“The intelligent investor realizes that stocks become more risky, not less, as their prices rise, and less risky, not more, as their prices fall.” – Jason Zweig

If you’re in the business of fear-mongering, one of the go-to moves to try to scare investors is to predict that the markets are looking eerily similar to October of 1987.

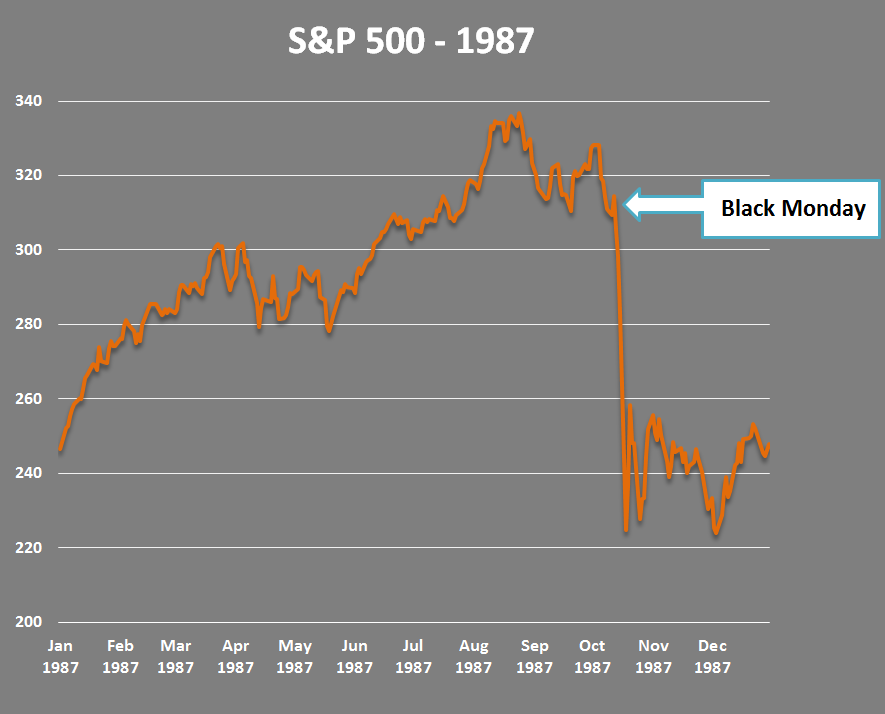

Black Monday is forever seared into the psyche of every trader and investor that was part of the markets on that fateful day. Investors of today are constantly reminded about the time the S&P 500 dropped more than 20% in a single day.

What many people don’t realize is that the three days leading up to Black Monday saw stocks fall over 10%, including a 5% drop on the preceding Friday. So in four days stocks were down more than 30%.

Interestingly enough, on a price basis the S&P finished the year basically flat, but on a total return basis, with dividends, was up around 5%. Doesn’t matter — crash, crash, crash is all anyone remembers.

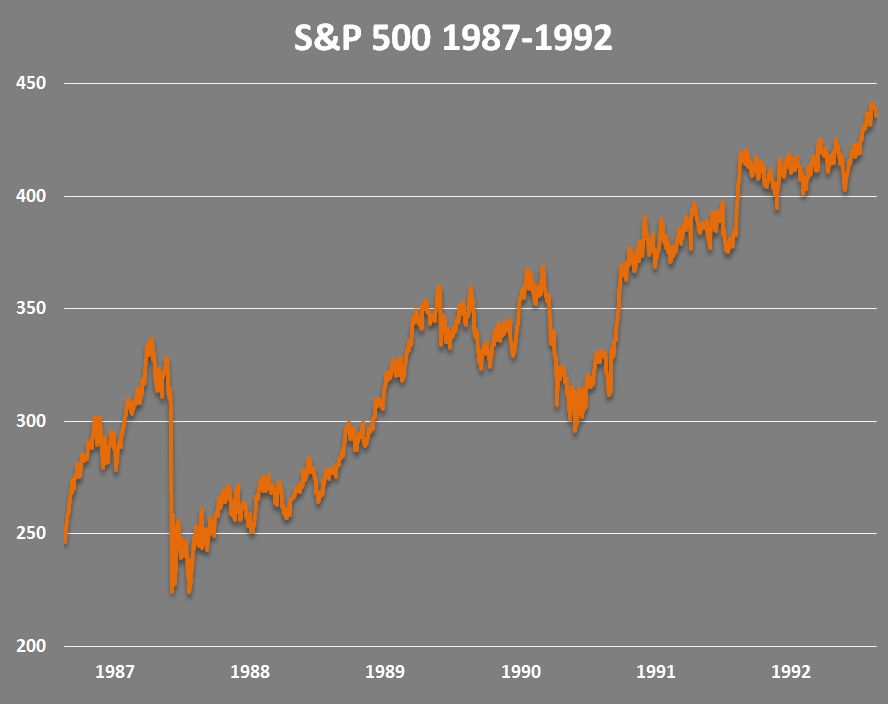

It’s also worth noting that Black Monday didn’t even really derail the market. Here’s the S&P over a six year period from 1987 through 1992:

Now 1987 looks a little more manageable. Still a huge drop, but in the context of a market that was up over 120% or 14% a year from the start of 1987 through the end of 1992, not too bad. No one talks as much about the gains, but investors will always speak of the huge Black Monday crash. This is a classic case of short-term myopic loss aversion overwhelming long-term market gains.

You could actually argue that the 1987 crash was a good thing for the markets. It knocked some of the wind out of its sails after more than doubling from 1982-1986.

From current levels, a 30% drop in the S&P 500 would take the index down to just over 1,400. That’s a mark last seen in December of 2012. So all of 2013 and 2014’s gains would be wiped out.

The S&P 500 currently trades at a P/E multiple of roughly 17x this year’s earnings. Earnings have actually grown more than 16% since late 2012 so a 30% drop would leave us with a P/E ratio of 12x. For anyone with a decent slug of human capital in the form of future savings, this type of swift wipeout would be a gift. Stocks would be marked down at a huge discount to current valuations.

This type of loss would tough for those with a mature portfolio, but for everyone else the biggest issue would be psychological. Stock market crashes are always thought of in terms of being frightening, scary and unnerving.

Earlier this year, Jason Zweig tweeted out that he once proposed the BGFN channel (Benjamin Graham Financial Network) that would cover market crashes as good news. Changing your mindset from how a crash affects your current performance to how it will affect your future performance is one of the keys to mastering your emotions when investing.

Historical market scenarios never happen exactly like they did in the past, so this is really just an exercise in crash preparation for the next time the market takes a dive.

These periods will never be easy, but they are necessary and one of the best things that can happen to an investor with a long time horizon, provided you have the right mindset.

Further Reading:

Even bull markets aren’t easy

[…] 1987 Crash Really That Bad […]

[…] What would a replay of 1987 look like? (A Wealth of Common Sense) […]

The challenge for investors to take advantage of a one-day crash like ’87 is that they’ll have no idea if it is in fact a one-day drop or the start of a prolonged crash like 2008-09. Think of an investor who deployed significant capital in October 2008 after the markets tanked in late September. He or she would watch in horror as the market continued to slide for another five or six months. Psychologically devastating, even though the move was probably fine on a long-term basis.

Right, I think the worry that worse is yet to come is always what keeps people from investing during a crash or correction. I actually noted on Twitter a few days ago that Buffett called it a buying opportunity in Oct ’08 but stocks fell another 30% from there. Still, up 130% from that call. Timing is always impossible to nail.

[…] are scared again – CNN/Money The Dollar’s Impact on the S&P 500 – Reformed Broker Would a Repeat of the 1987 Crash Be That Bad? – Wealth of Common Sense Everyone is a genius in a Fed-induced stock rally – […]

[…] Would a Repeat of the 1987 Crash Really Be That Bad? […]

As one who was actually invested in 1987 (and since 1973), I still have vivid memories of that market crash. It is oh-so-easy to look today at a long-term chart having a tiny blip and say “So what!…of course the market recovered…those who sold were fools”.

In 1987, market news was nothing like it is today. We had no Internet. We had the next day’s WSJ, and Friday’s 30-minute Lou Rukeyser’s Wall Street Week, we subscribed to a few stock newsletters (delivered by snail mail), and Kiplinger and Money magazines…that’s about it.

Therefore, though I heard about the crash on the radio as I drove home from work on Black Monday, I was not prepared to find my wife in tears…her first words were “You’ve lost our retirement!” (Reading it does not convey the impact of hearing it.)

In real time, the crash was a VERY big event. Fear for a changed future was the natural response. Talking heads were saying “This worldwide event could last for years; our children will have a lower standard of living than we have”.

Long story short–she insisted we sell everything the next day (which was also a significant down day); we eventually re-entered the market; I retired at age 53 in 1995; and today, my IRA is 3.5 times greater than at retirement (in spite of zero new $$$, 2 more market crashes, and 2 significant RMDs).

So, if you were to ask for advice, it would be this…

A couple’s ‘comfort zone’ is not of the one investing–when it counts, it is that of the most conservative spouse. Thus make a plan that keeps your spouse advised of investment decisions–for example, I prepare and review with her a monthly report on changes to investment value (against a melded S&P500 benchmark), also quarterly net worth statements, and semi-annual asset allocation summaries. She also reads the WSJ daily, and is very well self-educated in the market.

However, I don’t expect her to take-over as an active portfolio manager when I’m gone–but I am comforted to know she will not be the victim an “adviser” hoping she will accept questionable advice that mostly pads his pocket.

I recommend she do as Warren Buffet recommends…move the majority of our stocks to low-cost index ETFs (most likely, she will also retain for income some of the stocks, such as PG, JNJ, & T, as well as the utes).

This is a great perspective. Didn’t mean to trivialize the event, just trying to point out the fact that a market crash is a great thing for a long-term investor, despite the fact that it will be the most terrifying investment moment you go through. It will never feel like things are going to come back. Same thing happened in 08-09. They’re all different but that one was like nothing seen before or since.

I think the telling thing about your story is the fact that the memories are so vivid to you to this day. Losses like that leave psychological scars, even nearly 30 years later.

Thanks for sharing.

[…] Wäre ein Crash à la 1987 wirklich so schlecht für die Märkte? (Englisch, awealthofcommonsense) […]

[…] What would a replay of 1987 look like? (A Wealth of Common Sense) […]

[…] Would a repeat of the 1987 crash really be that bad? (A Wealth of Common Sense). Reasons not to dread a downturn. […]

[…] It always feels like this is the big one when losses start to pile up. We start hearing comparisons to the prior peaks in 2000 and 2007 along with some scary stories about the 1987 crash. […]

[…] had a reader leave a comment in a recent post about the 1987 crash. He said he found out about the Black Monday one day 20% plunge on the radio on his way home from […]

[…] market events that occured just after these Fed rate increases ended. Rates peaked just before the 1987 Black Monday crash as well as at the beginning of the 2000-2002 bear market. And the 2007 rate hike ended just […]

[…] Further Reading: Would a Repeat of the 1987 Crash Really Be That Bad? […]

[…] to grow is because we have more access to data, opinions and information than every before. In 1987, people had to learn about the 20% Black Monday crash in the stock market on the radio on their drive home from work. Today you can trade anytime you want by hitting a […]

[…] Further Reading: Would a Repeat of the 1987 Crash Really Be That Bad? […]