Just when I think things are slowly turning in favor of the financial consumer, I’m reminded of Wall Street’s old ways of doing things like putting fees, profits and margins ahead of client interests. There were three things I saw this week that showed Wall Street’s old guard isn’t going to go down without a fight for every last basis point of their investor’s money that they can get their hands on.

1. Morgan Stanley’s margins. On CNBC this week, bank analyst Mike Mayo said that Morgan Stanley is one of his top bank stock picks right now. One of the reasons he stated for this pick is because the CEO wrote in his latest letter to shareholders that one of the biggest goals of the firm this year is to get the margin in the wealth management division higher than it’s ever been in history. Translation: More for us, less for you.

Contrast Morgan Stanley’s strategy of margin expansion with Vanguard’s bonus system:

One example from Vanguard: The company has a partnership plan that calculates bonuses for employees based on how much less Vanguard’s expense ratio is than its competitors’ and how much its funds outperform. During Bogle’s tenure as CEO, annual bonuses could amount to as much as 30 percent of an employees’ pay.

Which firm would you rather partner with as an investor?

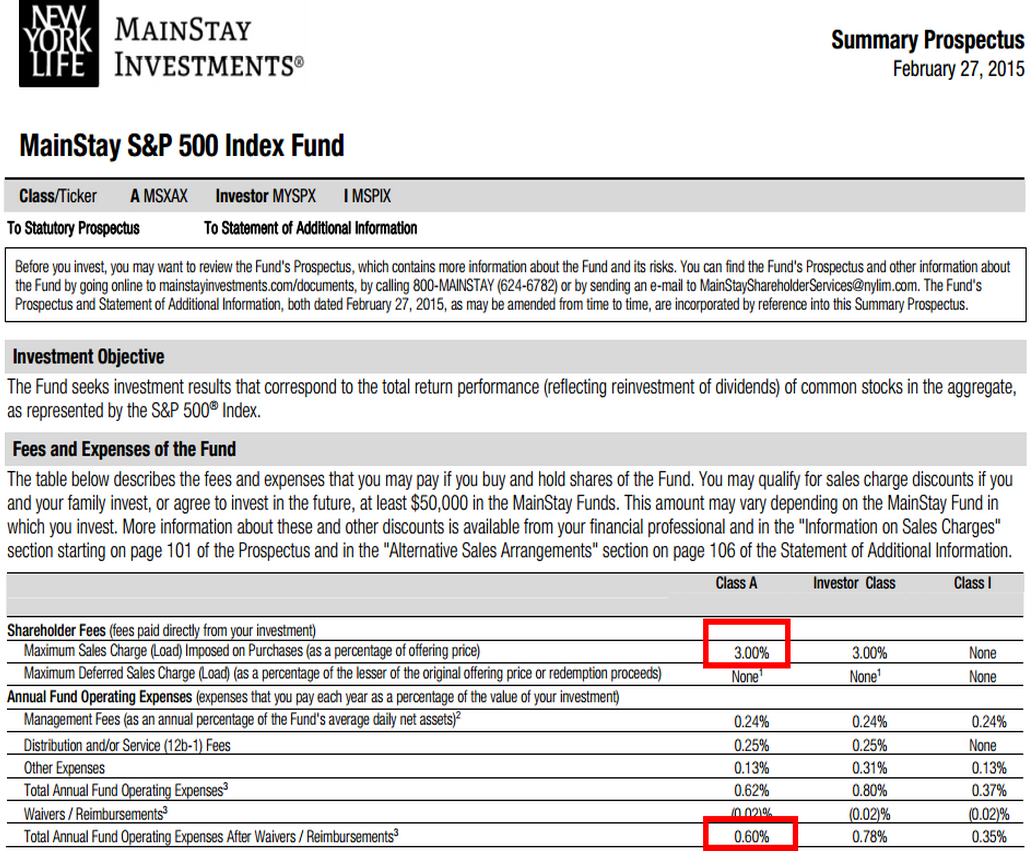

2. A ridiculously priced index fund. This one comes from my friend Wes Gray at Alpha Architect:

This S&P 500 Index Fund from insurer New York Life carries a 3% sales load. Even if you were able to skirt that egregious fee, you’d still pay 0.60% for the expense ratio, including a useless 12b-1 fee that should be outlawed. For comparison purposes, investors can buy the SPY ETF for 0.09% or the Vanguard 500 Index Fund for just 0.05% in the Admiral share class. These funds are all set up to do the exact same thing – track the S&P 500 index. The only difference is the fees. Supposedly most of the funds are in the Class I fund, but that doesn’t excuse the pointless fees that are sure to nail unsuspecting investors who don’t know any better.

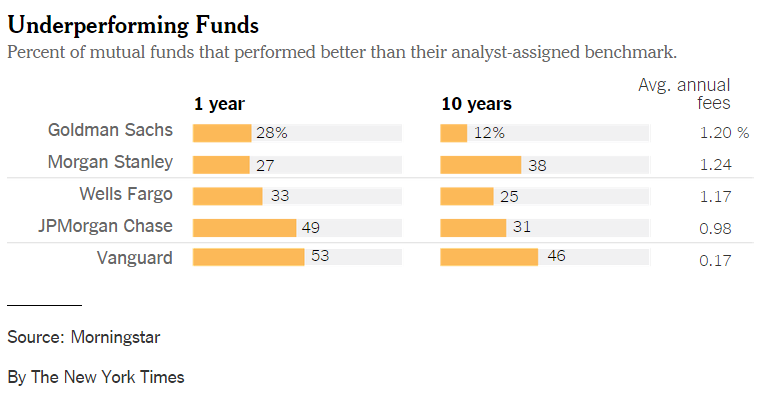

3. The Vampire Squid strikes again. Courtesy of the New York Times, the mutual fund offerings from the big banks are of the high-fee, low outperformance variety:

No worries. Goldman Sachs is doing just fine as they brought in $73 billion from new investors last year and continue to roll out new fund offerings at an impressive clip:

When Goldman’s chief financial officer, Harvey M. Schwartz, spoke about Goldman’s “strategic initiative to grow asset management” on his most recent call with investors, he said that the “team’s done a great job.”

For Goldman’s bottom line, the business has indeed been doing well. During 2014, the company’s funds drew $73 billion of new money from investors, increasing revenues in the investment management division by 11 percent over the previous year. Goldman has nearly doubled the number of mutual funds it has offered over the last decade.

Nice job team.

All fees and firms on Wall Street are not evil as some people assume. This has more to do with trust and honesty than fees. I just don’t see a scenario where these types of firms will ever truly care about their clients and investors. It looks to me like they’ve decided they’re going to wring out every last drop of fees that they can before their clients wise up. Of course, most clients won’t wise up to this game. Some people like investing with a firm because of the name on the side of the building, the size of the research team or the narrative of the marketing department.

But I think many people really have no clue what they’re getting themselves into when the invest with one of the behemoth financial firms. It’s very easy for financial professionals to talk over the heads of their clients and wear them down with the trust-me-I-got-this line. Prestige and a knowledgeable sales staff is still a formidable combination when it comes to gathering assets.

Things are improving for investors, but there are still financial firms that would rather keep the status quo.

Sources:

The Impossible Sale: An S&P 500 Index Fund at 60 bps with a 3% Sales Load (Alpha Architect)

Wall Street Banks’ Mutual Funds Can Lag Returns (New York Times)

Jack Bogle’s Success Principles to Live By (CNBC)

Further Reading:

What Would You Say…You Do Here

It’s Not a Chase For Yield, It’s a Chase For Fees

Subscribe to receive email updates and my monthly newsletter by clicking here.

Follow me on Twitter: @awealthofcs

I pay 1% for a S&P 500 in my 401k. But no load, so thats cool at least =/. That is also the cheapest fund, the target dates are in the 1.3-1.4% range (wish I was joking)

Wow. That’s crazy. If you don’t mind sharing — large employer or a small business? Usually small businesses have the worst 401ks. That’s insane. These kinds of things never cease to amaze.

Mass Mutual is the provider, ~150 employees, but likely < $5m in assets (pretty new company). A few of us have brought it up multiple times but its more or less too late, the company didn't seriously negotiate up front and can't do much short of moving to another provider.

A problem I’ve heard from a number of people. The issue in many organizations is that the people choosing the plans usually have no background in the financial markets so they are just doing what these companies tell them to do. That’s too bad. Hopefully they at least give you a company match to make up for it.

Jackson, the smaller employer retirement plan industry is a wasteland of excessive fees and abuse. There are many reasons, not excuses, for this. Average fees for smaller plans run around 1.3% to 1.4%. Ben mentions a couple of them and there are many more. Unfortunately, smaller employers rely more on relationships with brokers and “consultants” and do limited meaningful shopping of their plan.

Mass Mutual is probably providing a bundled solution and explaining to your employer how it is “streamlined” or “turnkey” or some term that sounds simple. They do the record keeping and provide some employee guidance and, on a day to day basis, the employer doesn’t worry about anything. Who knows, maybe there is an adviser or broker on the case that meets with the employees too and sells them more overpriced products. (Many brokers and RIA’s use the employer based plan as a venue to sell other products and services – it is a gold mine of revenue). Of course,it is all nonsense.

As a point of comparison, your employer can use an unbundled product and get all Admiral shares from Vanguard, full record keeping from an independent record keeper (there are plenty that do this type of work) and full fiduciary and advisory support. For a case of $5 Mil and 150 people, the all in costs might be around $22K or so, or about 44 bps per employee. That would be everything.

You think it is bad now? It gets worse for you and your colleagues! As the plan assets grow, and your account grows, you pay more because MM charges the fee as a percentage of assets – in many cases for virtually no more work! In the unbundled example I listed above, much of the cost is a flat fee, so it will go down to around 25 bps or so (still an all in charge) for the employees.

This is real money you are losing that goes to the financial services industry instead of your future. You and few of the other staff should get a quote and show it to the plan sponsors and ask them how they can justify these additional, crazy costs. You don’t want to jeopardize your job, but this will clearly cost any long term employee a significant amount of money and time in retirement. Good luck!

Yes, I’ve heard the Vanguard option is very cost effective. They should be the one everyone is shown first. Thanks for the color on this. Hopefully this is the next piece of the industry that gets fixed through better technology & lower costs.

[…] The finance industry is not going down without a fight. (awealthofcommonsense) […]

[…] A Wealth of Common Sense told us Wall Street is not going down without a fight. […]

If you think that’s bad check out the SP 500 Index Fund from State Farm. 5% load and .75% expense ratio. Sickening.

https://www.statefarm.com/finances/mutual-funds/funds/index-funds/s-p-500-index-fund

Wow. Unreal. Both fees are terrible, but when you combine them it’s even worse. Terrible

This was a standard question that I asked new clients or prospects with assets at other firms and was continually amazed by how little they knew about what they were paying for their investments. If it was a brokerage client, they were of course getting their account services for free! Worse yet, most consumers have even less of an idea of what the cumulative effect of higher fees will be on their investments over time and were shocked when they learned that even small differences in fees can translate into significant dollar differences. The source of the problem was usually ignorance, indifference or, worse yet, misplaced trust in “Joe” at their previous firm who was always so nice to them!

It’s hard to know who’s more to blame here — clients that don’t educate themselves or the financial professionals who do everything they can to earn fees over all else. Probably a 50/50 split. It’s just too bad most people have to deal with poor advice before finally realizing what they’re missing.

My wife’s last firm went through Edward Jones… all high fee funds in her 401K. We got just the matching, dumped it in cash, and are in the process of closing out the account to move to Vanguard. When I went through her plan prospectus, there were so many unique fees, some of them just gotcha’s, that I lost track and had to start marking them down on a piece of paper.

Ouch. Good plan on taking the match and moving it over but it sure would be nice if there was a better way of doing things. I’m not a huge fan of the gotcha-fees either.

A difference of 2% in fees and expenses can make a huge difference over a long period of time. Using the market’s long term return of 9.6% over a 40 year period I did two calculations. The first was a one time investment of $10,000. 2% in fees/expenses cost the investor about $204,000 over 40 years. Second was an investment of $100 a month. 2% in fees/expenses cost the investor about $254,000 over 40 years. High fees/expenses are really costly to an investor over a long time period. Companies and advisors should have to show how the funds they are selling perform over a long time period, say 40 years instead of the norm of 10 years, compared to their market benchmark taking into account fees/expenses. No one would buy a high fee fund plus pay for an advisor if they saw such a comparison.

Good information here John. There probably aren’t enough investors out there who realize this quite yet. Obviously you have to pay something if you’re getting advice from someone, but paying high fees for funds on tops of high fees for advice is a great way to throw a lot of money away. This should be one of the first questions people ask of a potential advisor.

[…] last 10 years but there are still some egregious examples. Check out some of the ones discussed here. A New York Life SP500 index fund with a 3% front end sales load and a 0.62% annual fee! This fund […]

[…] is a great post by Ben Carlson at A Wealth of Common Sense which highlights one of my main purposes for starting TAMMA which is to provide affordable […]