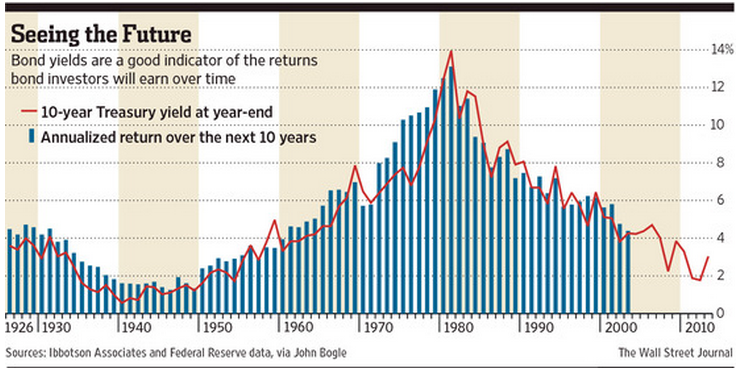

Last week I looked at some of the options available to bond investors in a low rate world. I showed that subsequent returns over the next decade tend to track the current interest rate level very closely. Here’s that graph again from the Wall Street Journal:

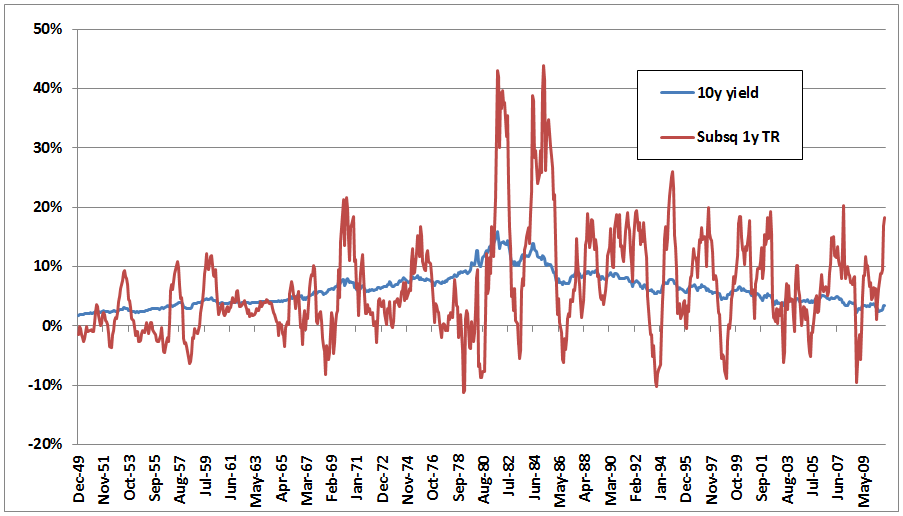

If only it were that easy. Thinking in 10 year increments isn’t something most investors can handle. One of my astute readers, named Jim, wondered how far out of whack the returns can get over any one year period from this long-term trendline. So if the current interest rate is very predictive of future performance, what happens when rates move or investor expectations trump this long-term reality? Here’s a graph that Jim sent me:

The blue line shows the same 10 year treasury yield from the WSJ chart, while the red line shows the subsequent one year total return on the 10 year bond. You can see how wild the fluctuations are. A couple of times in the 1980s the one year return was over 40%. This is pretty massive volatility for bonds, although the one year loss seems to have a floor at around 10%.

Holding individual bonds is often looked at as being superior to bond funds because you can simply hold an individual bond until maturity. In theory, you can ignore the price fluctuations if this is your strategy, but it still introduces temptation to make an unwarranted move.

I was talking with a retiree earlier this year who was worried about interest rates rising in the future. He set up a bond ladder by staggering the maturity of his bond holdings. For the uninitiated, a bond ladder is a way to spread out interest rate risk by buying bonds that mature at different times. As holdings mature and the principal amount is paid back, you reinvest the proceeds in a new bond at the prevailing interest rates. This keeps the portfolio balanced across the desired maturity profile and allows investors to take advantage of higher rates, should they ever materialize. l think a bond ladder is a great way to manage risk in a highly uncertain interest rate environment.

This gentleman set everything up so it would more or less run on auto-pilot, which is another good idea to keep emotions out of the equation. But once everything was in place, the markets tried to lure him out of his process as interest rates fell and the value of his bonds went up. Although this guy had painstakingly set up a bond ladder to take himself out of the equation, the market was tempting him with higher prices.

He wanted to know what he should do. He was considering selling the bonds to lock in the gains, but then he would still have to reinvest his proceeds at the now lower interest rates.

I didn’t have an answer for him but I did come back with a couple of questions — Why set up such an intricate bond ladder in the first place if you’re not going to follow it? Maybe it would be a good decision to sell your bonds, maybe not, but wasn’t the entire point of the bond ladder to take away the guessing game of what’s going to happen with interest rates?

This is the problem with the markets. They are constantly tempting us. It’s like they want us to behave badly so the market gods can laugh in our faces. Setting up a systematic process or portfolio is easy. Following that process is the real challenge because the markets never make it easy on you.

Further Reading:

How Interest Rates Affect the Behavior Gap

How to Create a Bond Ladder Using ETFs

Subscribe to receive email updates and my monthly newsletter by clicking here.

Follow me on Twitter: @awealthofcs

[…] Markets Tempt Us Into Mistakes […]

Thanks, Ben, for incorporating the graph into your post.

To receive the full benefit of a bond ladder, one needs not only to stay the course for a number of years (so that lower yield and higher yield purchases benefit from cost averaging), but also with a relatively stable amount of capital. Otherwise, if the account value is changing sharply, newer purchases will be overweighted or underweighted compared to seasoned ones.

Probably only a minority of investors are well suited for bond ladders. Among the top 10 government bond ETFs, all but one are focused on specific maturity ranges. Active bond managers try to hold shorter maturities than their benchmark when rates are rising, and longer maturities when rates are falling. But as the graph shows, bond yields contain a lot of noise, and often don’t trend as well or as long as equities.

Backtests of an indicator using the yield curve (which is anything but random, owing to Federal Reserve control of the short end) show that some value can be added using this indicator to adjust maturities.

Right, it’s easier than ever to diversify by maturity using bond funds only. Plus they are starting to create bond funds with a maturity date if you are so inclined to get out of the constant maturity game.

I think the bond market is where people giving financial advice over the next one or two decades are going to have to prove their worth, not the stock market.

there are no market gods, only the rapacious bastards who make money when you lose yours.

I guess the market gods would be the fee extractors on Wall St. They get paid either way.

All I have to say is we have enough to volatility worries with equity markets why sweat the bonds at all….ever? The bond portion of my investments plod along and have done for years now, they don’t make a bundle and they don’t loose a bundle, I put money there for this very reason. This is supposed to be safety portion of a portfolio. When I hear debates on buying and selling bonds like traders discussing equities I just don’t get it.

Great point. I believe everything in your portfolio should be there for a reason. Take your volatility were it will actually pay off (stocks) and use bonds as the stable portion to control emotions and use for rebalancing when stocks fall.

[…] Markets are always tempting us to make mistakes. (A Wealth of Common Sense) […]

Your post Ben reminds me that the best portfolio / financial plan is one you can stick with. Too many investors dive in and out of products. That’s not a good thing.

Personally, I don’t own bonds and don’t intend to for many years. These things will get hammered if and when rates rise. If they don’t rise, and stay low for many years to come, some people (heavy in bonds) will still lose out.

Mark

I agree. The only perfect plan is the one you can personally follow. I think the bond market is going to be facinating to watch over the next decade or so. Much more of an issue for retirees than young investors.

[…] A Wealth of Common Sense told us markets tempt us into making mistakes. […]

[…] Ben Carlson explains how the market tempts us into making mistakes. […]

[…] Regarding Bond Yields and Subsequent Bond Performance from Ben Carlson […]

[…] How the market tempts us – A Wealth of Common Sense […]

[…] Further Reading: Are We Witnessing a Melt-Up in Long-Term Bonds? How the Markets Tempt Us Into Making Mistakes […]

[…] See also: How interest rates affect the behavior gap & How the markets tempt us into making mistakes […]

[…] Reading: How the Markets Tempt Us Into Making Mistakes Advice Doesn’t Have to be Complicated to be […]

[…] • The “Misery” Index Falls to an 8 Year Low (Pragmatic Capitalism) see also Fed’s Rate Dilemma: Job Gains vs. Low Inflation (WSJ) • Most Innovative Companies 2015 (Fast Company) • Hedge Funds Keep Winning Despite Losing (WSJ) • Shark Tank: The lost pitches (Fortune) • How the Markets Tempt Us Into Making Mistakes (A Wealth of Common Sense) […]

[…] How the Market Tempts Us Into Making Mistakes — (A Wealth of Common Sense) […]

[…] How the Markets Tempt Us Into Making Mistakes (awealthofcommonsense) […]

[…] https://awealthofcommonsense.com/markets-tempt-us-making-mistakes/ […]

[…] other big risk in bonds, and long maturity bonds in particular, is temptation in the short-term. Here’s the one year rolling returns for long-term […]

[…] Further Reading: How the Markets Tempt Us Into Making Mistakes […]