoff situations — on a much smaller scale — in the coming years promising “safe” income options that turn out to be scams.

- Look to diversify your fixed income allocation. Bonds have basically been a one-decision asset class since the early 1980s. It didn’t really matter where you invested because high quality fixed income in the U.S. has provided phenomenal returns for such a safe asset class. I think it will make sense for many investors to look beyond the typical aggregate bond category and diversify more broadly in to include assets such as TIPS and high quality mortgage-backed securities.

- Reset your expectations. The next cycle in the bond market will not resemble the last one. I’m not smart enough to call the end of the bull market considering basically no one foresaw negative interest rates coming, but at such low yields it’s obvious that returns will be lower going forward and volatility will be higher. Investors should prepare themselves for both.

Source:

Negative interest rates require flexibility in fixed income (Blackrock)

Further Reading:

The Most Interesting Asset Class Over the Next Decade