There’s been something of a bull market in people who consider themselves a contrarian investor in recent years. People took notice of those who called the tech bubble in the late-1990s, the the real estate bubble in the mid-2000s or the bottom of the stock market in early 2009. Everyone would now like to think that they’re greedy when others are fearful and fearful when others are greedy.

It seems as though many of these new anti-consensus investors are trying to become a contrarian for the sake of being a contrarian. They take the other side of every bet. Markets that have gone up must be in bubble territory because of the herd mentality. And markets that have been slaughtered are simply un-loved and due for a comeback. The problem with this line of thinking is that sometimes the crowd is right. Sometimes markets, asset classes and securities are up or down for a reason.

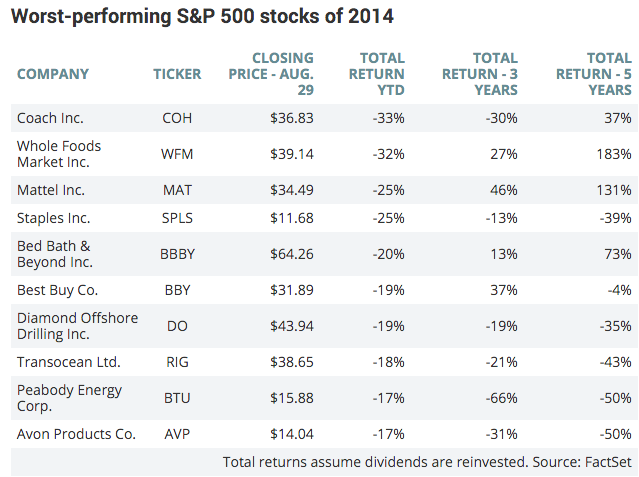

2015 provides a perfect example on why being a contrarian for the sake of being a contrarian doesn’t always work out so well. While preparing my year-end market review I stumbled across a couple of stories from the end of 2014 that I had saved to check back on in the future. This is a list of the 10 worst performing S&P 500 stocks in 2014:

And here are the 10 worst performing single country ETFs from 2014:

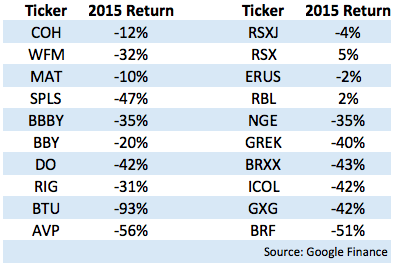

Any self-respecting contrarian investor would look at these types of returns and see the proverbial blood in the streets. Time to go pick up some investments on the cheap. Unfortunately, cheap investments can always get cheaper. Here are the returns for these stocks and ETFs in 2015:

The average loss for these 10 stocks in 2014 was -23%. In 2015, this group showed an average loss of -38%, without a single positive performer. The average loss for the country ETFs in 2014 was -31%. They followed that up in 2015 with an average loss of -25%. Only two of these ETFs showed gains and they were muted at that.

A few thoughts for those who are newly minted contrarian investors:

- You better be patient.

- You better have a plan beyond buy what’s gone down in price. Value matters too.

- You better have a disciplined process that you are willing and able to follow no matter what the outcome is because you’re never going to be able to time these things perfectly.

- Being a contrarian investor can be lonely and painful.

- Not all individual stocks come back from the dead. Markets or asset classes don’t go to zero but individual companies certainly can.

- Avoid anchoring to past price points. Stocks don’t have to trade back up to their previous highs just because they were there before. That past price level is meaningless if the fundamentals of the company have changed.

- Single country ETFs contain more risk than most understand. Yes, they’re more diversified than a single stock, but the majority of emerging market country ETFs are very concentrated in terms of the small number of stocks they own and the relatively un-diversified nature of their industry weightings.

- Eventually some of these stocks and ETFs will see huge counter-trend rallies. Timing is the hardest part of this equation. It’s easy to find things that are down in price but much more difficult to know if or when they will turn around.

- Trends can last much longer — in both directions — than most investors assume is possible. Emotions can cause prices to detach from fundamentals in a hurry and stay that way for a long time.

Don’t get me wrong — I’m all for the contrarian line of thinking when it comes to investing. Incorporating mean reversion and discipline into your investing process can be an enormously powerful factor over the long-term. I just think it’s possible to take the contrarian line of thinking too far.

Sources:

10 best and worst S&P 500 stocks of 2014 (MarketWatch)

Here are the worst countries for investors in 2014 — and maybe 2015, too (MarketWatch)

Further Reading:

Some Stocks Don’t Come Back

A Lesson in Market Crashes