Isaac Presley wrote a nice market update recently on his Cordant Wealth Partners blog. He broke down stock and bond yields by comparing some real (after-inflation) and nominal indicators to show where they currently stand in relation to their historical averages and ranges.

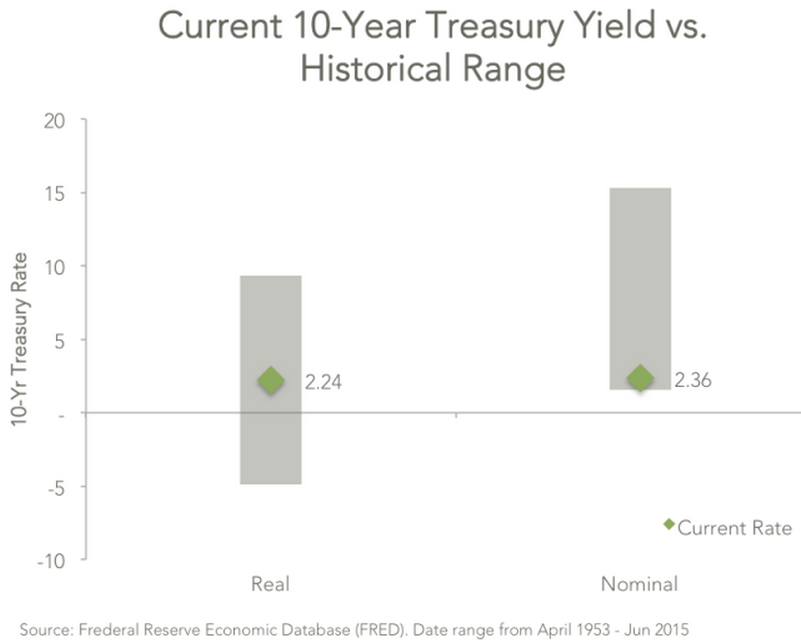

Here’s the 10 year treasury yield going back to the early 1950s:

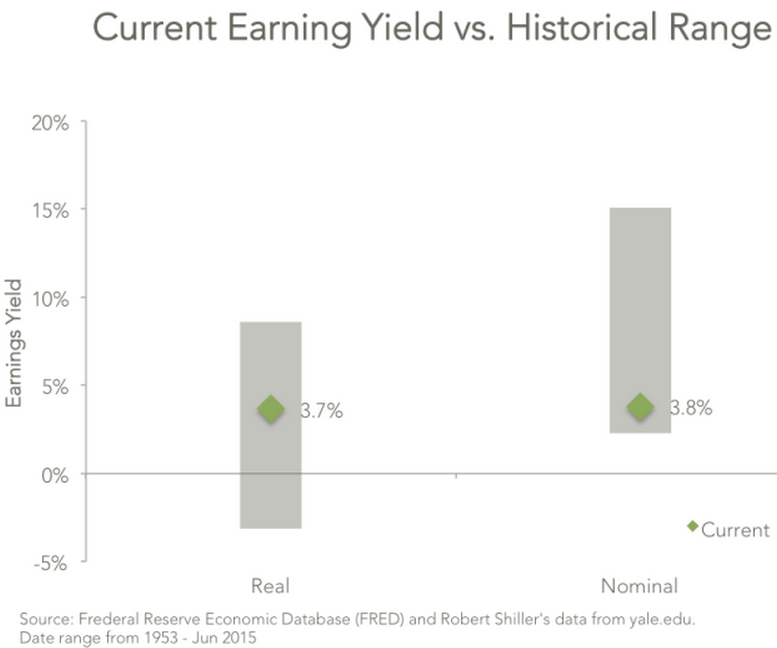

And this is the earnings yield (the inverse of the P/E ratio) on stocks:

You can see in both examples that the markets have dangerously low nominal yields compared to their historical ranges over the past six plus decades. According to Isaac, nominal bond yields have been higher than the current rate 96% of the time while nominal stock market yields are in the highest 10% of historical valuations. This is an obvious cause for concern as lower yields and higher valuations tend to lead to lower returns, on average.

But if you look at these measures on a real basis, they are actually both right in line with their long-term averages because inflation is so low at the moment. On a nominal basis things look scary. On a real basis, not so much. So which value matters more? That depends on whether or not inflation and/or yields pick up in the future and the magnitude of those moves in relation to expectations. As usual, things are not always as easy as they appear on the surface.

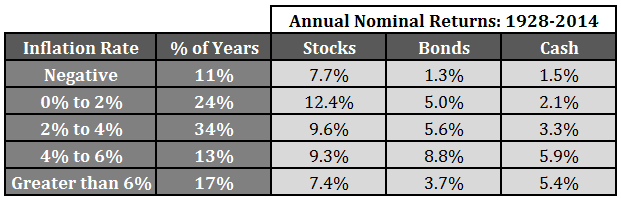

But Isaac’s piece did get me thinking about how inflation has impacted market returns over the years. Using historical data from Professor Damodaran, I took a look at the returns on stocks, bonds and cash (S&P 500, 10 year treasuries and 3 month t-bills) going back to 1928 and separated them out by different annual inflation rate rates:

It’s interesting that the sweet spot for inflation has been in the 0-2% range, which happens to be where we’re at currently. But you should also notice that stocks have really struggled in a highly inflationary environment, which occurred mostly the 1970s and WWII years.

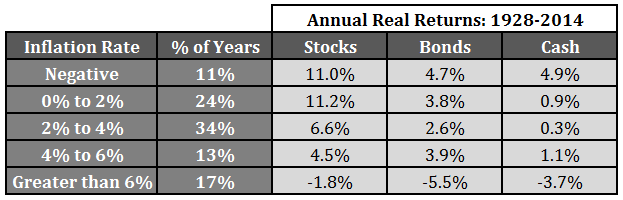

Now, as we saw in the yield examples above, you can’t compare historical averages without taking inflation into account. Historical market comparisons are always difficult because no two cycles are the same, but it’s even that much harder if you don’t take inflation into account across different time frames. Here is the same data presented with after-inflation returns:

Note how drastically different many of these numbers are when you take inflation into account. All of the returns go negative in the highest inflation environments. And the deflationary returns are much better than they appeared at first glance on a nominal basis because deflation actually adds to the real returns.

The real cash returns are another reminder that high yields are largely illusory, because even in those higher nominal yielding decades, most, if not all, of the returns are eaten up by inflation. Again, low inflation looks to be the sweet spot. As inflation rises, average stock returns fall. Bond performance was much more steady until you hit very high levels of inflation, which makes sense since inflation is one of the biggest risks of a fixed interest payment investment.

Inflation is something of a conundrum in the grand scheme of things because too much of it appears to harm financial market returns. But on the positive side of the ledger, inflation usually means rising wages, which hopefully means people can save more money with an increase in income (although things will also cost more).

It’s very difficult to predict when inflation will pick up again, but it’s worth planning for considering we’ve seen inflation of 4% or more roughly one-third of the time over the past 90 years or so. In a future post I’ll cover how investors could potentially protect themselves in the event that inflation eventually picks up.

Source:

2nd Quarter Market Performance (Cordant)

Further Reading:

Inflation is a Relatively New Phenomenon

Fat Tails and Hyper-inflationary Fears

Subscribe to receive email updates and my quarterly newsletter by clicking here.

Follow me on Twitter: @awealthofcs

My new book, A Wealth of Common Sense: Why Simplicity Trumps Complexity in Any Investment Plan, is out now.

It is interesting that no matter what the inflation rate range—-no matter whether returns are “real” or “nominal”—-stocks always “beat” bonds and cash. If only one can survive the volatility………..

This is true (on average). There have been a few longer periods where stocks have lost to bonds, but in general the risk-reward relationship holds here.

[…] How inflation affects market returns (@awealthofcs) […]

@paullavanway:disqus I had never heard of Nick Murray before he was on Barry Ritholtz’s “Masters in Business” podcast last week. But he made the point there is “no place” for fixed income in long term retirement accounts. And I think he even meant for a 60 something year old. He said something like “fixed income is the liquidation of purchasing power.” Anyway, the sentiment was that stocks are the only way to get the kind of return needed for long term financial success. I don’t hear that kind of sentiment often, but I agree. As for surviving the volatility, he advised a minimum of two years of spending in cash reserve, a financial advisor who will not let the investor stray from the plan, etc.

Here’s more on Nick Murray if you’re interested:

https://awealthofcommonsense.com/book-review-simple-wealth-inevitable-wealth-2/

I highly recommend his book Simple Wealth, Inevitable Wealth.

Nice, thanks!

I heard that comment and I think he was dead wrong. In fact, I was taken aback by it. Unfortunately, when people say “Fixed Income” they generally mean treasuries. There are dozens of other options to deploy, Secondly, a decent portfolio with a reliable income stream is nothing to turn your nose up in retirement. Preservation of capital with income being thrown off is what I built a good part of my business on, and both my clients and I are quite pleased with the results.

One only has to look at the performance of energy related MLPs in the past year, and think what misery that must have brought millions of investors.

[…] How inflation affects market returns […]

[…] How Inflation Affects Market Returns (A Wealth Of Common Sense) […]

[…] Dont forget to consider inflation when looking at what your long term (and short term) returns have been. At the end of the day, real returns are what matter not nominal returns – How Inflation Affects Market Returns […]

[…] this week I took a look at how inflation has affected market returns over the years. As you can see from the chart below, inflation has historically run in excess of 4% […]

[…] nominal interest rates (the market rates) and real interest rates (nominal rates minus inflation). This post does a good job of showing the difference. It explains that today nominal rates seem very high […]

[…] How Inflation effects market returns […]