A reader asks:

Will there be any significant premiums in the future? What is the future of risk premiums?

With the amount of competition in the markets nowadays this a legitimate concern. You can now invest in almost any strategy imaginable for pennies on the dollar and do so in a diversified, tax-efficient manner. This is a luxury investors in the past could only dream of.

This reader was talking about the value premium, but he just as easily could have been sharing worries about quality, momentum, shareholder yield, market cap or any other risk factor.

Not only is there increased competition in the financial marketplace for repeatable investment strategies, but investors also have to deal with inevitable bouts of underperformance. When something’s not working it becomes quite easy for doubt to seep in. And people these days are very quick to proclaim the beginning or the end of an era in just about anything. Investors are no different. Based on what you read in the financial media it would seem that well-known investment strategies are dying on an annual basis.

Obviously, no one knows for sure whether or not these premiums will continue to “work” in the future. Cliff Asness talked about the factor cycle in a recent conversation with Tyler Cowen:

If your car worked like this, you’d fire your mechanic, if it worked like I use that word. I think it is harder than you might guess, even if something works long term, to have it go away because a lot of investors can’t live through the bad periods. They decide why it’s never going to work again at the wrong time.

The point Asness is getting at here is that investors would have to collectively become completely rational all at once for risk premiums to be completely eliminated. I don’t see that happening any time soon. In the mutual fund era, investors would chase the past performance of star mutual fund managers. In the ETF era, investors will likely chase the best performing factor ETFs.

But I also think investors need to understand why they invest in different risk factors in the first place. Many try to pick a single factor in hopes of beating the market. I’m a huge fan of simplifying the investment process, but if you’re heavily reliant on a single variable for your investment decisions, you’re probably going to be out of luck unless you are extremely disciplined. Even then it probably makes sense to diversify by different risks and strategies.

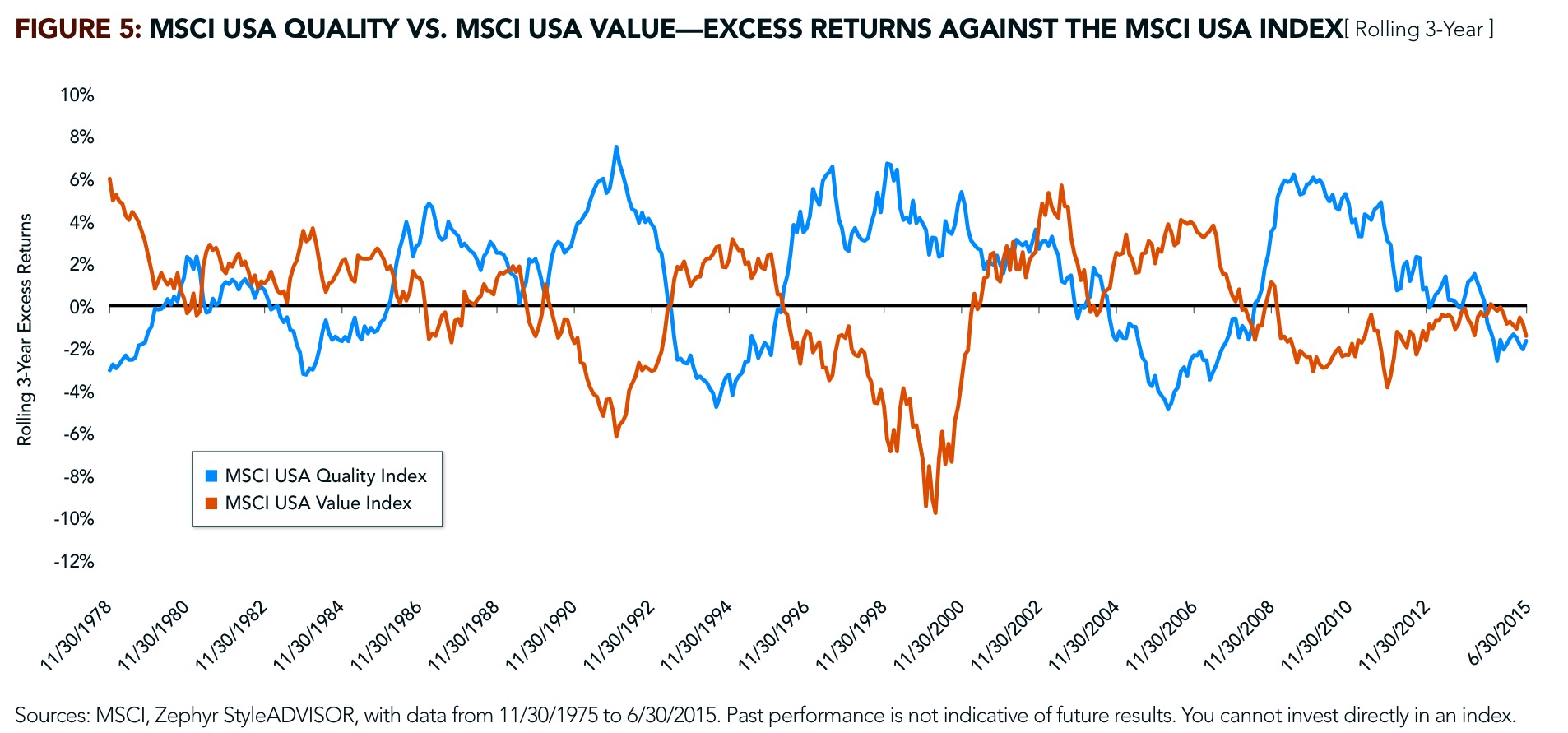

Jeremy Schwartz from WisdomTree had a really interesting graph on the quality and value factors in a recent piece:

This shows the rolling three year excess return for each strategy. You can see the periods of outperformance in quality match up quite nicely with periods underperformance in value (and vice versa). Holding a portfolio of either value stocks or quality stocks would have worked out well for investors during this time frame, but holding a diversified portfolio utilizing both quality and value would have given you a much smoother ride with far fewer sleepless nights.

Factor diversification provides something of a counterbalance so things never get too hot or too cold.

Investors spend far too much time worrying about outperforming the market and far too little time with portfolio construction and planning. It’s not only about finding strategies that have worked in the past that you think will work in the future. It’s about finding risks that complement one another. It’s not just security or asset class selection. It’s about certain investments behave within the construct of an overall portfolio.

In his talk with Cowen, Asness says it would be silly to assume that the historical premiums seen in popular factors won’t become compressed in the future now that everyone knows about them. But knowing about something is not the same as implementing it in real time.

Let’s say for argument’s sake that all risk factor premiums go away in the future. Even if that were to happen I think you could still make a case that owning a handful of different strategies makes sense simply because of the diversification benefits from rebalancing.

If competition in the markets makes it harder to earn risk premiums then investors will have to make sure they take advantage of many minor edges — diversification, rebalancing, tax deferral, compound interest, costs and behavior. The last one — behavior — is by far the most important one because any successful strategy requires that you understand the behavior of both yourself and the other market participants.

Sources:

Cliff Asness: Conversations with Tyler

The Dividends of a Quality and Growth Factor Approach (WisdomTree)

Further Reading:

What Happens When The Umbrella Shop Gets Too Crowded?

Why Value Investing Works

Why Momentum Investing Works

What about the theory that blending too many factors takes you back to cap-weighted benchmark, potentially at greater cost?

How does the above work as a blended strategy vs MSCI USA?

Here’s a good one from Asness that shows how value and momentum work well on their own but even better together: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2174501

I believe more and more people will invest in multiple-factor indicies. Multiple-factor smart beta funds are more and more popular. On the other hand I believe there are no gains without pains so people who stick to SINGLE factor through bad times can outperform the multiple-factor funds.

On a Sharpe Ratio-adjusted basis, do you still believe this?

This is highly unlikely. Unsystematic risk is not compensated in any model of expected returns.

Would you recommend holding a single stock instead of the index? Because that is analogous to suggesting that one factor will outperform several.

There is an example for my concern: the MSCI ACWI

Diversified Multiple-Factor Index has outperformed the plain vanilla MSCI ACWI Index from 2001 every year except 2008. If it is so easy to outperform without periods of underperformance everybody will invest in multiple-factor indicies via smart beta funds. Please check it:

https://www.msci.com/documents/10199/cf31a389-7def-4fd3-8445-cabe63f5b627

Ben,

There is no theory that says ‘combining multiple factors takes you back to the market.’ The market, by definition, has no excess exposure to the factors, so as soon as you tilt, you will hold a non-cap weighted portfolio.

What you may mean is that there is a limit, in a long-only portfolio, for how much you can overweight any one factor as you add additional sorts. As you overweight higher-profitability stocks you must reduce deep-value exposure or risk excessive portfolio concentration.

No, instead, what we find with multi-factor portfolios is quite the opposite of your concern: it’s been possible to combine several factors – say value, size and profitability, in modest amounts across an entire market portfolio, and increase returns above the market with much greater consistency and without any discernible difference in volatility. That of course makes it easier to achieve goals and easier to stay on the path towards those goals. And with a low cost, low turnover, broadly diversified approach, even if factors don’t produce excess returns you’ll still likely get about the market return.

Good!:) Plus https://awealthofcommonsense.com/happens-umbrella-shop-gets-crowded/

Ben (Kumar), here are my thoughts on your question re: blending value and profitability.

1) start with large/small value – there’s a solid risk/return story there and 20+ years of out-of-sample evidence of market-beating durability at the asset-class level. In active form it has been in place since the Graham & Dodd days.

2) recognize this expected outperformance comes with times of significant tracking error relative to the market (in 1998-1999, the Russell 3000 did +22.5% per year, a 60/40 US large value & small value index mix only did +5.8% per year)

3) use large cap profitable growth stocks in conjunction with large/small value to customize the level of tracking error you can stomach (LCG typically > the market when large/small value underperform).

Here’s two working examples (ignoring Int’l diversification):

First, a mix that is 30% US large (profitable) growth, 30% US large value, 40% US small value – about the limit any reasonable investor can stick with. From 1998-2014, it returned +9.9% per year compared to +6.8% for the Russell 3000 with a whopping 0.7 greater annual volatility – a much better long-term outcome. But that hides the ’98-’99 period where the Russell 3000 did +22.5% and the 30/30/40 only did +11.5% – 11% per year underperformance (!!)

If that was two much tracking error, then maybe a 50/30/20 mix would have been better: it only did +8.9% but from ’98-’99 it was closer to the market, +16.9% per year.

Always better to have a lower-expected returning portfolio that you can stick with than a higher-expected returning one that you bail on. Because everything looks awful from time to time.

[…] What happens if risk factor premiums go away? (awealthofcommonsense) […]

Thanks Ben, the Asness paper is decent.

I think I rushed my question, although Eric, thank you for your response nevertheless. Completely agree with the limit that long-only places on factor isolation is difficult – although mitigation is possible, there are definitely implementation limits.

Likewise agree with your second post. Particularly that everything looks awful from time to time!

My question, now I’ve had a sec to think about it, is more simple and specific. The MSCI Growth and MSCI Value indices both reflect 50% of the MSCI USA index according to the MSCI factsheet. Not sure if there is crossover…but my thought was that both together make up the MSCI USA Cap Weighted?

If a novice investor were to buy both, rather than the cap weighted index, do they not end up eating away at their return through rebalancing?

Very specific I know!